The year you sell your business is, almost always, the highest-tax year of your life. It’s also the single best year to do something charitable you may have been meaning to do anyway — and the most time-sensitive. The catch is that the most valuable version of that move has to happen before the deal is binding, not after the wire hits.

A liquidity event — selling the company, a large block of stock, a building — concentrates years of gain into a single tax year. The capital-gains bill can be enormous, and it all lands at once.

If charitable giving is anywhere in your plans — a cause you care about, a family foundation, a donor-advised fund you’ve been meaning to fund — that high-tax year is when a gift does the most work. A deduction is worth the most when your income is highest, and giving away an appreciated asset before it’s sold avoids the capital-gains tax on the portion you give. Done right, the same dollars support a cause you value and cut the tax on the sale.

Done a few months too late, none of it works. The difference between a brilliant move and a missed one is almost entirely about timing.

Why the sale year is the moment

Two things make a business sale the prime charitable window.

First, the deduction is most valuable when your income — and your bracket — is at its peak. A charitable deduction in your highest-income year offsets income taxed at the highest rate. In an ordinary year it’s helpful; in a sale year it’s powerful.

Second, and more important, is what you give. If you donate an appreciated asset — company stock, shares, a business interest — to charity before it’s sold, you generally get a deduction for its full fair-market value, and neither you nor the charity pays capital-gains tax on the appreciation. Donate cash from the after-tax proceeds instead, and you’ve already paid the gains tax before the gift. Giving the asset rather than the cash is what turns a nice gesture into a genuinely efficient one.

