The standard advice answers a yes/no question. The actual decision is when, how much, and in what sequence.

The standard question gets framed wrong.

"Should I do a Roth conversion?" treats the decision as a single yes-or-no answer — convert, or don't. Most of the advice content online answers it that way. Run the bracket arbitrage math: if your tax rate today is lower than your projected rate later, convert. If it's higher, don't.

That framing is incomplete. The real question isn't whether to convert. It's which years are conversion years — because the answer changes year by year, and a multi-year conversion strategy has to thread several constraints that have nothing to do with bracket arbitrage.

A Roth conversion isn't a tax decision. It's a timing decision disguised as a tax decision.

What "should I convert" actually means

The yes/no framing made sense when Roth conversions were a relatively narrow planning move — usually a one-time decision in a transition year. As Roth conversions have become a more common multi-year strategy, especially in early retirement (the window between work and Required Minimum Distributions), the decision has become temporal. You're not deciding whether to convert. You're deciding how much, in which year, over how many years.

The right way to think about it: you have a pool of pre-tax dollars that will eventually be taxed. The question is whether to pay that tax now — accelerating it on your terms, at brackets you control — or later, on the government's schedule, at brackets that depend on factors outside your control.

But "now" and "later" aren't single moments. They're windows. And the math that determines which window beats which window isn't just about brackets.

