When one spouse dies, the survivor’s income usually falls — but the tax bill often climbs. It’s one of the most predictable problems in retirement, and one of the most plannable, if you start before it happens.

A higher tax bill on a smaller income

Here’s the part that catches families off guard. When a spouse dies, you’d expect taxes to go down — the household is smaller, the income is lower. Instead, the surviving spouse frequently pays more tax on less income.

The reason is filing status. For the year of death, the survivor can still file jointly. After that — unless they have a dependent child — they file as a single taxpayer. And the single tax system is built for one person’s income, not two people’s worth of pensions, required distributions, and portfolio income that mostly keeps flowing after one spouse is gone.

This is the widow’s penalty. It has nothing to do with the size of the estate and everything to do with how the survivor’s income gets taxed going forward.

Why income barely drops but taxes climb

When a spouse dies, the household loses one Social Security benefit — the smaller of the two; the survivor keeps the larger. But pensions often continue (sometimes reduced), required minimum distributions keep coming, and the investment portfolio is still the same portfolio. So the income that lands on the tax return may be only modestly lower than before.

The tax treatment of that income, though, changes sharply.

The three places it bites

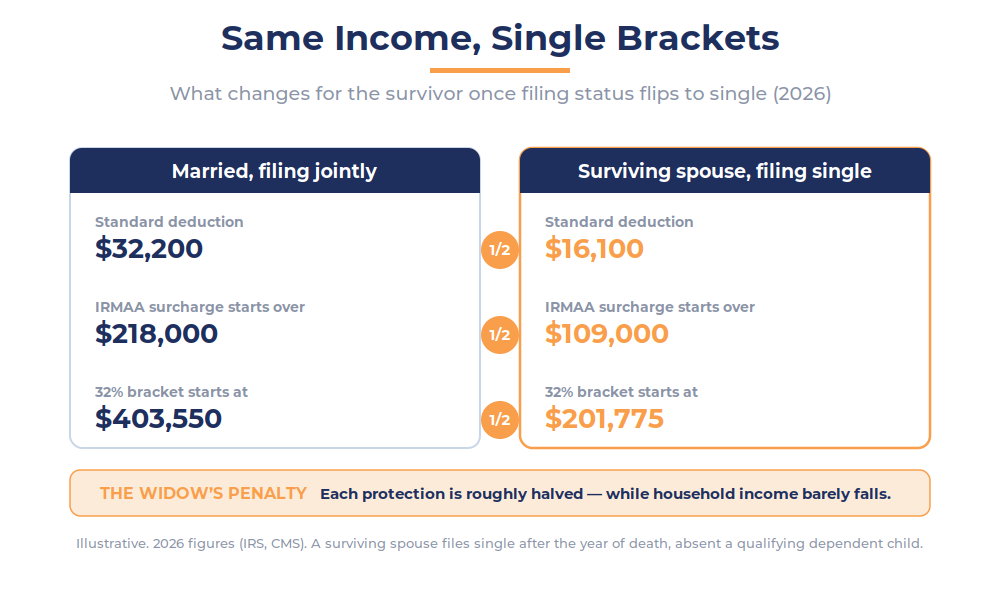

The brackets compress. Single brackets are roughly half as wide as joint brackets through most of the schedule. The same taxable income that sat comfortably in the 24% bracket as a couple can spill into 32% as a single filer — for 2026, that jump happens at about $201,775 for a single filer versus $403,550 for a couple. Same dollars, higher marginal rate.

The standard deduction is cut in half. For 2026 it falls from $32,200 (married filing jointly) to $16,100 (single). More of the survivor’s income becomes taxable. Seniors get an additional age-based deduction, but the survivor now claims one person’s worth instead of two — and the temporary $6,000 senior deduction (through 2028) phases out at a lower income for a single filer ($75,000 of MAGI) than for a couple ($150,000), so a survivor can lose a deduction the couple kept.