The rule that makes or breaks it — give before it’s binding

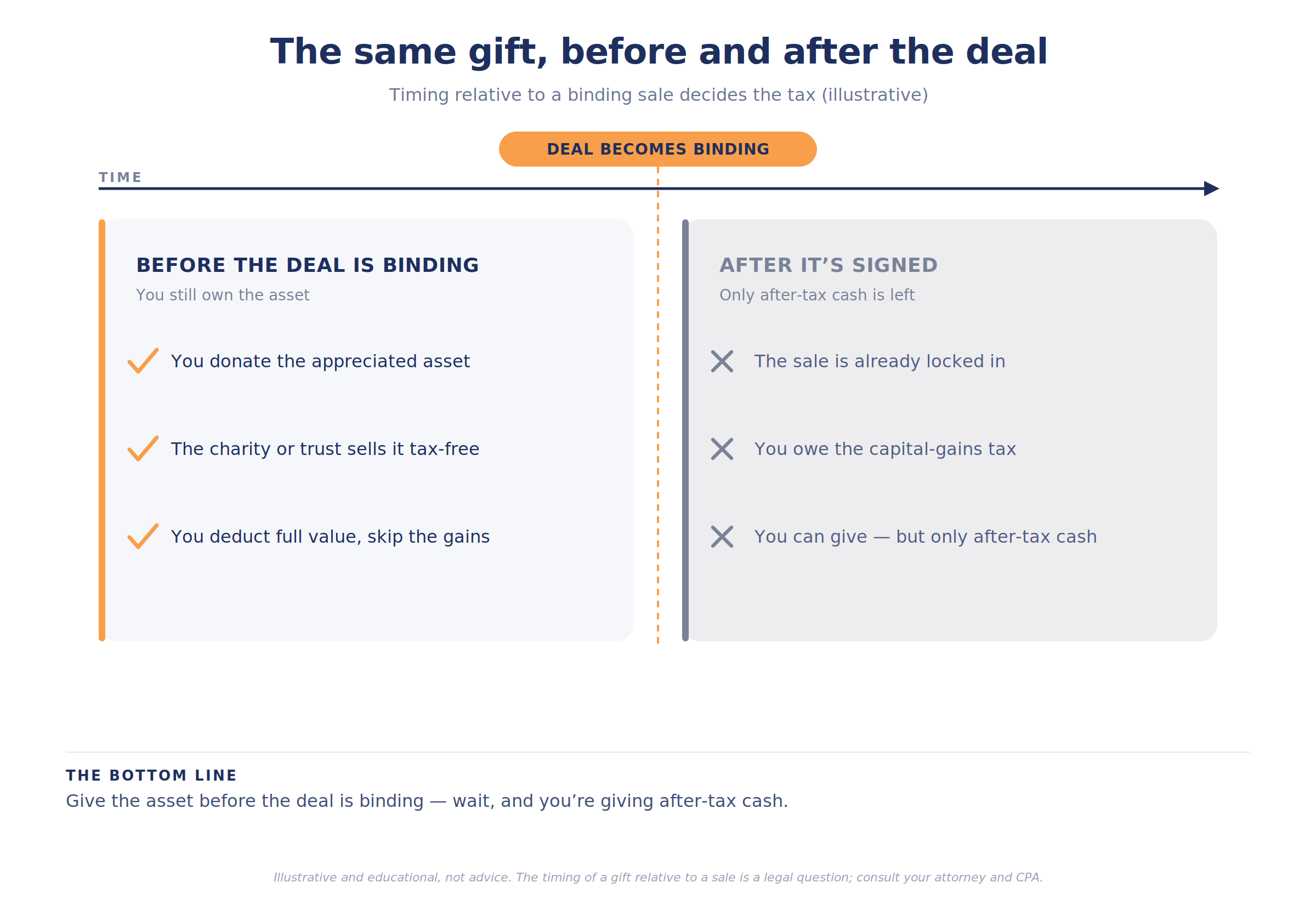

Here’s the timing trap, and it’s the whole game. The gift of the asset has to happen before the sale is locked in.

Tax law looks at substance. If you’ve already signed a binding agreement to sell — or the deal is so far along that the sale is effectively a done thing — and only then donate the shares, the IRS can treat it as if you sold the asset yourself and donated the cash. You’d owe the capital-gains tax anyway, and the central benefit evaporates. The doctrine has names — assignment of income, the step-transaction rule — but the practical lesson is simple: you have to gift the asset while you still genuinely own something that hasn’t yet been sold, not after the deal is wired.

That’s why this is planning, not paperwork. By the time most owners are thinking about charity — at the closing table, or after — the window has closed. The move has to be set up earlier, while the sale is still a plan rather than a signed contract.

Two vehicles — the DAF and the CRT

Two structures do most of this work, and they suit different goals.

A donor-advised fund is the simpler of the two. You contribute appreciated stock or interests to the fund before the sale, take the full deduction in the high-income year, and then recommend grants to charities over time — this year, next year, for decades. It separates the timing of the tax benefit (now, when it’s most valuable) from the timing of the giving (whenever you choose). For an owner who wants to lock in a big deduction in the sale year and decide on the charities later, it’s hard to beat.

A charitable remainder trust does more, and asks more. You contribute the appreciated asset to the trust; the trust can sell it without paying capital-gains tax, and reinvest the full amount. The trust then pays you (or you and your spouse) an income stream for life or a set term, and whatever remains at the end goes to charity. You get a partial deduction up front — the present value of what charity will eventually receive — defer and spread the gain across years of income, and create diversified cash flow from a concentrated, low-basis asset. The trade-offs: it’s irrevocable, it requires an attorney to draft and a trustee to run, and a larger income stream to you means a smaller deduction and less for charity. For the right situation — significant appreciation, a desire for income, and genuine charitable intent — it’s a powerful tool.

Some people use both: a CRT to convert the appreciated asset into lifetime income, with a donor-advised fund named to receive the remainder.

The 2026 wrinkles worth knowing

A few rules shape the math, and two of them are new this year:

• The 0.5% floor. As of 2026, only the portion of your charitable giving above 0.5% of your adjusted gross income is deductible. In a sale year with a very high AGI, that floor is larger in absolute terms — one more reason to make a single substantial gift (which clears it easily) rather than spreading small ones.

