The One Big Beautiful Bill Act gave high-tax-state taxpayers their biggest win in years: the SALT deduction cap jumped from $10,000 to $40,000. For a California household paying six figures in combined property and state income tax, that’s real money back.

Then there’s the fine print. The higher cap doesn’t apply evenly — it phases down once modified adjusted gross income crosses $500,000, and it phases down fast. For a specific band of income, the practical effect is a marginal tax rate meaningfully higher than anything printed in the bracket tables. If your income lives anywhere near that band — or visits it in a bonus year, a vesting year, or a conversion year — this is worth ten minutes of your attention.

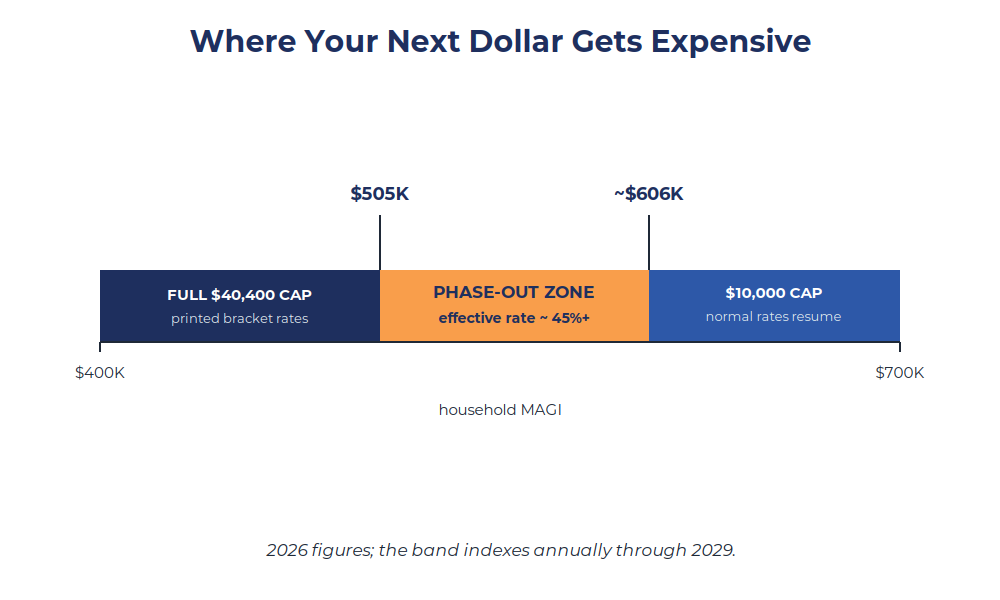

The mechanics

For 2025, the cap is $40,000 with a $500,000 MAGI threshold; both index up about 1% annually through 2029 (for 2026: roughly $40,400 and $505,000). Above the threshold, the cap shrinks by 30% of the income over the line, until it hits a floor of $10,000 — which happens around $600,000 of MAGI. In 2030, under current law, the whole thing reverts to a flat $10,000 for everyone.

So a household at $505,000 keeps the full $40,400. A household around $606,000 or above is back to $10,000. Everyone in between is losing deduction as income rises.

Why the band bites harder than it looks

Follow one extra dollar of income through the phase-out. The dollar itself is taxed at your bracket rate — say 35%. But that same dollar also erases 30 cents of SALT deduction, which means taxable income actually rises by $1.30. At a 35% bracket, the effective federal rate on that marginal dollar is 35% × 1.3 = 45.5%. The same arithmetic at a 37% bracket lands near 48%. That’s before California’s own tax on the dollar, which the federal cap does nothing to reduce.

This is the kind of provision that never shows up in a paycheck and always shows up in April. Nothing on a W-4 or an estimated-payment voucher flags it. The bracket table says 35; the return says otherwise.

Who wanders into the band

Some households live in it. More visit it — and the visitors often have the most control over the timing. Income that arrives in lumps is exactly what pushes a $450,000 year into a $580,000 year: a bonus, a large RSU vest, a strong distribution year from the business, a one-time capital gain, or — note the irony after our last piece — a Roth conversion sized without this phase-out on the map. A conversion that looks sensible against the bracket table can effectively be taxed at 45%+ if it lands inside the band. The senior-deduction phase-out we covered previously and this SALT phase-down are the same lesson twice: post-OBBBA, thresholds matter as much as brackets.