IRMAA thresholds drop by half. The Medicare surcharge that kicks in at $218,000 of income for a couple kicks in at $109,000 for a single filer in 2026 — exactly half. IRMAA is a cliff: one dollar over a threshold triggers the full surcharge for that tier, and it is based on income from two years earlier. A survivor with the same income a couple comfortably absorbed can suddenly owe thousands more in Medicare premiums.

What you can do before it happens

The good news is that almost everything that makes the widow’s penalty worse is visible in advance — and the most powerful moves happen while both spouses are alive, when the wider joint brackets are still available.

Filling up the lower joint brackets deliberately — for example, through Roth conversions in lower-income years before required distributions and Medicare begin — moves money out of accounts that would otherwise generate taxable income for a future single filer. Whether that makes sense, and how much, depends entirely on your situation and should be modeled with your CPA. Managing income around the IRMAA cliffs, and, for the charitably inclined, using qualified charitable distributions to keep reportable income down, are levers too.

One nuance worth knowing: when a spouse dies, the survivor can sometimes appeal an IRMAA determination using Form SSA-44, since death of a spouse is a qualifying life-changing event. That can help when income actually drops — but it does not undo the bracket-and-deduction math of filing single. The structural penalty is solved by planning, not by an appeal after the fact.

The widow’s penalty is one of the few tax problems you can see coming years in advance. That’s exactly why it belongs on the to-do list while both spouses are still here.

None of this is about predicting when something will happen. It’s about recognizing that the surviving spouse’s tax bill is largely set by decisions made years earlier — and using the joint-filing years on purpose rather than letting them pass. For most couples, that’s the difference between a survivor who’s comfortable and one who’s quietly handing more to the IRS every year for the rest of their life.

Key takeaways

• After the year of death, a surviving spouse without a dependent child files as single — narrower brackets, half the standard deduction, lower IRMAA thresholds.

• Household income often drops only modestly (one Social Security check is lost; pensions, RMDs, and portfolio income largely continue), so the same income is taxed harder.

• For 2026, the standard deduction falls from $32,200 (MFJ) to $16,100 (single), and IRMAA’s first threshold falls from $218,000 to $109,000 — both exactly half.

• IRMAA is a per-person cliff based on income from two years prior, so a survivor can be surprised by a surcharge years later.

• The most effective moves — Roth conversions, income smoothing, managing IRMAA cliffs — happen while both spouses are alive and the wider joint brackets are available.

• An SSA-44 appeal can help after an income drop but does not undo the filing-status math; the penalty is solved by planning ahead.

Common questions about the widow’s penalty

What is the “widow’s penalty”?

It is the higher tax burden a surviving spouse often faces after a spouse’s death, because they shift from married-filing-jointly to single — with narrower brackets, a smaller standard deduction, and lower IRMAA thresholds — applied to an income that usually drops only modestly.

Doesn’t income go down enough to offset it?

Usually not. The household loses one Social Security benefit (the smaller one), but pensions, required distributions, and portfolio income largely continue. The income decline is often small relative to how much harder it is taxed as a single filer.

When does the survivor start filing as single?

The year of death, a joint return is still allowed. After that, the survivor files single — unless they have a qualifying dependent child, which can allow joint rates for up to two more years.

How does this affect Medicare?

IRMAA surcharges on Medicare Part B and D start at half the income for a single filer ($109,000 in 2026) versus a couple ($218,000). Because it is a cliff based on income from two years earlier, a survivor can cross a threshold unexpectedly and owe materially higher premiums.

Can anything be done after the fact?

Some things help — an SSA-44 appeal if income drops for a qualifying event, and ongoing income management. But the structural penalty is best addressed before it happens, while both spouses are alive.

What’s the single most useful step?

Using the joint-filing years on purpose — often by filling lower brackets through Roth conversions or other income-smoothing while the wider joint brackets are available — modeled with your CPA for your specific situation.

This article is for educational purposes only and is not tax advice. Consult your CPA or tax advisor before acting on anything described here.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.