• The 35% cap for top earners. Also new in 2026: for taxpayers in the top bracket, the value of itemized deductions is capped at 35% rather than the full 37%. It slightly raises the after-tax cost of giving for the highest earners, but it doesn’t change the core logic — it makes the timing and the choice of asset matter more, not less.

• The AGI limits. Gifts of appreciated assets to public charities and donor-advised funds are generally deductible up to 30% of AGI (60% for cash), with a five-year carryforward for anything above the limit. In a high-AGI sale year, those ceilings are unusually high.

• Private-business complexity. Giving an interest in a private company — rather than publicly traded stock — adds real complexity: a qualified appraisal, entity-specific rules, and extra care around the timing doctrine. It’s very doable, but it’s a coordinated effort, not a do-it-yourself one.

The pattern

Charitable planning at a sale isn’t really about generosity — it’s about timing and structure layered onto generosity you already intended. The giving was always going to happen; the question is whether it happens in the way that also does the most for your tax bill and your income.

And like most of the highest-value moves, it lives upstream of the event, not at it. By the time the deal closes, the best options are gone. The owners who capture this are the ones who treated the sale and the gift as one coordinated plan — CPA, attorney, and advisor at the same table, months before the closing, not after.

The gift you make before the deal is signed avoids the tax. The identical gift made after the wire clears does not. The asset is the same; only the timing changed.

A liquidity event is a once-in-a-lifetime tax event, and that makes it a once-in-a-lifetime planning opportunity. The charitable piece is one of the cleanest parts of it — but only if it’s set up while the sale is still a plan. The work is doing the giving you intended in the way, and at the moment, that makes it count twice.

The plan is the residue. The planning is the work.

Key takeaways

• A business sale is typically your highest-tax year, which makes it the most valuable year for a charitable deduction.

• Donating an appreciated asset before it’s sold avoids capital-gains tax on the donated portion and yields a fair-market-value deduction — far better than donating after-tax cash.

• The gift must happen before the sale is binding; donate after a signed deal and the IRS can tax you as if you sold and gave cash (assignment-of-income / step-transaction).

• A donor-advised fund locks in a big deduction in the sale year and lets you grant over time; a charitable remainder trust adds an income stream and spreads the gain.

• New for 2026: only giving above 0.5% of AGI is deductible, and top-bracket deductions are capped at 35% — a single large gift clears the floor efficiently.

• Appreciated-asset gifts to public charities and DAFs are generally deductible up to 30% of AGI (60% for cash), with a five-year carryforward; private-business gifts add appraisal and complexity.

Common questions about charitable giving around a sale

Why give before selling instead of after?

Donating the appreciated asset before the sale avoids capital-gains tax on the donated portion and gives you a full fair-market-value deduction. Sell first, and you’ve already paid the gains tax before you give.

What happens if I wait until the deal is signed?

The IRS can treat it as if you sold the asset and donated cash, leaving you with the capital-gains bill. The gift generally has to happen before the sale is binding.

What’s the difference between a DAF and a CRT?

A donor-advised fund gives an immediate deduction and lets you grant to charities over time. A charitable remainder trust also pays you an income stream for life or a term, with the remainder going to charity, in exchange for a smaller up-front deduction.

How much can I deduct?

Gifts of appreciated assets to public charities and DAFs are generally limited to 30% of AGI (60% for cash), with a five-year carryforward for the excess.

Did the rules change for 2026?

Yes. Only giving above 0.5% of AGI is now deductible, and top-bracket taxpayers’ deductions are capped at a 35% benefit. A single large gift in a high-income year clears the floor efficiently.

Can I donate an interest in a private business?

Yes, but it’s more complex than donating public stock — it requires a qualified appraisal and careful attention to timing and entity rules. Coordinate with your attorney and CPA early.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. Charitable trusts, donor-advised funds, and gifts of business interests are complex, often irrevocable, and subject to detailed rules on timing, valuation, and deductibility that depend on your specific circumstances. The timing of a gift relative to a sale is a legal question with significant consequences. Consult your CPA, tax advisor, and an estate or tax attorney before acting.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.