Exit planning content overwhelmingly focuses on the financial and structural side — valuation, tax math, deal terms. That work is well-defined and modelable. It is also not where most exits actually fail. Personal readiness has its own runway, and it isn’t on the spreadsheet.

The financial side of business exit is the visible side. The valuation, the tax structure, the gross-to-net math from the prior post in this series on the valuation gap — those are the numbers that get modeled and re-modeled in the months leading up to a transaction. They’re what advisors are trained to analyze, what business owners ask about first, and what conventional exit planning content focuses on.

They’re also not where most exits actually fail.

The pattern that recurs in advisor offices and in industry deal-failure studies is the same: a healthy business, a willing buyer, fair terms, a clean tax structure — and at some point in the process, often late, the owner walks away. The deal collapses. The owner restructures, takes a year, tries again. Sometimes the next attempt succeeds. Sometimes the owner discovers, in the gap year, that they didn’t actually want to exit at all.

Industry data on post-exit regret is notable: a significant majority of business owners who do complete an exit report substantial regret within 12 months. The reason is rarely the deal economics. The reason is that personal readiness — separate from business readiness and financial readiness — never got the same engineering attention as the other two.

This is the gap most exit planning misses.

Three readinesses, not one

The Certified Exit Planning Advisor (CEPA) framework refers to three distinct readinesses required for a successful exit: business readiness (is the business attractive and transferable?), financial readiness (do the numbers work for the owner?), and personal readiness (is the owner actually ready to stop being the owner?).

Most owners optimize for the first two. The first is operational — improving the business, professionalizing management, building processes that don’t require the owner. The second is financial — the planning work from the prior post on the valuation gap. Both are well-understood, well-modeled, and the subject of most exit planning frameworks.

The third is personal. It doesn’t show up on a spreadsheet.

