For years, the knock on the 529 was the “what if.” What if your kid gets a scholarship, picks a cheaper school, or skips college entirely? You’d be stuck pulling the money out with a penalty. A 2022 law quietly removed that fear — and in doing so turned the 529 from a single-purpose college account into something far more flexible.

Parents and grandparents who could afford to fund education generously often didn’t — not all the way — because of a nagging worry. Put too much into a 529 and you were making a bet that the child would need exactly that much for school. Guess high, and the leftover money came with strings: withdraw it for anything other than education and you’d owe income tax plus a 10% penalty on the earnings.

So people underfunded on purpose, hedging against a good outcome — a scholarship, a frugal school choice, a kid who chose a different path. The SECURE 2.0 Act, which took effect in 2024, changed the math. Now leftover 529 money has somewhere useful to go: the child’s own Roth IRA.

That single change reframes what a 529 is for. It’s no longer just a college account. It’s an education account with a retirement-savings backstop — and for families with the means, a quietly powerful way to move wealth to the next generation.

The old problem — the 529 was a one-way bet

The 529’s tax deal is excellent: contributions grow tax-free, and withdrawals are tax-free when used for qualified education expenses. The catch was always what happened to money you didn’t spend on school.

Non-qualified withdrawals — taking the money out for anything else — meant income tax on the earnings plus a 10% federal penalty on those earnings. You had workarounds: change the beneficiary to another child or grandchild, hold the account for a future generation, use it for graduate school. But none of them helped the family that had simply set aside more than one kid ended up needing. The fear of that outcome kept a lot of 529s smaller than they should have been.

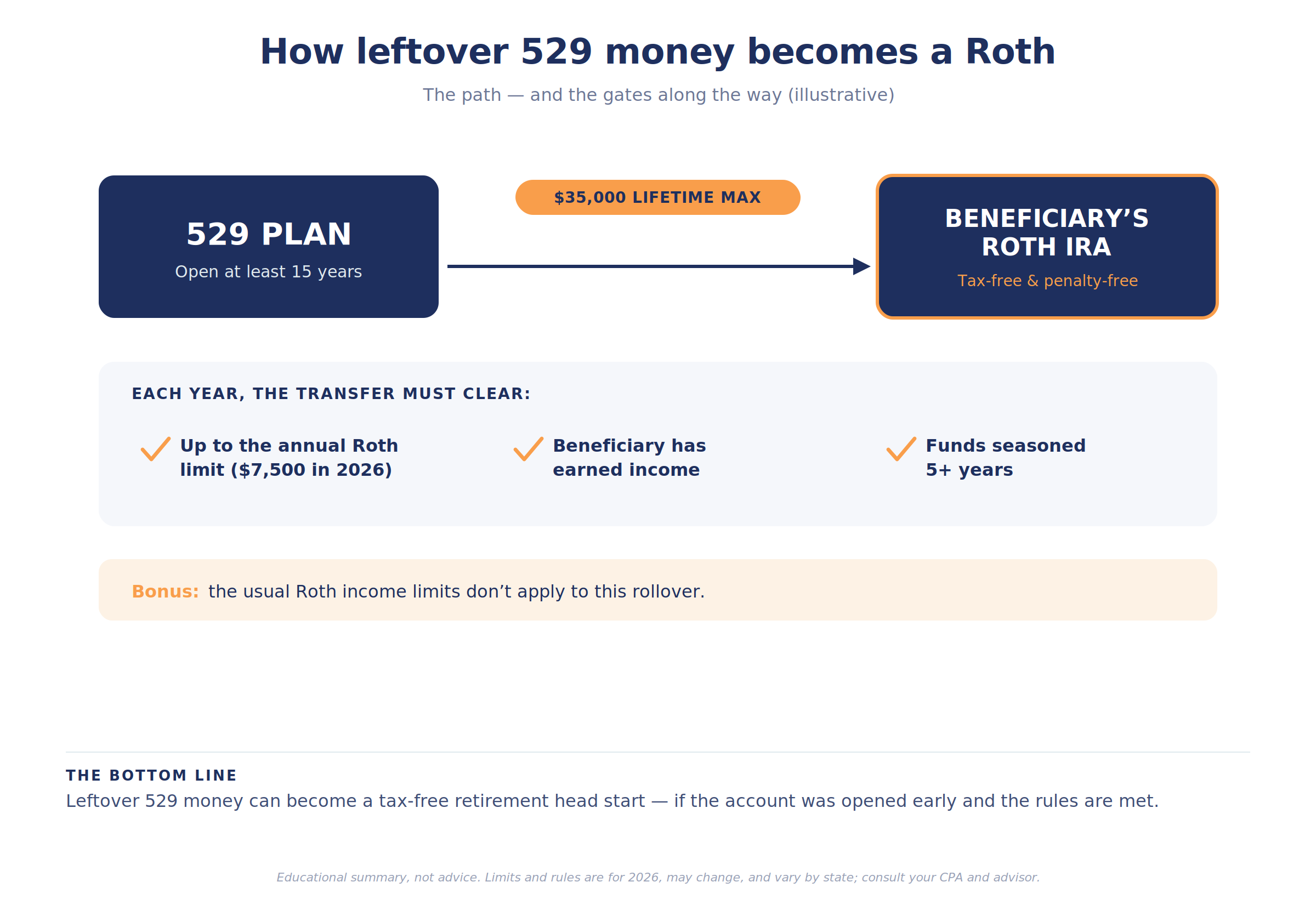

What changed — leftover money can become a Roth

SECURE 2.0 created a new exit. Unused 529 funds can now be rolled directly into a Roth IRA owned by the plan’s beneficiary — tax-free and penalty-free.

