The exemption permanently jumped to $15M per person. For most families, the federal estate tax is no longer the planning issue — but the real estate planning conversation still hasn’t happened.

If you spent the last few years building an estate plan around the looming TCJA sunset, you can exhale. You can also keep working — because the conversation that actually matters didn’t change.

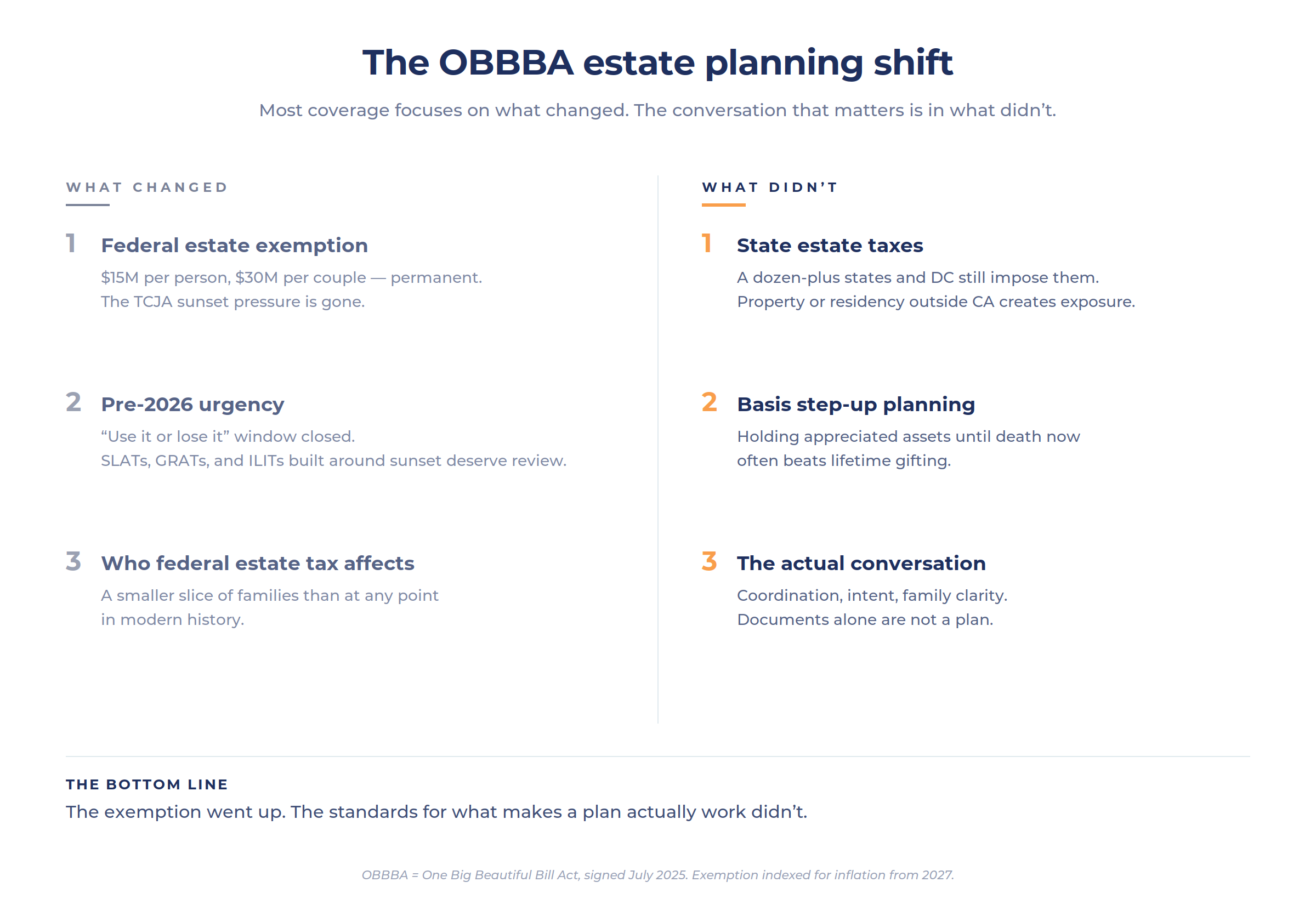

In July 2025, Congress passed the One Big Beautiful Bill Act. Among many other provisions, it permanently raised the federal estate, gift, and generation-skipping transfer tax exemption to $15 million per person — $30 million per married couple with portability — starting in 2026. The exemption is indexed for inflation from 2027 onward. “Permanent,” in tax-law usage, means “until Congress changes it again.” But the snap-back to roughly $7 million per person that was driving so much pre-2026 planning is no longer the timeline you’re working against.

That’s the news. Here’s what most coverage isn’t saying.

Who this actually matters for — and who it doesn’t

The federal estate tax now affects a smaller slice of families than at almost any point in modern history. A married couple with under $30 million in combined estate value generally won’t owe federal estate tax. For perspective, that’s the top fraction of one percent.

For families well above that threshold, transfer planning still matters — but the urgency profile changed. The “use it or lose it” pressure that drove SLATs, GRATs, dynasty trusts, and aggressive gifting strategies across the last several years is gone. Structures created specifically to lock in the higher exemption before sunset should be reviewed: do they still align with current goals, or were they solving a problem that no longer exists?

For families under the new threshold, the more important question isn’t “how do I reduce estate tax?” It’s “what should I actually be planning for?”

What this doesn’t change

State estate taxes. More than a dozen states, plus DC, impose their own estate or inheritance taxes, often with much lower exemptions than federal. California isn’t one of them. But if you own real estate in Oregon, Washington, New York, Minnesota, Massachusetts, or several other states — or if you maintain residency there — the state-level exposure didn’t go away. Estate plans built around federal numbers can miss state-level pitfalls entirely.

