An estimated $124 trillion will change hands in the United States by 2048 — the largest intergenerational wealth transfer in history. Most of the families in its path have done the paperwork. Far fewer have done the preparation.

Bank of America’s 2026 Study of Wealthy Americans, surveying households with $3 million or more in investable assets, found that only 36% believe their heirs are very prepared to receive an inheritance. Meanwhile, 61% worry that family wealth could undermine their heirs’ motivation. Read those two numbers together: most wealthy families are planning to hand significant assets to people they don’t consider ready, and they know it.

That gap doesn’t show up in the estate documents. The trust can be flawlessly drafted, the titling clean, the beneficiary designations current — and the transfer can still fail, because documents move assets while preparation determines what happens to them afterward.

The transfer rarely goes where you think it goes first

One detail most families overlook: the majority of wealth doesn’t pass directly to children. It passes horizontally first — to a surviving spouse — and only later to the next generation. That two-stage pattern matters, because the surviving spouse often wasn’t the one managing the financial relationship. Industry research has consistently found that a large majority of heirs change advisors after inheriting, and surviving spouses who were left out of planning conversations move assets at the highest rates of any group.

The lesson isn’t about advisor retention. It’s about what that statistic reveals: when only one person in a household holds the relationships, the knowledge, and the context, everyone else inherits assets without inheriting understanding. That’s the real single point of failure in most estate plans.

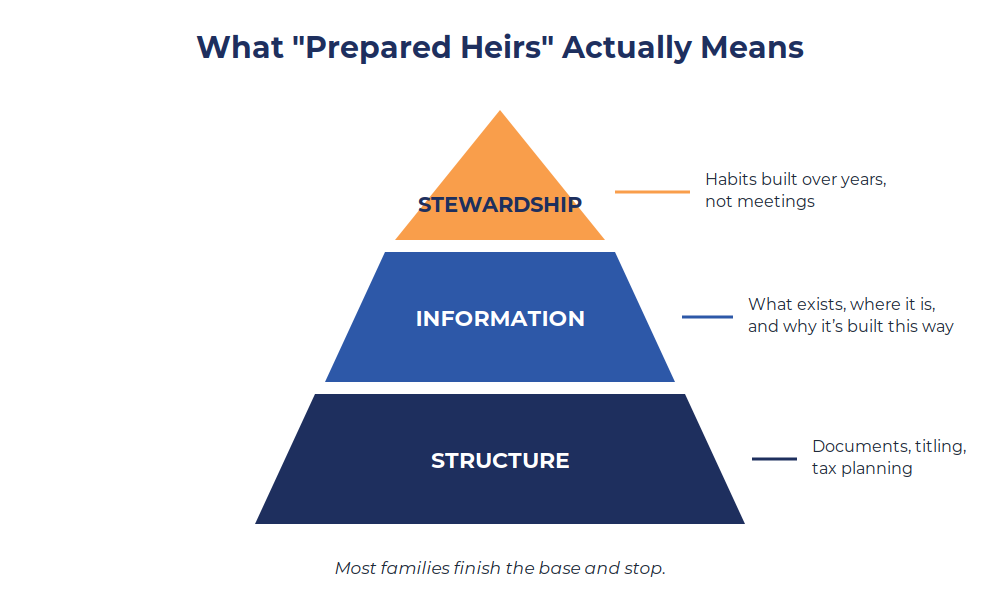

What prepared actually means

Preparing heirs isn’t a single conversation, and it isn’t handing over a binder. In practice, it has three layers.

The first is structural — the documents, the titling, the tax planning. For 2026, the federal estate and gift tax exemption is $15 million per person ($30 million for married couples), and the annual gift exclusion is $19,000 per recipient. Those numbers create room for lifetime gifting strategies that let heirs practice stewardship with real money, at manageable scale, while you’re still here to guide them.

The second layer is informational. Heirs need to know what exists, where it is, who the advisors are, and why the plan is built the way it is. The “why” is the part families skip. An heir who knows a trust exists but not its purpose is far more likely to see it as an obstacle than as protection.

The third layer is behavioral — and it’s the one that takes years, not meetings. Stewardship is a set of habits: understanding how decisions get made, what the family’s capital is for, how to evaluate advice, how to say no. Families that transfer these habits tend to do it deliberately — regular family meetings, defined roles, heirs included in advisor conversations before the wealth ever moves. Families that don’t tend to discover the gap at the worst possible moment.

Start smaller and earlier than feels natural

The instinct is to wait — until the kids are older, until the business sells, until the plan is “final.” The plan is never final, and waiting concentrates the entire education into the period right after a death, which is the worst classroom imaginable.

A more workable sequence: bring the next generation into one advisor meeting a year. Share the structure of the plan before sharing the numbers, if the numbers are the sticking point. Use annual gifts as low-stakes practice rounds. Put the family’s purpose for its wealth in writing — one page is enough — so heirs inherit intent, not just assets.

None of this requires disclosing everything at once. It requires treating the transfer as a multi-year process with a curriculum, rather than an event with a reading of the will.

Where this fits in a plan

At Via Luce Capital, wealth transfer planning sits inside the annual planning cycle, not off to the side of it — coordinated with the estate attorney and CPA, revisited as exemptions, family circumstances, and asset values change. The documents matter. But the families who transfer wealth successfully are the ones who spent as much effort preparing people as they spent preparing paperwork.

Documents move assets. Preparation determines what happens to them afterward.

If the structure is done and the conversations haven’t started, the plan is half-built.

Key takeaways

• Roughly $124 trillion is projected to transfer between generations in the U.S. by 2048, yet only about a third of wealthy families believe their heirs are very prepared.

• Most wealth passes to a surviving spouse before reaching children — households where only one person holds the financial relationships carry the biggest risk.

• Preparation has three layers: structure (documents and tax planning), information (what exists and why), and behavior (stewardship habits built over years).

• The 2026 exemption ($15M individual / $30M married) and $19,000 annual gift exclusion create room to let heirs practice stewardship during your lifetime.

• Treat the transfer as a multi-year process with a curriculum — not an event that begins with a reading of the will.

Common questions about preparing heirs

How much wealth is actually transferring, and when?

Cerulli Associates projects roughly $124 trillion moving between 2024 and 2048, with annual transfers peaking in the mid-2030s. About half is expected to come from high-net-worth and ultra-high-net-worth households.

When should we start talking to our children about the estate plan?

Earlier than feels comfortable. You can share the structure and intent of the plan long before sharing dollar figures. Many families start with one joint advisor meeting per year.

Do we have to disclose everything?

No. Staged disclosure is common and reasonable. What heirs need first is context — what exists, who the advisors are, and why the plan is built the way it is.

What if my spouse isn’t involved in our finances?

That’s the most common and most costly gap. Surviving spouses who weren’t part of planning conversations are the group most likely to inherit assets without inheriting understanding. Bring both spouses into the process now.

Does gifting during my lifetime make sense?

It can — both for estate tax efficiency and as a way to let heirs build stewardship habits at manageable scale. Whether and how much depends on your own liquidity needs, which is a planning question before it’s a tax question.

This article is for informational and educational purposes only and is not tax, legal, or financial planning advice. Estate, gift, and wealth transfer rules are complex, subject to change, and apply differently to each family’s situation. Consult a qualified estate attorney, your CPA, and your financial advisor before acting. Via Luce Capital and LPL Financial do not provide legal or tax advice.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.