Required minimum distributions look like a chore — a form, a calculation, a withdrawal the government makes you take. For someone who saved diligently into pre-tax accounts for forty years, they can be something else: a tax squeeze that arrives on a fixed schedule, just when you have the least flexibility to do anything about it. The good news is that the real planning happens years before the first one is due.

At some point in your seventies, the IRS stops letting you leave your traditional retirement accounts alone. You’ve deferred tax on that money for decades — contributions and growth, untaxed — and now it wants its share. So it requires you to start withdrawing a minimum amount each year, and to pay ordinary income tax on every dollar.

That’s a required minimum distribution, and on its own it’s purely mechanical: a balance divided by a number from an IRS table. The mechanics aren’t the story. The story is what those forced withdrawals can do to a successful saver’s tax picture — and why the time to deal with them is the decade before they start, not the year they arrive.

What an RMD actually is

The rules are straightforward. Once you reach your required age, you must withdraw a minimum amount each year from tax-deferred accounts — traditional IRAs, 401(k)s, and similar plans — calculated by dividing the prior year-end balance by a life-expectancy factor from the IRS table. At 73, that factor works out to roughly 3.8% of the balance; the percentage climbs as you age.

A few specifics worth knowing:

• The age is 73 if you were born between 1951 and 1959, and 75 if you were born in 1960 or later. (Under the SECURE 2.0 law, the starting age stepped up from 72, and rises again to 75 in 2033.)

• Roth accounts are exempt. Roth IRAs never require distributions during your lifetime, and Roth 401(k)s stopped requiring them in 2024.

• The penalty for missing one is steep — 25% of the amount you should have taken, though it drops to 10% if you fix it promptly.

None of that is the hard part. The hard part is what the withdrawals do to everything else.

How success becomes a tax problem

Here’s the squeeze. If you saved well, your pre-tax balances are large — and a required withdrawal is a percentage of a large number. That forced income lands on top of everything else you already have coming in: Social Security, a pension, dividends, rental income. Stacked together, it can push you into a higher bracket in your seventies than you were in while working.

And the damage doesn’t stop at your tax bracket. That same income raises the share of your Social Security that gets taxed, and it can lift you over the thresholds that trigger IRMAA — the income-based surcharge on Medicare premiums we covered earlier in this series. One forced withdrawal can quietly raise three different bills at once.

The cruel part is the timing. By the time RMDs begin, your income is high and largely locked in — Social Security is on, the pension is flowing, the balances are big. You have the least room to maneuver exactly when the bill comes due. The flexibility was all in the years before.

