Three changes to the charitable deduction took effect in 2026, and together they reward giving with a plan over giving on autopilot. The good news: the same dollars, given on a smarter schedule, can produce a noticeably bigger deduction.

What changed in 2026

For years, charitable giving had a simple tax story: if you itemized, you deducted what you gave. The One Big Beautiful Bill Act added three wrinkles, all effective with the 2026 tax year.

First, a floor. Itemizers can now only deduct charitable contributions to the extent they exceed 0.5% of adjusted gross income. The first half-percent of your AGI in giving is simply non-deductible. On a $400,000 income, that’s the first $2,000 of donations gone from your deduction — every year.

Second, a cap for top earners. For donors in the 37% bracket, the value of itemized deductions, charitable ones included, is now capped at 35 cents on the dollar rather than 37. A $100,000 gift that once cut taxes by $37,000 now cuts them by $35,000.

Third, a small break for non-itemizers. If you take the standard deduction, you can now also deduct up to $1,000 (single) or $2,000 (married) of cash gifts to qualifying charities — a modest but permanent benefit that didn’t exist before. It doesn’t apply to gifts made to donor-advised funds, though.

None of this is a reason to give less. It’s a reason to give deliberately.

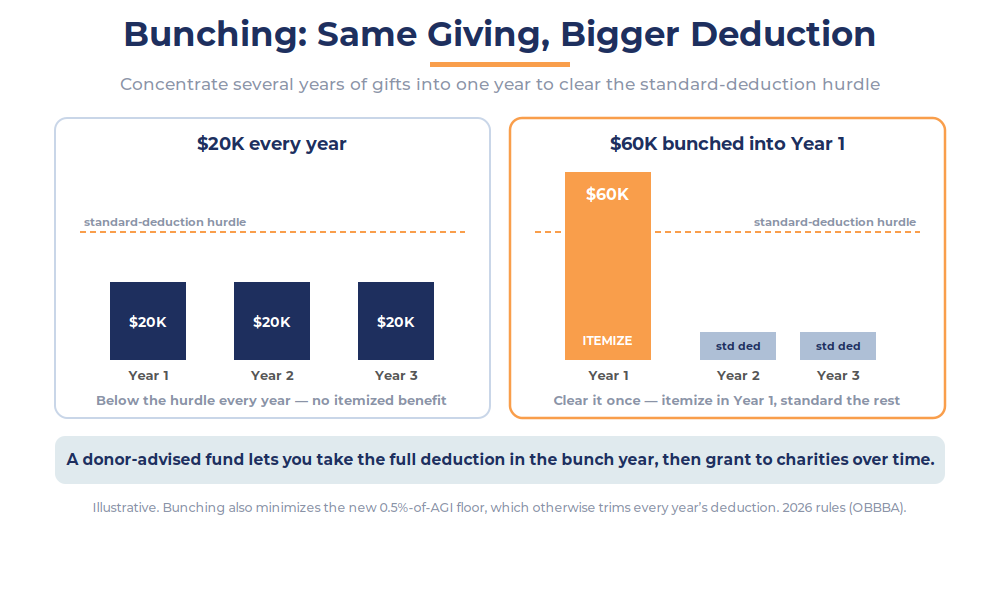

Why bunching got more powerful

The floor changes the math in a way that rewards concentration. If you give roughly the same amount every year, you absorb that 0.5% haircut annually, and if your total giving plus other deductions doesn’t clear the standard deduction, you get no itemized benefit at all.

Bunching flips that. Instead of giving $20,000 a year for three years, you give $60,000 in one year and nothing the next two. In the bunch year, you sail past both the 0.5% floor and the standard-deduction threshold, itemize, and capture a real deduction. In the off years, you simply take the standard deduction. Same total given, far more deducted — because you only pay the floor’s toll once instead of three times, and you only need to clear the itemizing hurdle once.

The catch is logistical: most people don’t want to dump three years of giving on their favorite charity in a single January and leave it dry the next two. That’s where the donor-advised fund comes in.

Where the donor-advised fund fits

A donor-advised fund solves the timing problem. You contribute a lump sum in your bunch year — and take the full deduction that year — then recommend grants out to the charities you support on whatever schedule you like, over the following years. The charities still receive a steady stream; you get the concentrated deduction. The fund can also invest the balance while it waits to be granted.