What actually has to align

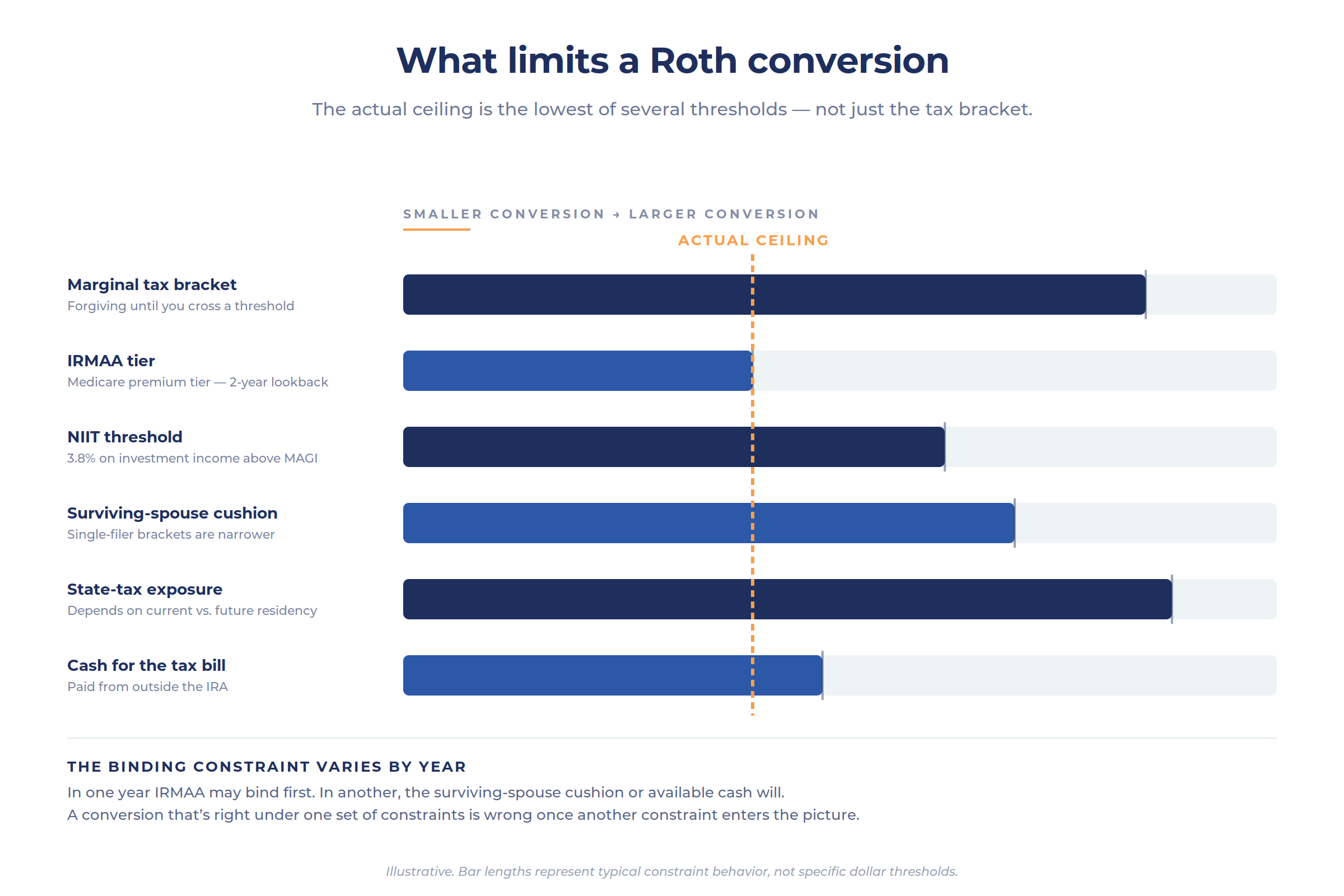

A Roth conversion year is a year when several conditions line up favorably. The standard bracket comparison is one of them. The rest are usually missed.

Current bracket vs. projected bracket. The classic comparison. If your current effective rate on the converted dollars is meaningfully lower than your projected rate when those dollars eventually get distributed — either by you, or by a surviving spouse, or by an heir — converting now produces lifetime tax savings. If your current rate is higher, converting destroys value. The math is straightforward in principle. The hard part is the projection.

IRMAA thresholds. Medicare Part B and Part D premiums are income-related. Income above defined Modified Adjusted Gross Income thresholds bumps you into higher premium tiers — sometimes by hundreds of dollars per month, for both spouses, for the next two years. IRMAA uses a two-year lookback: a conversion in a given year affects premiums two years later. A conversion that crosses an IRMAA tier by even a dollar costs the full additional premium for the year. Crossing two tiers costs twice.

This is the seam most commonly missed. The bracket math says "convert another $40,000 this year — you're still in the 22% bracket." The IRMAA math says "those last $5,000 just pushed you across the next premium tier and will cost you an additional several thousand dollars in Medicare premiums two years out." Bracket math wins on the conversion year. IRMAA math wins on the actual outcome.

The surviving-spouse cliff. Married couples filing jointly have wider tax brackets than single filers. When one spouse dies, the survivor files single — and the same income is taxed at meaningfully higher marginal rates. Converting more aggressively while both spouses are alive often makes sense not because the immediate math favors it, but because the future math — once the survivor is filing single — favors having already paid tax on those dollars. The conversion decision shouldn't model only the couple's current bracket. It should also model the survivor's bracket, weighted by life-expectancy assumptions.

State-tax exposure. If you live in a high-tax state today but plan to retire to a no-tax state, converting now means paying state tax that you wouldn't pay later. If you live in a no-tax state today but might move to a high-tax state for family reasons, converting now locks in the state tax advantage. State residence is a planning variable, not a fact of life.

NIIT and other thresholds. The 3.8% Net Investment Income Tax applies above certain MAGI thresholds. A conversion can push other income into NIIT exposure, even if the conversion itself isn't investment income. Similar threshold effects apply to deductions phase-outs, the American Opportunity Tax Credit for dependents, and other features of the tax code that key off MAGI.

Liquidity for the tax bill. The tax on a Roth conversion is owed in the year of conversion. Paying that tax from the IRA itself defeats the purpose — you've withdrawn IRA dollars to pay tax instead of converting them. Paying from outside the IRA requires either taxable cash or selling other assets (which has its own tax implications). The availability of outside cash is a real constraint on conversion size, not a footnote.

RMD trajectory. Conversions reduce the future RMD base, which reduces forced distributions later. The savings only matter if the future RMDs would have pushed you into higher brackets, higher IRMAA tiers, or NIIT exposure. If your projected RMDs were going to be modest anyway, the conversion's main benefit is the bracket arbitrage and the surviving-spouse benefit — not the RMD reduction itself.

These constraints don't cleanly resolve into a formula. They create a window — usually narrow — where a conversion makes sense in any given year. The window's size and location changes year by year.

What makes a year a conversion year

Most years are not conversion years. Most conversion plans don't run continuously — they run in concentrated periods when several conditions align.

