Every forecast sounds like a strategy. Almost none of them are.

The investment industry runs on predictions. Year-ahead price targets, rate-cut timelines, recession odds, the call on which sector leads next. They arrive with confidence and precision, and they shape how an enormous amount of money gets positioned. The trouble isn’t that the people making them aren’t smart — many are. The trouble is that a portfolio built on a guess inherits the unreliability of the guess.

That’s a narrower claim than “nobody is ever right.” Forecasters are right sometimes. The problem is you can’t tell in advance which forecast is the right one, and the misses tend to cluster at exactly the moments that matter most — the turning points, where being wrong is most expensive.

The track record nobody keeps

Major firms publish year-end market targets every January. By the following December, the spread between the most bullish and most bearish calls is usually wide, and the market often finishes outside that entire range. Almost no one revisits the January predictions to see how they held up, because there’s no scorekeeper and no consequence for being wrong. The forecasts get made, they move money, and then they quietly disappear.

That’s not a knock on any individual analyst. It’s a feature of the activity itself. Forecasting the path of a complex, adaptive system over twelve months is closer to weather prediction past ten days than to anything you can model with precision.

Why prediction breaks down

Markets already reflect what’s widely expected. Today’s price embeds the consensus view of tomorrow. For a forecast to actually make you money, it has to be both different from the consensus and correct — and the events that genuinely move markets are usually the ones almost no one saw coming. By definition, those aren’t in anyone’s forecast.

There’s a second problem: feedback. In most systems you can study, observing the system doesn’t change it. Markets are different. When enough people act on the same prediction, they move the price the prediction was about — sometimes erasing the opportunity, sometimes inverting it. The forecast changes the thing it was trying to forecast.

The real cost of a wrong call

The damage from prediction-based investing isn’t only the missed return. When your allocation depends on a forecast being right, being wrong tends to push you into the worst behavior at the worst time: abandoning a position after the loss, then chasing the recovery after it’s already happened. The forecast doesn’t just fail — it manufactures bad decisions, because it gives you a story to defend instead of a process to follow.

A concentrated bet on a view also concentrates your regret. If the call goes wrong, there’s no framework telling you what to do next. There’s just the uncomfortable choice between doubling down on a thesis that isn’t working and capitulating at the bottom.