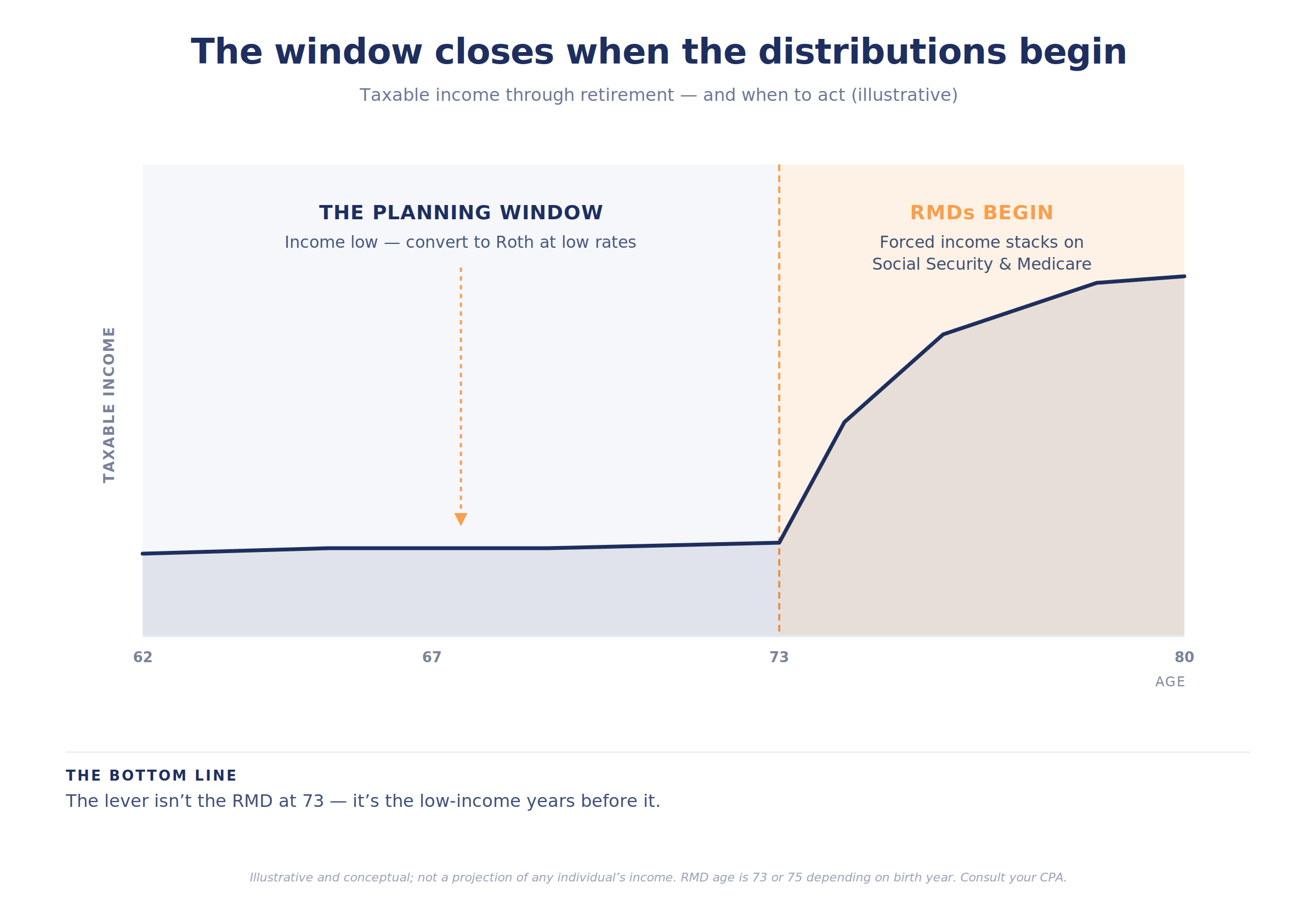

The window — the quiet years in your sixties

Between the day you stop working and the day RMDs (and often Social Security) begin, many successful people pass through the lowest-income years of their adult lives. No paycheck. No required withdrawals yet. Maybe Social Security not yet turned on. For a stretch — often the early-to-mid sixties into the early seventies — your taxable income can be unusually, temporarily low.

That window is the whole game. It’s the time to voluntarily pull money out of pre-tax accounts at low rates — through Roth conversions — shrinking the balance that will someday drive your RMDs. Every dollar you convert in a low-bracket year is a dollar that won’t be forced out at a higher rate later, won’t inflate your future RMD, and won’t stack onto Social Security and Medicare down the line. You’re not avoiding the tax; you’re choosing to pay it when you control the rate instead of when the IRS sets the schedule.

Done deliberately over several years, this can meaningfully flatten the spike — converting in your sixties to lower the forced income in your seventies and beyond. It has to be coordinated, though: convert too aggressively and you create the very bracket and IRMAA problems you’re trying to avoid. The art is filling up the low brackets each year without spilling over.

A few more levers

Beyond conversions, a handful of tools help once RMDs are near or underway:

• Qualified charitable distributions. From age 70½, you can send up to $111,000 a year (indexed) directly from an IRA to charity. It counts toward your RMD but never hits your taxable income — the most tax-efficient way to give if you’re charitably inclined, and especially valuable if you don’t itemize.

• The first-year timing trap. You can delay your very first RMD to April 1 of the following year — but then you take two in one year, often a worse tax outcome than just taking the first one on time.

• The still-working exception. If you’re still employed past your RMD age and don’t own a large stake in the company, you can generally delay RMDs from that employer’s plan (though not from your IRAs).

The pattern

The RMD isn’t the decision. It’s the bill that arrives for decisions you made — or didn’t make — years earlier. By the time the first one is due, the levers that matter most have largely been put away.

That’s the through-line that runs through so much of this: the work happens upstream, in the quiet years before the forced event, when income is low and options are open. Required distributions are the most predictable tax event in retirement — you can see them coming a decade out. Which means they reward, more than almost anything else, the people who plan for them before they start.

A required distribution is the bill for tax you deferred decades ago. The only question left at 73 is whether you planned for it at 63.

The withdrawal itself is a formula you can’t argue with. What you can shape is the balance it’s calculated on, and the bracket it lands in — and both of those are decided in the years before the first distribution, not after. The work is using the quiet window while it’s open.

The plan is the residue. The planning is the work.

Key takeaways

• Required minimum distributions are forced annual withdrawals from tax-deferred accounts, taxed as ordinary income, starting at 73 (born 1951–1959) or 75 (born 1960+).

• For diligent savers, large pre-tax balances mean large forced withdrawals that can push you into a higher bracket in your seventies than during your working years.

• That forced income also increases the taxable share of Social Security and can trigger IRMAA Medicare surcharges — one withdrawal raising several bills.

• The planning window is the low-income years before RMDs (and often before Social Security) begin — typically the sixties.

• Roth conversions in those low-bracket years shrink the future RMD base; the art is filling low brackets without spilling into higher ones or IRMAA.

• Qualified charitable distributions (up to $111,000 in 2026, from age 70½) satisfy RMDs without adding to taxable income; Roth accounts have no lifetime RMDs.

Common questions about required minimum distributions

When do RMDs start?

At 73 if you were born between 1951 and 1959, or 75 if born in 1960 or later. The first one can be delayed to April 1 of the following year, but that forces two withdrawals in one year.

How is the RMD amount calculated?

Your prior year-end balance divided by a life-expectancy factor from the IRS table — roughly 3.8% of the balance at 73, rising with age.

What’s the penalty for missing one?

25% of the amount you should have withdrawn, reduced to 10% if you correct it promptly.

Do Roth accounts have RMDs?

Roth IRAs never require lifetime distributions, and Roth 401(k)s stopped requiring them in 2024.

How can I reduce future RMDs?

Most commonly, Roth conversions in the lower-income years before RMDs begin, which shrink the pre-tax balance that drives them.

What’s a QCD?

A qualified charitable distribution: from age 70½ you can give up to $111,000 a year (indexed) directly from an IRA to charity, satisfying your RMD without the income counting toward your taxes.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. RMD ages, life-expectancy factors, contribution and QCD limits, and other rules can change, and the right strategy depends on your specific circumstances. Roth conversions create taxable income in the year of conversion and aren’t right for everyone. Consult your CPA, tax advisor, and financial advisor about your situation before acting.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.