For years, the Roth conversion conversation started with a countdown. The 2017 tax cuts were scheduled to sunset after 2025, rates were going up, and the pitch wrote itself: convert now, beat the increase. Then the One Big Beautiful Bill Act made those rates permanent. The countdown clock is gone.

You’d think that would quiet the conversion talk. It shouldn’t — it should improve it. The countdown was always the weakest argument for conversions, because it rested on predicting Congress. The durable case rests on something you can actually measure: the difference between your tax bracket in different periods of your own life.

The argument that survived

A Roth conversion is a trade: pay ordinary income tax on IRA dollars today in exchange for tax-free growth and tax-free withdrawals later. The trade wins when the rate you pay now is lower than the rate those dollars would otherwise face later. Notice what that comparison doesn’t require: any assumption about tax law changing. It only requires your own rate to differ across time. For many retirees, it does — predictably, in four places.

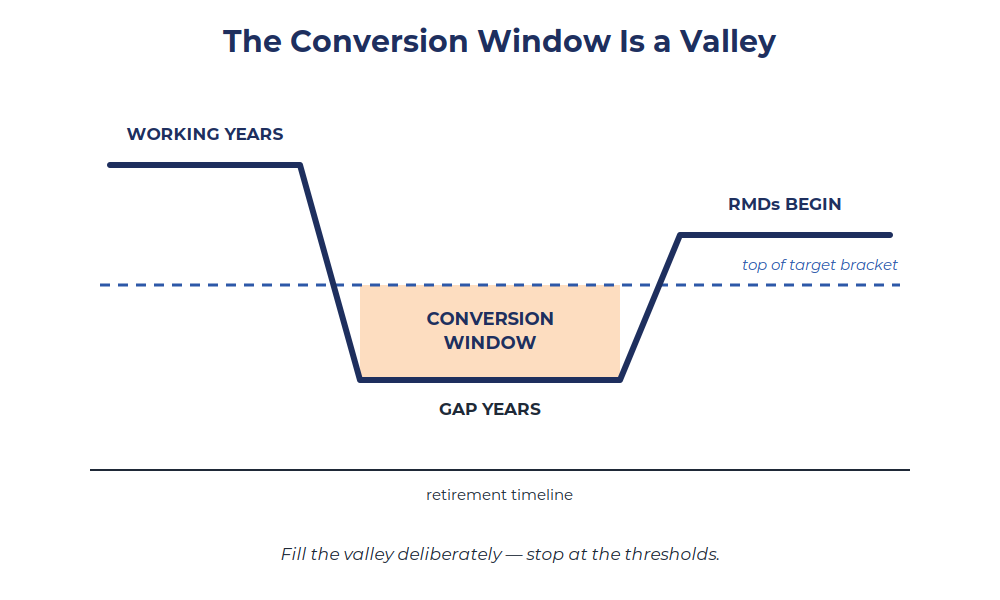

The gap years. Between retirement and required minimum distributions (age 73, or 75 for those born in 1960 or later), many households drop into the lowest brackets they’ll ever see again. Wages stop; RMDs haven’t started; Social Security may be deferred. Those low-bracket years are exactly when conversion dollars are cheapest.

The RMD ramp. Large pre-tax balances compound quietly until RMDs force them out — and force the income whether you need it or not. Converting during the valley shrinks the future balance RMDs are calculated on, flattening the ramp before it starts.

The survivor’s brackets. When one spouse dies, the survivor typically keeps most of the household income but files single — same money, compressed brackets, higher rates. Dollars converted at joint rates today are dollars the survivor won’t be forced to withdraw at single rates later.

The heirs’ brackets. Under the 10-year rule, most non-spouse beneficiaries must empty an inherited IRA within a decade — usually during their own peak earning years. A parent converting at 22% or 24% may be sparing a child a withdrawal taxed at 35%. For families with legacy intentions, this alone can justify conversions that look marginal on a single-generation analysis.

The new wrinkle: OBBBA’s senior deduction

Here’s what changed that most conversion commentary hasn’t caught up with. OBBBA created a temporary bonus deduction of $6,000 per person for taxpayers 65 and older — $12,000 for an eligible couple — available from 2025 through 2028. It phases out at 6% of modified adjusted gross income above $75,000 (single) or $150,000 (joint).

Roth conversions raise MAGI. Which means a conversion inside the phase-out band doesn’t just cost the tax on the conversion — it also claws back deduction dollars, quietly raising the effective marginal rate on those converted dollars above the bracket rate on the page. For a 65-plus couple in the phase-out range, a conversion that looks like a 22% decision can price out meaningfully higher once the lost deduction is counted.

