Almost everyone with a health savings account uses it the same way: money goes in, and it comes right back out at the pharmacy counter. That’s the obvious use — and it quietly wastes the most tax-favored account in the code. Used the other way, an HSA isn’t a way to pay medical bills. It’s a strategy to build tax-free wealth.

The HSA gets filed in most people’s minds next to the FSA — a place to park some pre-tax money for copays and prescriptions, spent down by year’s end. That’s a fine use. It’s also the least valuable thing an HSA can do.

Because of how it’s taxed, the HSA is the single most efficient savings vehicle available to people who can afford to leave it alone. No other account offers the same deal. The catch is that capturing it means doing the opposite of what the account seems built for: not spending it.

The only account with three tax breaks

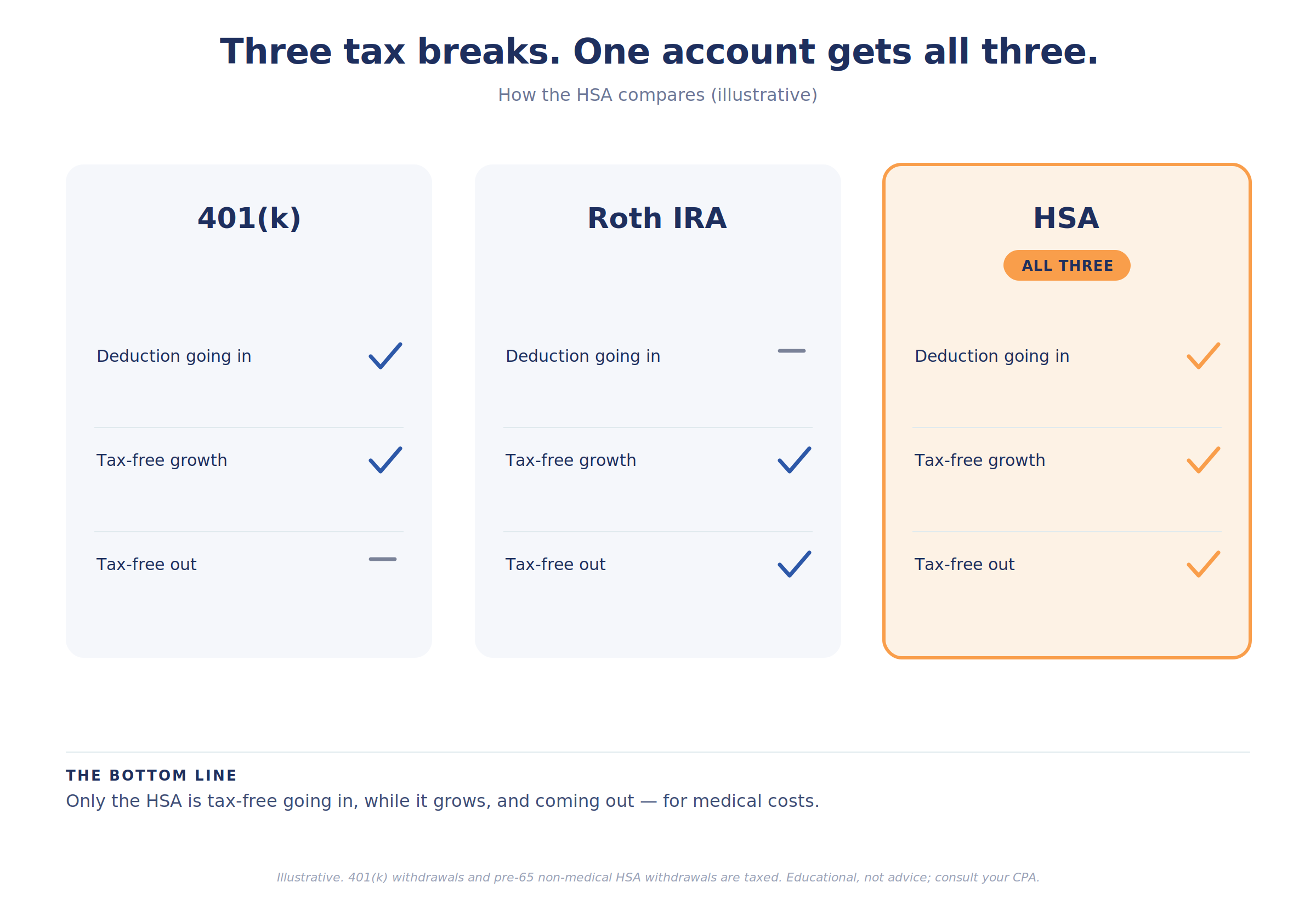

Every tax-advantaged account gives you one tax break, or at most two. A traditional 401(k) gives you a deduction going in, but the money is taxed coming out. A Roth gives you tax-free withdrawals, but no deduction going in. The HSA gives you all three at once:

• Contributions are deductible — they go in pre-tax, lowering this year’s taxable income.

• Growth is untaxed — no tax on dividends, interest, or capital gains inside the account.

• Withdrawals are tax-free — when used for qualified medical expenses, at any age.

Deduction in, tax-free growth, tax-free out. No other account does all three. That triple break is why, dollar for dollar, an HSA left to compound is the most tax-efficient money you can own.

For 2026, you can contribute $4,400 with individual coverage or $8,750 for a family, plus an extra $1,000 if you’re 55 or older. (Note the age — the HSA catch-up starts at 55, not 50.) You need to be enrolled in a qualifying high-deductible health plan to contribute.