It pairs especially well with one more move: funding the DAF with appreciated stock rather than cash. Donate a long-held position that’s gained value, and you generally skip the capital gains tax entirely and deduct the full market value. In California, where capital gains are taxed as ordinary income at rates up to 13.3%, sidestepping that gain is often worth more than the income-tax deduction itself. And notably, the new 35% cap doesn’t touch the capital-gains savings — that benefit is untouched.

The move for retirees: QCDs

If you’re 70½ or older, there’s a lever that sidesteps all of this. A qualified charitable distribution sends money directly from your IRA to a charity — up to $111,000 in 2026 — and it never lands in your income at all. Because it reduces your AGI rather than working as an itemized deduction, the QCD skips the 0.5% floor and the 35% cap completely. It can also count toward your required minimum distribution.

For a retiree who’s charitably inclined and taking RMDs, the QCD is frequently the single most tax-efficient way to give a dollar to charity under the new rules — more efficient than writing a check and deducting it. The one limitation: it has to go to an operating charity, not to a donor-advised fund.

The new rules don’t punish generosity. They reward the donor who gives the same amount with a plan instead of on autopilot.

Putting it together

The right approach depends on your situation, and the pieces combine. A working high earner might bunch several years of appreciated-stock gifts into a donor-advised fund in a high-income year — clearing the floor, beating the standard deduction, and dodging the capital gains tax all at once. A retiree might lean on QCDs to give straight from an IRA while keeping AGI down, which has the added benefit of easing Medicare surcharges and other income-driven costs. A couple who gives modestly and takes the standard deduction can simply use the new non-itemizer deduction.

What ties them together is intent. The 2026 rules added friction to casual, year-after-year giving and left the rewards for donors who plan the timing, the vehicle, and the asset. Map your giving against your income years with your CPA and advisor, and the same generosity does more — for the causes you care about and for your tax bill.

Key takeaways

• Starting in 2026, itemizers can only deduct charitable gifts that exceed 0.5% of AGI — the first slice of every year’s giving is non-deductible.

• For 37%-bracket donors, the value of itemized deductions (charitable included) is capped at 35 cents on the dollar.

• Non-itemizers get a new permanent deduction of up to $1,000 (single) / $2,000 (married) for cash gifts — but not for gifts to donor-advised funds.

• Bunching multiple years of giving into one year clears the floor and the standard-deduction hurdle once instead of repeatedly — and a donor-advised fund lets you still grant to charities gradually.

• Funding a DAF with appreciated stock skips capital gains (worth up to 13.3% in California) on top of the deduction, and the 35% cap doesn’t reduce that benefit.

• For those 70½+, QCDs (up to $111,000 in 2026) give straight from an IRA, sidestep the floor and the cap, and can satisfy RMDs.

Common questions about the 2026 charitable rules

What is the new 0.5% floor?

Beginning in 2026, itemizers can only deduct charitable contributions above 0.5% of their adjusted gross income. At a $300,000 AGI, the first $1,500 of giving isn’t deductible.

What is the 35% cap?

For taxpayers in the top 37% bracket, the tax benefit of itemized deductions — including charitable — is limited to 35 cents per dollar instead of 37. It slightly raises the after-tax cost of large gifts.

What’s bunching?

Concentrating several years’ worth of charitable giving into a single tax year, so you clear the deduction floor and the standard-deduction threshold once rather than getting little or no benefit spreading the same total across multiple years.

How does a donor-advised fund help?

It lets you take the full deduction in the year you fund it, then recommend grants to charities over time — so you can bunch the tax benefit without forcing all the actual giving into one year.

Can I use the new non-itemizer deduction with a DAF?

No. The $1,000/$2,000 above-the-line deduction is only for cash gifts made directly to qualifying charities, not to donor-advised funds or private foundations.

Are QCDs still worthwhile?

Often more than ever. Because a qualified charitable distribution reduces AGI instead of working as an itemized deduction, it avoids the 0.5% floor and the 35% cap entirely — and can satisfy an RMD. It must go to an operating charity, not a DAF.

This article is for educational purposes only and is not tax advice. Consult your CPA or tax advisor before acting on anything described here.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.