One more wrinkle worth knowing: the band has a far side. At roughly $606,000+, the deduction is fully clawed back, the 1.3 multiplier disappears, and marginal rates return to the printed bracket. The elevated rate is a zone, not a ceiling — which is precisely why timing and sizing decisions matter. Income that must cross the band is often cheapest crossing it decisively in one year rather than camping in it for three.

The planning levers

The response isn’t exotic; it’s sequencing and structure.

MAGI management first: maximizing pre-tax retirement plan contributions — for business owners, potentially a cash balance or defined benefit plan — moves income out of the band directly. Deferred compensation elections, where available, do the same.

Timing second: if lumpy income is coming, model which year it lands in. Two years at $490,000 can beat one at $430,000 and one at $560,000 — same total income, very different deduction outcomes. Roth conversions, gain harvesting, and discretionary distributions should all be sized against the band, not just the brackets.

Structure third, for business owners: most states, including California, offer an elective pass-through entity tax, which lets the entity pay state tax at the company level — where it remains fully deductible against business income, outside the SALT cap entirely. OBBBA preserved this workaround. California’s version has its own election deadlines, payment requirements, and eligibility rules, so this is squarely CPA-coordination territory — but for profitable pass-through owners in the band, it’s often the largest single lever on the board.

And a calendar note: because the enhanced cap runs only through 2029, households safely below the threshold have a five-year window where itemizing works harder than it has since 2017 — worth coordinating with charitable timing while it lasts.

Where this fits in a plan

At Via Luce Capital, this is exactly the kind of provision our annual tax-strategy review exists to catch: it lives in the interaction between income timing, entity structure, and deduction thresholds — territory that belongs to no single document and no single advisor, which is why we coordinate it with your CPA rather than around them.

The rate that matters isn’t the one in the bracket table. It’s the rate on your next dollar.

If your household income sits anywhere between $450,000 and $650,000 — or lands there in your good years — the map of where your next dollar is taxed has changed. Worth knowing before the next bonus, vest, or conversion, not after.

Key takeaways

• OBBBA raised the SALT cap to $40,000 (indexed ~1% annually through 2029), but it phases down by 30% of MAGI above $500,000, hitting the old $10,000 floor around $600,000.

• Inside the phase-out band, each marginal dollar pulls $1.30 into taxable income — turning a 35% bracket into an effective 45.5% federal rate (near 48% at the 37% bracket).

• Lumpy income is the trap: bonuses, RSU vests, capital gains, strong business years, and Roth conversions can push a household into the band unexpectedly.

• The band has a far side — above roughly $606,000 the marginal rate normalizes — so crossing it decisively in one year often beats camping in it across several.

• The biggest levers: MAGI management (retirement plan design, deferrals), income timing, and for pass-through business owners, the state PTET election, which OBBBA preserved.

• Under current law the cap reverts to $10,000 in 2030, making 2025–2029 a five-year window worth planning around.

Common questions about the SALT phase-down

My income is under $500,000 — does any of this affect me?

Not the phase-out. You get the full enhanced cap ($40,400 for 2026), which for many California households means itemizing beats the standard deduction again through 2029 — worth coordinating with charitable and property-tax timing.

My income is well over $600,000 — am I stuck at $10,000?

Yes, the cap is $10,000 once the phase-out completes — but you’re also past the elevated-marginal-rate zone, so additional income is taxed at the printed bracket rate. The zone punishes the band, not everything above it.

How does this interact with Roth conversions?

Directly. A conversion sized only against the bracket table can land inside the band and face an effective rate near 45% or higher. Conversion sizing should map every threshold — this one, the senior-deduction phase-out through 2028, and IRMAA — before the bracket edges.

What is the pass-through entity tax election?

Most states, including California, let a pass-through business elect to pay state income tax at the entity level, where it’s deductible against business income without touching the personal SALT cap. Rules, deadlines, and eligibility vary by state and situation — coordinate with your CPA before electing.

Is the $40,000 cap permanent?

No. Under current law it runs through 2029 (indexed ~1% per year) and reverts to a flat $10,000 in 2030. Planning that depends on the higher cap has a five-year shelf life unless Congress acts again.

This article is for informational and educational purposes only and is not tax, legal, or financial planning advice. Tax figures reflect current federal law, which may change; state rules — including pass-through entity tax elections — vary and carry their own requirements and deadlines. Effective-rate examples are arithmetic illustrations, not projections of any individual’s tax outcome. Consult your CPA and financial advisor regarding your specific situation. Via Luce Capital and LPL Financial do not provide legal or tax advice.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.