What personal readiness actually means

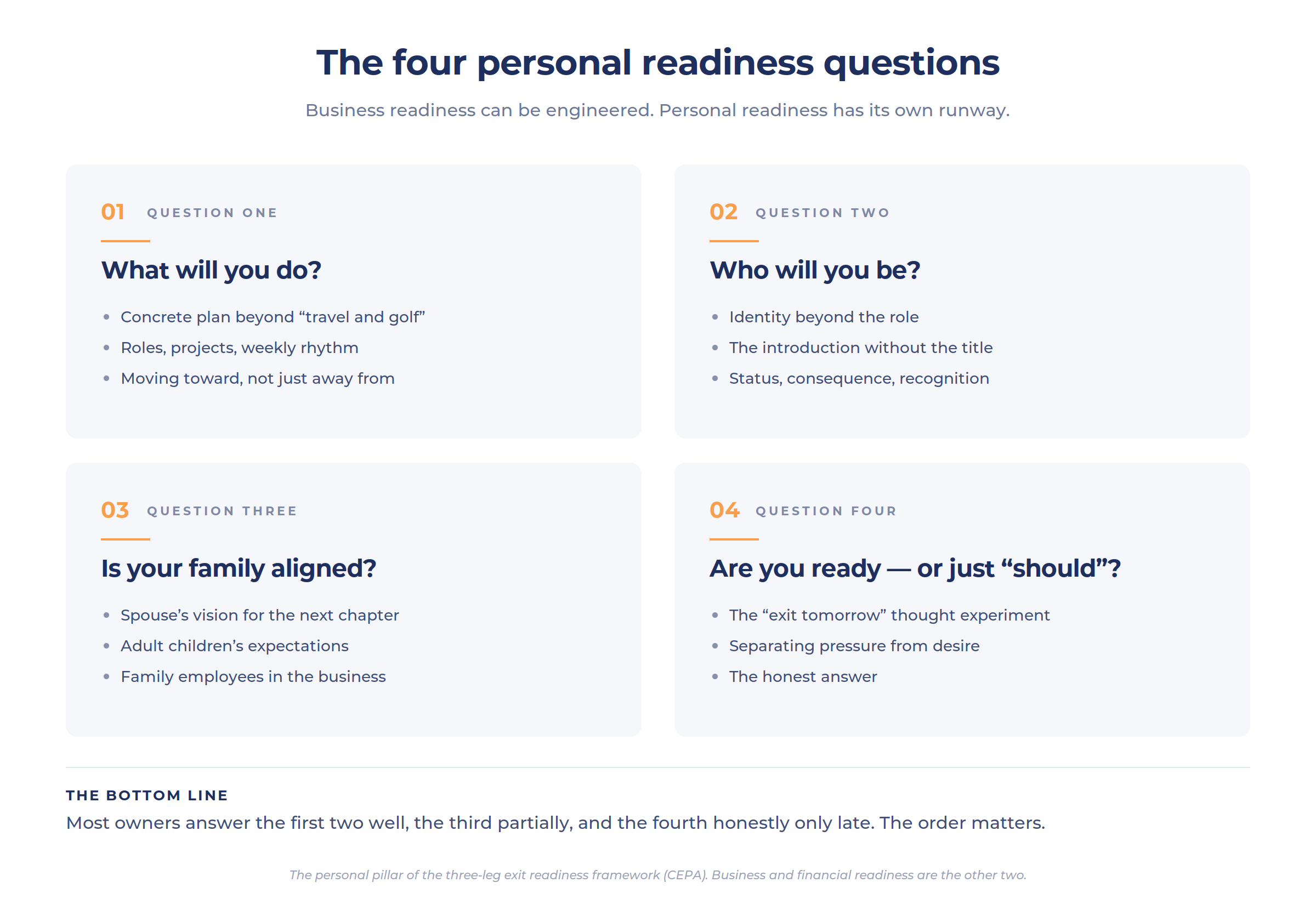

Personal readiness is shorthand for a cluster of separate-but-connected questions. Four of them recur.

What will you do? This is the most concrete question and the one owners most often answer with a vague answer. “I’ll travel.” “I’ll play more golf.” “I’ll spend time with the grandkids.” Those are activities, not lives. The owners who exit well usually have a specific plan for the post-exit chapter: a board role, a nonprofit position, a teaching role, a new venture (often advisory or angel investing), a writing project, a phased step-back, a meaningful philanthropic role. The plan doesn’t need to be permanent. It needs to be concrete. The question isn’t “what will you do all day” — it’s “what are you moving toward, not just away from.”

Who will you be? For owners who built their business over decades, identity is bound up with the role. The introduction is “I run X.” The professional network is the business network. The status, the recognition, the sense of consequence — these are part of the package. Exit removes the role; it doesn’t automatically replace it. Owners who don’t think about identity separately from business often experience what looks like depression in the year following exit. It isn’t depression. It’s that the answer to “who am I” was bound up with an answer that no longer applies.

Is your family aligned? A spouse who’s been adjacent to the business for thirty years has their own model of what the next chapter looks like — which may or may not match the owner’s. Adult children may have their own expectations or anxieties. Family employees (children, siblings, in-laws working in the business) face their own transitions. The conversation that owners often skip until the year of the transaction needs to start much earlier, and recur. “Are we both ready” isn’t a one-time question. It’s a series of questions about lifestyle, geography, social patterns, family dynamics, and shared purpose.

Are you ready, or do you think you should be? This is the hardest one because it requires separating “should” from “want.” Many owners reach the point where the business is exit-ready and the finances are exit-ready and conclude they “should” exit. Some genuinely want to. Some don’t, but feel pressure from advisors, family, or industry norms. The test is straightforward: if the financial constraint were removed entirely — if you could exit tomorrow with full freedom — would you? The owners who answer yes have personal readiness. The owners who answer no usually have unresolved versions of one or more of the prior three questions.

Why personal readiness fails late, not early

A failure of personal readiness rarely shows up early in the process. It shows up late.

Early in exit planning, the conversation is abstract. Numbers on spreadsheets, structural decisions, valuation projections. The owner is engaged but not yet emotionally invested in the decision. It feels like planning, not like actually leaving.

The emotional reality arrives during diligence. Buyers conducting due diligence ask probing questions about the business that surface, for the owner, what’s actually being given up. Long-time employees learn that a transaction is contemplated. Customers and suppliers find out. The transition starts feeling real.

This is when personal unreadiness becomes visible — and when many otherwise-good deals collapse. Owners renegotiate at the eleventh hour. They add conditions that make the deal unworkable. They quietly look for a reason to walk away. Sometimes the rationale is buyer fit or terms; often the underlying issue is that the owner discovered, in the diligence months, that they weren’t actually ready to stop being the owner.

The fix isn’t to engineer the deal differently. The fix is to do personal readiness work years before the diligence happens.

What personal readiness work looks like

It looks unlike most of what’s been discussed in this series. It’s not modeling, and it isn’t structural. It includes:

• Trial separations from the business. Extended time away — three weeks, three months, six months — where the business runs without the owner. These tell the owner what life looks like when the business isn’t filling the calendar. They also test whether the management team can actually operate without daily owner involvement, which doubles as business-readiness work.

• Vision development. Working with a coach, peer advisory group, or trusted advisor on what the next chapter looks like — concretely. Not “travel and golf.” Specific roles, specific projects, specific weekly rhythms.

• Identity work. Separately answering the “who am I” question outside the business role. For many owners this is the hardest piece because business identity has been the dominant frame for decades.