The headline number is a $35,000 lifetime limit per beneficiary. That’s not a fortune, but it’s a meaningful head start: $35,000 of Roth money in a 22-year-old’s hands, compounding tax-free for forty-plus years, becomes a substantial retirement asset by the time they’re your age. And because it lands in a Roth, the growth comes out tax-free in retirement. It turns money you were once afraid to contribute into a multi-decade gift.

The rules that trip people up

This is a narrow door, not a backdoor, and the guardrails matter. Get one wrong and a tax-free transfer becomes a taxable one. The key conditions:

• The 15-year rule. The 529 account must have been open for at least 15 years before you can roll anything to a Roth. This rewards opening accounts early — even with modest balances — to start the clock.

• The annual limit. You can’t move the whole $35,000 at once. Each year’s rollover is capped at that year’s Roth contribution limit ($7,500 in 2026, or $8,600 if the beneficiary is 50 or older), so it takes several years to move the full amount.

• The earned-income rule. The beneficiary must have earned income at least equal to the amount rolled that year. A recent graduate with a job qualifies; a child with no income does not.

• The shared cap. The rollover counts against the beneficiary’s own Roth contribution limit for the year. If they already put $3,000 into a Roth from their paycheck, only the remaining room is available for the 529 rollover.

• The seasoning rule. Contributions made to the 529 within the last five years (and their earnings) can’t be rolled. Recent deposits have to wait.

• One genuinely friendly wrinkle: the Roth income limits don’t apply. Normally high earners are phased out of Roth contributions, but that phase-out is waived for 529-to-Roth rollovers — so a well-paid young beneficiary who couldn’t otherwise contribute to a Roth still can through this path.

The other lever — superfunding

The Roth rollover handles the “too much” worry. Superfunding addresses the opposite goal: getting a lot into a 529 quickly, and out of your taxable estate.

Normally, contributions to a 529 count as gifts subject to the annual gift-tax exclusion. Superfunding lets you front-load five years of those gifts at once — up to $95,000 from one person, or $190,000 from a married couple, in a single year — by electing to spread the gift over five years for gift-tax purposes. The money starts compounding immediately, and it’s removed from your estate (one caveat: if you don’t survive the full five years, a prorated portion comes back into the estate).

For grandparents in particular, this is a clean way to move meaningful wealth to grandchildren, put decades of tax-free growth to work sooner, and shrink a taxable estate — all at once. Pair it with the Roth backstop, and the old fear of putting in “too much” largely disappears.

The pattern

The 529 isn’t a college account anymore. It’s an education account that doubles as a retirement head start and an estate-planning tool — and the change rewards exactly the behavior people used to avoid: funding early and funding generously.

That’s the through-line. The 15-year clock rewards opening the account years before you need it. Superfunding rewards moving money in sooner. The Roth backstop rewards funding without fear of overshooting. Every one of these levers pays off for the family that plans years ahead — and does almost nothing for the family that waits until senior year of high school to think about it.

Overfunding a 529 used to be a gamble. Now the leftover money has somewhere to go — and a long time to grow.

The accounts haven’t changed shape so much as the rules around them have, and the rules now reward foresight. Opened early, funded deliberately, and coordinated with the rest of the plan — gift strategy, estate goals, the kids’ eventual incomes — a 529 does far more than pay tuition. The work is setting it up to.

The plan is the residue. The planning is the work.

Key takeaways

• SECURE 2.0 lets up to $35,000 of leftover 529 money roll into the beneficiary’s own Roth IRA, tax- and penalty-free — removing the old overfunding risk.

• The 529 must have been open at least 15 years before any rollover, which rewards opening accounts early.

• Rollovers are capped each year at the beneficiary’s Roth contribution limit ($7,500 in 2026, $8,600 if 50+), so moving the full $35,000 takes several years.

• The beneficiary needs earned income at least equal to the amount rolled, and the rollover shares their annual Roth limit; contributions made in the last five years can’t be rolled.

• Unlike normal Roth contributions, the income phase-out doesn’t apply to 529-to-Roth rollovers.

• Superfunding lets you front-load up to $95,000 (single) or $190,000 (couple) into a 529 in one year, accelerating tax-free growth and reducing your taxable estate.

Common questions about 529-to-Roth rollovers

How much can I roll from a 529 to a Roth IRA?

Up to $35,000 over the beneficiary’s lifetime, but only up to the annual Roth limit each year ($7,500 in 2026), so it takes multiple years.

Whose Roth IRA does the money go into?

The 529 beneficiary’s. The account owner can’t roll it into their own Roth unless they’re also the beneficiary.

What’s the 15-year rule?

The 529 must have been open for at least 15 years before any rollover. There’s also a five-year wait on recently contributed funds.

Does my child need a job to do this?

Yes. The beneficiary must have earned income at least equal to the amount rolled in that year.

What if my child earns too much for a Roth?

The usual Roth income limits don’t apply to 529-to-Roth rollovers, so a high earner can still receive them.

What is superfunding?

Contributing up to five years of annual gift-tax exclusions to a 529 at once — up to $95,000 per person or $190,000 per couple — to accelerate growth and move money out of your estate.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. 529 plan rules, contribution and rollover limits, and gift-tax provisions can change, may vary by state, and depend on your specific circumstances — including state tax treatment and the possible recapture of prior state tax deductions. Consult your CPA, tax advisor, estate attorney, and financial advisor about your situation before acting.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.