The move — stop spending it

Here’s the strategy that turns a healthcare account into a retirement account, and almost nobody uses it: pay your medical bills out of pocket, and leave the HSA alone to grow.

Most people don’t invest their HSA at all — they leave it in cash and spend it as expenses come up. That captures only the first tax break and throws away the other two. The alternative: invest the balance the way you would a retirement account, pay current medical costs from regular cash flow, and let the HSA compound for decades.

The mechanism that makes this work is a quirk most people don’t know about: there’s no deadline to reimburse yourself. Save the receipt for a medical expense you pay today, leave the HSA untouched, and you can reimburse yourself for that expense tax-free years — even decades — later. A bill you paid in 2026 can come out of the HSA, tax-free, in 2046. Keep the receipts in a folder, and you’ve built a pool of tax-free withdrawals you can tap whenever you want.

And after 65, the account gets even more flexible. You can still pull money out tax-free for medical costs — including Medicare premiums — but you can also withdraw it for anything else, taxed simply as ordinary income with no penalty. At that point it behaves like a traditional IRA for non-medical use, and stays tax-free for the medical costs that are all but certain in retirement. Estimates routinely put a retired couple’s lifetime healthcare bill in the hundreds of thousands of dollars; an invested HSA is the most tax-efficient way to meet it.

The California asterisk

There’s a catch for California residents that most national articles skip entirely. California is one of a small number of states that doesn’t recognize the HSA’s tax benefits at the state level.

In practice, that means two things. Your contributions aren’t deductible on your California return — you owe state income tax on the money you put in. And the earnings inside the account — dividends, interest, capital gains — are taxable by California each year, even while they grow tax-free federally. For a high earner in a 13.3% state, that’s not nothing.

It doesn’t break the case for an HSA; the federal triple break is valuable enough on its own that funding and investing one still makes sense for most eligible Californians. But it does change the details. The state-level tax on earnings is a reason to keep the HSA’s investments tax-efficient, and one more reason to coordinate the account with the rest of your plan rather than treating it as free money. If you later move to a state that does recognize HSAs, the math improves — another small line item for the “leaving California” checklist.

The fine print worth knowing

A few practical points that trip people up:

• You need a high-deductible health plan to contribute, and the contribution limits include anything your employer puts in — their contribution reduces your room.

• Contributing through payroll is more efficient than writing a check, because payroll contributions also avoid the FICA taxes that direct contributions don’t.

• Many custodians require a small cash balance before you can invest the rest, so the “invest it” approach may leave a modest cushion in cash.

• Once you enroll in Medicare, you can no longer contribute — which makes the working years before 65 the window to fund it.

The pattern

The HSA isn’t a health account. It’s a retirement account wearing a health account’s clothes, and the people who get the most from it are the ones who resist using it the obvious way.

That’s a through-line that runs through a lot of good planning: the most valuable move is often the one the account doesn’t advertise. Fund it, invest it, pay your medical bills from cash flow, save the receipts, and let the rarest tax treatment in the code do its work for thirty years. The version of this account that pays for today’s prescription is fine. The version that quietly becomes a tax-free retirement fund is the one worth building.

An HSA used for spending captures one tax break. An HSA left to grow captures all three.

The account is the same either way; what changes is whether you let it do its best work. Spent down each year, it’s a modest convenience. Funded, invested, and left alone — coordinated with your cash flow, your state’s rules, and the rest of your plan — it’s the most tax-efficient dollar you own. The work is choosing the second version on purpose.

The plan is the residue. The planning is the work.

Key takeaways

• The HSA is the only account with a triple tax advantage: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

• Using it as a spending account captures just one of the three breaks; investing it and leaving it alone captures all three.

• For 2026 you can contribute $4,400 (individual) or $8,750 (family), plus a $1,000 catch-up at 55+, with a qualifying high-deductible health plan.

• There’s no deadline to reimburse yourself — pay medical bills from cash flow, save receipts, and reimburse tax-free years later.

• After 65, HSA funds can be withdrawn for any purpose taxed as ordinary income (no penalty), and remain tax-free for medical costs and Medicare premiums.

• California doesn’t recognize the HSA’s tax benefits — no state deduction, and earnings are state-taxable — but the federal triple break usually still makes it worthwhile.

Common questions about HSAs

What’s the “triple tax advantage”?

Contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. No other account offers all three.

How much can I contribute in 2026?

$4,400 for individual coverage or $8,750 for family, plus $1,000 more if you’re 55 or older. Employer contributions count toward the limit.

Why pay medical bills out of pocket instead of from the HSA?

To let the HSA invest and compound. There’s no deadline to reimburse yourself, so you can pay now, save the receipt, and reimburse tax-free decades later.

What happens to my HSA after 65?

You can still use it tax-free for medical costs and Medicare premiums, and you can withdraw it for anything else taxed as ordinary income with no penalty — like a traditional IRA.

Do I really owe California tax on my HSA?

Yes. California doesn’t recognize HSAs, so contributions aren’t deductible on your state return and earnings are state-taxable. The federal benefits still apply.

Can I contribute if I’m on Medicare?

No. Once you enroll in Medicare you can’t make new HSA contributions, though you can still spend the balance.

This article is for informational and educational purposes only and is not intended as tax, legal, investment, or financial planning advice. HSA eligibility, contribution limits, and tax treatment can change, and state tax treatment varies — California and a few other states do not follow the federal HSA rules. Investing involves risk, including possible loss of principal. Consult your CPA, tax advisor, and financial advisor about your specific situation before acting.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.