• Family conversations. Repeated, not one-time, conversations with spouse, adult children, family employees. Aligning expectations, surfacing concerns, integrating each family member’s vision for what comes next.

• Calendar audits. A blunt examination of what the owner actually does in a typical week — and what of that, if anything, ports to the next chapter.

This work doesn’t have a deliverable. It doesn’t show up in a financial plan. It doesn’t get reviewed by a board. And it’s the work that determines, more often than not, whether the eventual exit is successful or regretted.

The pattern

The series theme keeps recurring: the work that determines success is the work that happens years before the event. Estate planning isn’t the document. Roth conversion isn’t the conversion. SALT relief isn’t the headline. Business value isn’t the gap.

Exit isn’t the transaction. The transaction is the residue of years of three-leg readiness work — business, financial, and personal. Most owners do the first two. The third is what separates a clean exit from a regretted one.

Your business can be ready in three years. You can be ready in three months. Most owners get those backward.

The plan is the residue. The planning is the work.

Key takeaways

• Successful exits require three distinct readinesses: business (is the company attractive and transferable?), financial (do the numbers work for the owner?), and personal (is the owner actually ready to stop being the owner?). Most exit planning focuses on the first two.

• Personal readiness includes four recurring questions: what will you do, who will you be, is your family aligned, and are you actually ready (separate from “should”)?

• A significant majority of business owners report substantial regret within 12 months of completing an exit. The reason is rarely the deal economics.

• Personal unreadiness usually shows up late in the process — during diligence — and is a common reason otherwise-good deals fall apart.

• Personal readiness work can’t be modeled. It includes trial separations, vision development, identity work, family conversations, and calendar audits.

• Personal readiness has its own runway. It can’t be engineered the same way business readiness can, and it needs to start earlier than most owners think.

Common questions about personal readiness for exit

What is personal readiness in exit planning?

Personal readiness is one of three components — alongside business readiness and financial readiness — that determine whether a business owner can successfully exit. While business readiness focuses on making the company attractive and transferable, and financial readiness focuses on whether the numbers work for the owner’s post-exit life, personal readiness addresses whether the owner is actually prepared to stop being the owner. It includes identity, purpose, family alignment, and emotional readiness — distinct from financial sufficiency.

What are the three readinesses for business exit?

In the Certified Exit Planning Advisor (CEPA) framework, three distinct readinesses are required for a successful exit. Business readiness is whether the company is attractive and transferable to a buyer — operations, management, processes, customer concentration, financial documentation. Financial readiness is whether the owner’s total wealth (business plus other assets) is sufficient to fund post-exit life after taxes and transaction costs. Personal readiness is whether the owner is psychologically and relationally prepared to no longer be the owner. Most exit planning focuses on the first two; the third is often where exits fail.

How common is regret after selling a business?

Industry studies and Exit Planning Institute research consistently show that a significant majority of business owners report substantial regret within 12 months of completing an exit. The reasons are rarely about the deal economics — most regretful owners describe loss of purpose, identity disruption, family tension, or simply a sense that they weren’t actually ready to step away. The regret rate is one of the strongest arguments for treating personal readiness as a separate, multi-year work stream rather than a final-month consideration.

Why do business exit deals fall through?

Deals fall through for many reasons — financing issues, market shifts, valuation disputes, buyer-seller misalignment. But a recurring pattern in advisor experience is that otherwise-good deals collapse late in the process because the owner discovers, during diligence, that they aren’t actually ready to stop being the owner. This often shows up as last-minute renegotiation, added conditions, or a quiet search for a reason to walk away. The underlying issue is typically personal readiness, not deal mechanics.

How long does personal readiness for exit take?

Unlike business readiness — which can be engineered with 2–3 years of focused work on operations, management, and financial documentation — personal readiness doesn’t have a predictable timeline. It includes identity work, vision development, family alignment, and trial separations from the business. For owners whose identity is heavily tied to the role, the process can take longer than the business-side work. It should start well before the contemplated exit window, ideally in parallel with business readiness efforts.

What's the difference between being financially ready to exit and personally ready?

Financial readiness means the numbers work — business value plus other assets, net of taxes and transaction costs, is sufficient to fund the post-exit life as the owner has described it. Personal readiness means the owner is actually prepared to live that post-exit life — psychologically, in identity terms, in family alignment, in concrete vision for the next chapter. Many owners reach financial readiness without personal readiness. Some achieve personal readiness without financial readiness. A successful exit requires both, and the work to build each is largely separate.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. Business exit decisions involve complex personal, family, and financial considerations that should be made in coordination with qualified professionals. Consult your CPA, corporate attorney, financial advisor, and where appropriate a business coach or executive advisor about your specific situation.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.