That cuts two ways, and both matter. Through 2028, conversions for eligible retirees need tighter sizing — filling brackets is no longer enough; the phase-out band is part of the map. And because the deduction is scheduled to disappear after 2028, some households genuinely face a lower effective rate on conversions starting in 2029. That’s not a countdown clock; it’s a sequencing question the plan should answer household by household.

The same discipline applies to the other thresholds conversions can trip: Medicare IRMAA surcharges keyed to income from two years prior, and the taxable share of Social Security. None of these make conversions wrong. All of them make sloppy conversions expensive.

What a real conversion analysis looks like

The honest version is unglamorous. Project income year by year through the gap years, RMD years, and a survivor scenario. Map every relevant threshold — bracket edges, the senior-deduction phase-out through 2028, IRMAA tiers, Social Security taxation. Size each year’s conversion to fill cheap space and stop before expensive space. Decide where the conversion tax gets paid from (outside dollars stretch the benefit; withheld dollars shrink it). Revisit annually, because income, markets, and law all move.

Two cautions belong in any honest discussion. Conversions are irreversible — recharacterization was eliminated years ago, so a conversion that turns out to be mistimed can’t be undone. And a conversion never makes sense in a vacuum: it competes with charitable strategies, gain harvesting, and the rest of the tax plan for the same low-bracket space.

Where this fits in a plan

At Via Luce Capital, conversion analysis lives inside the annual planning cycle — modeled against the household’s actual bracket map, coordinated with the CPA who’ll file the return, and revisited every year the window is open. The countdown pitch made conversions sound like a decision you make once, under deadline. The real work is quieter: a measured, multi-year repositioning of retirement dollars from brackets you can predict into brackets you control.

The case for converting was never “rates are going up.” It’s “your rates are uneven — use the cheap years.”

If your retirement plan has never mapped your bracket valley — or hasn’t re-mapped it since OBBBA — that’s a gap worth closing while the cheap years are still ahead of you.

Key takeaways

• OBBBA made the 2017 tax rates permanent, ending the “convert before the sunset” argument — but the durable case for Roth conversions never depended on predicting Congress.

• The real case is bracket arbitrage across your own lifetime: low-bracket gap years before RMDs, joint rates before survivor rates, and your bracket versus your heirs’ under the 10-year rule.

• OBBBA’s temporary senior deduction ($6,000 per person 65+, 2025–2028, phasing out above $75K/$150K MAGI) raises the effective marginal cost of conversions inside the phase-out band — sizing matters more, not less.

• Conversions interact with IRMAA surcharges and Social Security taxation; thresholds, not just brackets, define the map.

• Conversions are irreversible and compete with other strategies for the same low-bracket space — they belong inside an annual, year-by-year analysis, not a one-time decision.

Common questions about Roth conversions after OBBBA

Are Roth conversions still worth it now that rates are permanent?

Often, yes — but for the right reason. The case was never really about tax law changing; it’s about your own rates differing across time. Gap years, RMD compression, survivor brackets, and heirs’ brackets create rate differences no act of Congress is needed for.

How much should I convert in a year?

There’s no universal number. The disciplined approach sizes each year’s conversion to fill low-bracket space and stop before thresholds — the next bracket edge, the senior-deduction phase-out (through 2028), IRMAA tiers. That takes a year-by-year projection, not a rule of thumb.

What is the senior deduction and why does it affect conversions?

OBBBA added a $6,000-per-person deduction for taxpayers 65 and older, from 2025 through 2028, phasing out at 6% of MAGI above $75,000 single / $150,000 joint. Because conversions raise MAGI, converting inside the phase-out band claws back deduction dollars — making the effective rate on those dollars higher than the bracket rate suggests.

Should I wait until after 2028 to convert?

For some 65-plus households in the phase-out band, later years may genuinely be cheaper; for others, waiting wastes low-bracket gap years. It’s a sequencing question the projection answers — not a blanket rule in either direction.

Where should the conversion tax be paid from?

Paying it from outside (taxable) dollars generally preserves more of the conversion’s benefit, since the full converted amount keeps compounding tax-free. Paying from withheld IRA dollars shrinks the transfer — and before 59½ can trigger penalties. This is a detail worth getting right with your advisor and CPA.

This article is for informational and educational purposes only and is not tax, legal, or financial planning advice. Roth conversions are irrevocable, increase taxable income in the year of conversion, and can affect deductions, Medicare premiums, and taxation of Social Security benefits; whether and how much to convert depends on individual circumstances and current law, which may change. Consult your tax professional and financial advisor before acting. Via Luce Capital and LPL Financial do not provide legal or tax advice.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.