Income tax planning. This is where the most underdiscussed shift is happening. For the last decade, sophisticated planning often meant gifting appreciated assets out of the estate before they appreciated further. That move traded estate-tax savings for income-tax cost: the recipient inherits the donor’s original cost basis instead of getting a step-up at death.

With most families no longer facing federal estate tax, the math reverses. Holding appreciated assets until death — and capturing the basis step-up — often beats lifetime gifting. A position you bought for $100,000 that’s worth $1 million today carries $900,000 of unrealized gain. Gift it during life, and the recipient inherits your basis along with the asset. Hold it until death, and the basis resets to fair market value, erasing that embedded tax. The difference at the highest capital-gains rates is significant.

The conversation families still haven’t had. Tax thresholds change. The conversation about what you actually want — who inherits what, when, how decisions get made, what happens if you become incapacitated, whether your children should know what’s in your plan, who has authority over health care and financial decisions — that conversation hasn’t happened in most families. The exemption increase doesn’t change that gap. If anything, the removal of “use it or lose it” urgency creates a new risk: families coasting on the assumption that everything is fine because no tax is owed.

The estate plan that no one understands except the attorney who drafted it isn’t functionally a plan. It’s a document.

Documents do half the work of estate planning. Coordination and clarity do the rest.

What to actually do this year

A few concrete steps for families revisiting their plan in light of the new exemption:

1. Pull out the current plan. If it includes spousal lifetime access trusts, irrevocable life insurance trusts, intentionally defective grantor trusts, or other structures built to use exemption capacity before sunset, ask your estate attorney whether the structures still match where you actually want to end up. Some will. Some were solving the wrong problem.

2. Check state exposure. If you have property or residency outside California — or plan to relocate — review state-level estate tax thresholds. They’re often a fraction of federal and catch families that thought they were “below the limit.”

3. Talk basis planning with your CPA. With step-up at death now the more valuable lever for most families, decisions about whether to gift appreciated assets during life or hold them through death deserve a fresh look. The answer depends on family income tax brackets, the asset’s growth trajectory, and donor circumstances — not just an estate-tax calculation.

4. Have the real conversation. With your spouse, with your adult children if appropriate, with the trustees and agents you’ve named. The most common estate planning failure isn’t a tax mistake. It’s a coordination mistake — heirs who don’t know where documents are, named trustees who didn’t know they were named, family members surprised by decisions that should have been discussed years earlier.

The shift this represents

For most of the last decade, estate planning conversations in our office orbited the same gravitational pull: the TCJA sunset and what to do about it. That pull is gone. What replaces it isn’t “you don’t need estate planning anymore.” It’s a recalibration toward the planning that always mattered more — coordination, intent, basis management, contingency, and the conversations that documents alone can’t substitute for.

The exemption went up. The standards for what makes a plan actually work didn’t.

If your estate plan was built around the sunset, this is a reasonable year to review it. If it wasn’t built around the sunset and hasn’t been reviewed in a few years anyway, that’s the better reason.

Key takeaways

• The federal estate, gift, and GST exemption is permanently set at $15M per person ($30M per couple) starting 2026, indexed for inflation from 2027. The scheduled snap-back to ~$7M is off the table.

• For most families, federal estate tax is no longer the binding planning issue. The urgency that drove SLATs, GRATs, and other transfer-planning structures has changed — existing structures should be reviewed against current goals.

• State estate or inheritance taxes still apply in more than a dozen states plus DC. California residents face no state estate tax, but property or residency elsewhere creates exposure.

• Income tax planning has become the more valuable lever for most families. Holding appreciated assets until death to capture the basis step-up often beats lifetime gifting now that estate tax exposure is gone.

• The conversation that matters most — coordination, intent, family clarity — didn’t change with the exemption increase. Documents alone are not a plan.

- What is the 2026 federal estate tax exemption? Starting in 2026, the federal estate, gift, and generation-skipping transfer tax exemption is permanently set at $15 million per person, indexed for inflation from 2027 onward. A married couple has $30 million in combined exemption capacity using portability.

- Is the increased estate tax exemption permanent? The One Big Beautiful Bill Act, signed July 2025, made the increase permanent — meaning the previously scheduled sunset to roughly $7 million per person no longer applies. "Permanent" in tax law means until Congress changes it.

- Do California residents still need estate planning? Yes. California doesn't have a state estate tax, but estate planning addresses far more than estate tax avoidance — including incapacity planning, trustee designations, basis management, charitable strategies, and family coordination. Residents with property in states that do impose estate or inheritance taxes face additional exposure.

- How does the new exemption affect existing trusts like SLATs and ILITs? Many transfer-planning structures were built to lock in the higher exemption before the scheduled sunset. With the sunset removed, those structures should be reviewed against current family goals. Some will remain valuable; others may have been solving a problem that no longer exists.

- Is gifting appreciated assets still a smart strategy? For families no longer facing federal estate tax, holding appreciated assets until death to capture the basis step-up often beats lifetime gifting. The right answer depends on family tax brackets, asset growth potential, and donor circumstances — and should be reviewed with a CPA.

- What changed under OBBBA besides the estate exemption? The act also locked in TCJA tax rates permanently, raised the SALT cap to $40K (with phase-out above $500K MAGI), expanded QSBS benefits for business owners, preserved the 20% QBI deduction, and introduced a 0.5% AGI floor for charitable contributions.

This article is for informational purposes only and is not intended as tax, legal, or estate planning advice. Estate planning decisions involve complex personal, family, and legal considerations and should be made in coordination with qualified tax and legal professionals. Consult your CPA and estate attorney about how the One Big Beautiful Bill Act provisions apply to your specific situation.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.