The most common conversion-friendly window is the period between retirement and the start of Required Minimum Distributions. In this window, earned income has dropped, Social Security may not have started yet (deferring Social Security past Full Retirement Age is a common strategy), and RMDs haven't kicked in. The result is a multi-year period of low taxable income — sometimes the lowest of an entire adult life — during which converting pre-tax dollars at relatively low marginal rates can move substantial assets to Roth treatment for the long run.

Inside that broad window, the specific years that are conversion years still depend on the other variables. A year with a big medical event, a windfall, a property sale, or a state-residency change isn't a conversion year — even if the bracket math looks good. Conversely, a year with unexpectedly low income, or one that comes right before a planned move to a high-tax state, can be a high-priority conversion year that other "scheduled" conversions should defer to.

A Roth conversion isn't a tax decision. It's a timing decision disguised as a tax decision.

This is the part that the planning framework from earlier posts in this series matters for. A multi-year Roth conversion plan isn't a one-time decision. It's a recurring evaluation — once a year, based on the conditions of that specific year, run inside an ongoing planning process that reassesses what changed. The plan made in the vision phase of the year gets stress-tested in the mid-year wealth strategy phase against what actually happened. If income came in higher than projected, the conversion scales back. If a Social Security claiming decision shifts, the conversion sequence adjusts. If a state-residency change is now on the table for next year, this year's conversion sizing changes accordingly.

The plan is the residue. The planning is the work.

The integration point

A Roth conversion is the textbook example of why cross-domain planning matters. The decision touches tax, healthcare, estate, retirement income, state residency, and charitable strategy. Each of those has a specialist. None of those specialists individually owns the integration.

The tax preparer can run the bracket math, but isn't necessarily modeling IRMAA, the surviving-spouse cliff, or state-residency changes. The estate attorney isn't modeling tax. The Medicare specialist isn't modeling income brackets. The financial advisor sometimes models the bracket math but skips the rest. Each one is doing their job. None is doing the integration.

A Roth conversion that gets done well is one where someone is responsible for surfacing all the constraints, modeling the consequences across domains, and making sure the conversion year sizing accounts for all of them. The decision that looks right inside any single specialist's lane often looks wrong once the lanes are integrated.

The right question

The yes/no framing — "should I do a Roth conversion?" — produces answers that look right and miss what matters. Yes, the bracket math favors converting. Yes, your future rate is probably higher. Convert.

The integrated question — "which years should be conversion years, at what sizes, threading which constraints?" — produces different answers. Sometimes much smaller conversions than the bracket math suggested. Sometimes a different sequence across years than a uniform ladder would suggest. Sometimes no conversion at all in a year that looked like an obvious conversion year before the other constraints got modeled.

The conversion decision is one of the clearest places where the difference between having a plan and being actively planned with shows up in actual dollars. The plan that says "convert $X a year for the next five years" can be technically correct and still miss meaningfully — because it ignores what's changing year by year. The planning relationship that re-evaluates the conversion question every year, against that year's specific constraints, captures value the plan can't.

Roth conversions aren't a tax problem. They're a timing problem disguised as a tax problem — and the timing only works if someone is actively planning the conversion, not just deciding to do it.

Key takeaways

• The standard "should I convert?" framing misses the actual decision. The real question is which years are conversion years, at what size, in what sequence.

• A Roth conversion year has to thread several constraints simultaneously: current bracket, projected future bracket, IRMAA thresholds, the surviving-spouse cliff, state-tax exposure, NIIT, RMD trajectory, and liquidity for the tax bill.

• Most years are not conversion years. The conversion-friendly window is usually a concentrated period — most often the years between retirement and the start of RMDs.

• The right conversion amount in a given year changes year by year as conditions shift. A multi-year conversion plan has to be re-evaluated inside an ongoing planning process, not set once.

• Roth conversions are the textbook example of why cross-domain integration matters. The decision touches tax, healthcare, estate, retirement income, and state residency — and no single specialist owns the integration.

This article is for educational purposes and is not personalized tax advice. Roth conversion decisions depend on specific facts and circumstances — including current and projected tax brackets, IRMAA thresholds, state of residence, family situation, and available liquidity. Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. Discuss your situation with your tax advisor and financial advisor before acting.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).