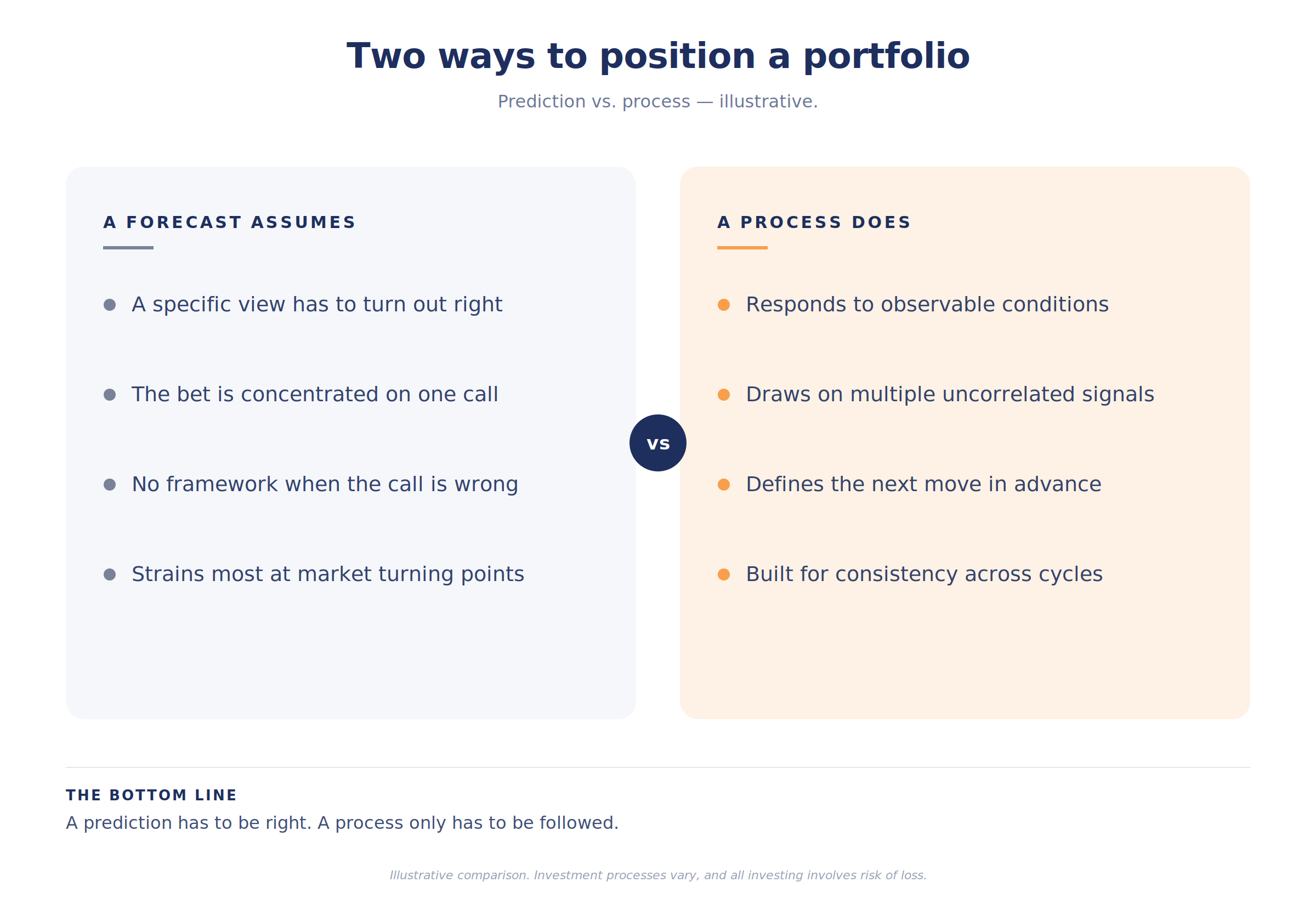

A process instead of a prediction

The alternative isn’t to have no opinion about markets. It’s to stop making the opinion the structure everything rests on.

A rules-based, evidence-driven process starts from a different question. Not “what will happen next?” but “what is actually happening now, and what does the weight of the evidence say to do about it?” Instead of one analyst’s view, it draws on multiple, largely uncorrelated signals — trend and momentum, valuation, yield-curve dynamics, volatility structure, cross-asset behavior — and is designed to respond to observable conditions rather than to a guess about the future. When the data changes, the positioning is built to adapt. When it doesn’t, the process holds.

The point of that design isn’t to be clairvoyant. It’s to behave consistently across market cycles and to remove discretion and emotion from the moment of decision — the moment where prediction-based investing tends to fall apart. None of this promises a particular outcome; markets carry risk regardless of process. But a disciplined framework is built to keep you invested according to a plan instead of according to the last headline.

The pattern

It’s the same idea that runs through good planning. The plan isn’t the document. The exit isn’t the transaction. And the forecast isn’t the portfolio. In each case, the visible artifact — the binder, the closing, the year-ahead call — is the easy part. The work is the discipline underneath it.

A prediction is a bet on being right once. A process is built to work whether you’re right or not.

A forecast asks you to be right. A process asks you to be consistent. Over a full market cycle, consistency is the rarer edge — and the one you can actually build on.

The prediction is the noise. The process is the work.

Key takeaways

• Forecasts are made with confidence and precision, but the future they describe can’t be reliably known — and the misses cluster at the turning points that matter most.

• Markets already price in the consensus, so a forecast only pays off if it’s both different from consensus and correct.

• A wrong call costs more than missed return; it tends to drive selling low and buying high — it manufactures bad decisions.

• A rules-based process asks “what is happening now?” rather than “what will happen next?”

• Drawing on multiple uncorrelated signals is designed to reduce reliance on any single view being right.

• Consistency across cycles, not prediction, is the durable edge.

Common questions about prediction-based investing

Doesn’t every investment decision involve some prediction?

Every decision involves a view of the future in some sense. The distinction is whether your portfolio’s success depends on a specific call being right, or on a process that adapts as conditions change.

Are market forecasts useless, then?

Not useless as commentary or context. The issue is using them as the foundation of how capital is positioned, where their unreliability becomes your unreliability.

What makes a rules-based approach different from just having a strategy?

A rules-based approach defines in advance how it responds to observable conditions, rather than leaving each decision to discretion in the moment — which is where emotion and bias tend to enter.

Does this mean the portfolio never changes?

The opposite. It’s designed to adapt as the underlying data changes — but according to a defined framework rather than a reaction to the latest forecast.

Can a disciplined process still lose money?

Yes. All investing involves risk, including the possible loss of principal. A process is designed to govern behavior and positioning consistently; it does not eliminate market risk.

How does this connect to financial planning?

The same principle applies. Durable outcomes come from a repeatable process, not from getting any single prediction right.

This article is for informational and educational purposes only and is not intended as investment, tax, legal, or financial planning advice. All investing involves risk, including the possible loss of principal. A rules-based or evidence-based investment process does not guarantee any particular result and cannot eliminate market risk. Consult your financial advisor about your specific situation.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

This commentary may incorporate research and tools provided by Helios Quantitative Research LLC (“Helios”), which is associated with, and under the supervision of, Clear Creek Financial Management, LLC (“Clear Creek”), a Registered Investment Advisor. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital.