Restricted stock units come with two surprises Californians rarely see coming: a tax bill far bigger than what was withheld, and a state that keeps taxing the stock you earned here long after you’ve moved away.

RSUs are taxed when they vest — as ordinary income

Start with the part people most often get wrong. When your RSUs vest, the full value of those shares becomes ordinary income on your W-2 that year — whether or not you sell a single share. Not a capital gain. Not at grant. At vest, taxed at your full ordinary rate, just like salary.

That framing matters, because it sets up everything that follows. A big vest can add six figures of ordinary income in a single year, stacking on top of your salary and pushing you into higher brackets. And the amount your employer sets aside for taxes is usually nowhere near enough.

The withholding gap

Employers withhold federal tax on RSU income at a flat supplemental rate — 22% up to $1 million of supplemental wages, 37% above it — and California withholds at a flat 10.23%. For a lot of people, those numbers sound about right. For high earners, they aren’t close.

A successful professional’s real marginal rate runs much higher: federal tax of 32% to 37%, California up to 13.3%, plus Medicare and California’s disability insurance tax, which now applies to all wages with no cap. Stack those and the combined marginal rate can clear 45%. Withhold 22% federally against a 37% liability and you’ve quietly built a shortfall you’ll discover in April — sometimes with an underpayment penalty attached. The fix is unglamorous: top up your withholding or make quarterly estimated payments, to both the IRS and the Franchise Tax Board.

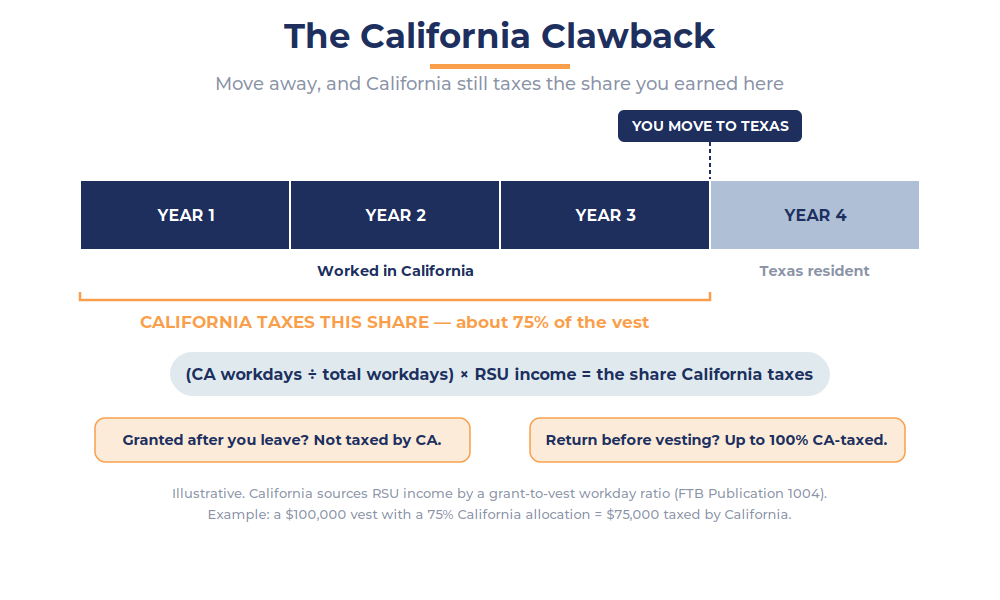

The California clawback

Here’s the one that blindsides people.

California taxes RSU income based on where you worked between the grant date and the vesting date — a simple ratio of California workdays to total workdays over that period. Vest while you live and work in California, and it’s fully California income. But here’s the trap: move to Texas after three of a four-year vesting schedule, and California still taxes roughly 75% of that vest. You earned three-quarters of it here, so California takes its share — even though you were a Texas resident on the day it vested.

This isn’t a gray area. The Franchise Tax Board applies the grant-to-vest workday allocation, and it has been upheld on appeal, including against taxpayers whose stock soared in value after they left. Moving out of state lowers your future tax bill, but it doesn’t erase California’s claim on the income you already earned within its borders. And it cuts the other way too: come back to California before your shares vest, and as much as 100% of that income can land back on a California return.

The double-tax error at sale

There’s a quieter trap waiting at the other end. When you eventually sell vested shares, your cost basis is the value of the stock at vesting — the amount you already paid ordinary income tax on. Only the gain above that counts as a capital gain.

The problem is that brokerage 1099-B forms frequently report a cost basis of zero, or just the (often nominal) amount you paid. Take that number at face value and you’ll report the entire sale price as gain — paying tax a second time on dollars you were already taxed on at vest. It’s one of the most common and most expensive RSU filing errors, and it’s entirely avoidable: check the basis and adjust it to the value at vesting.

How to get ahead of it

The theme across all of this is that none of it is a surprise if you plan for it. A few habits make the difference.

Treat each vest as a taxable event, not a windfall — top up withholding or make estimates so April holds no shocks. Decide deliberately whether to sell at vest or hold: vested RSUs are a concentrated bet on a single stock, often your employer’s, and holding adds both market risk and a second layer of tax to manage. If a move out of California is on the horizon, document your departure carefully and keep a workday log, because every California business trip after you leave adds to your California allocation and raises the share the state can tax. And coordinate the timing of a relocation with your CPA before you go, not after the vests have landed.

Leaving California lowers your future tax bill. It doesn’t erase the state’s claim on the stock you already earned here.

RSUs are genuinely valuable compensation. The mistakes around them come almost entirely from treating each vest as a lump of free money rather than what it is — a planned, taxable event with a few sharp edges that are easy to see coming once you know where they are.

Key takeaways

• RSUs are taxed as ordinary income at vesting — the full value hits your W-2 that year, whether or not you sell.

• Flat withholding (22% federal, 10.23% California) usually falls short of a high earner’s real marginal rate, which can clear 45% — leaving an April shortfall.

• California taxes RSU income by a grant-to-vest workday ratio, so it keeps taxing the California-earned share even if you’ve moved to a no-tax state before the vest.

• Returning to California before vesting can put up to 100% of the income back on a California return.

• At sale, your basis is the value at vesting; 1099-B forms often misreport it, causing accidental double taxation if not corrected.

• Treat each vest as a planned event: top up withholding or pay estimates, decide sell-vs-hold deliberately, and document a relocation with your CPA in advance.

Common questions about RSU taxes in California

When are RSUs taxed?

At vesting, the full value is ordinary income on your W-2 for that year — regardless of whether you sell. A later sale can produce an additional capital gain or loss on any change in value after vesting.

Why do I owe more than was withheld?

Employers withhold at flat rates (22% federal, 10.23% California) that often sit well below a high earner’s true marginal rate. The difference shows up as a balance due — and possibly a penalty — when you file.

If I move out of California before my RSUs vest, do I escape California tax?

Not on the part you earned here. California uses a grant-to-vest workday allocation, so it taxes the share attributable to your California workdays even if you vest as a resident of another state.

What if I move back to California?

Returning before your shares vest can make as much as 100% of that RSU income taxable by California, depending on your workdays during the vesting period.

How do I avoid being taxed twice when I sell?

Confirm your cost basis equals the share value at vesting. Brokerage forms often report it as zero, which would tax you again on income you already paid tax on at vest. Adjust it on your return.

Should I sell my RSUs as they vest or hold them?

That depends on your concentration, your goals, and your tax picture. Holding keeps a single-stock bet on the table and adds tax complexity; selling at vest lets you diversify. It’s a decision worth making deliberately with your advisor and CPA.

This article is for educational purposes only and is not tax advice. Consult your CPA or tax advisor before acting on anything described here.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.