The Social Security trustees released their annual report on June 9, and the number that made every headline was 2032. That’s when the trust fund that pays retirement benefits — Old-Age and Survivors Insurance — is now projected to run dry, three months earlier than last year’s estimate. If Congress does nothing before then, incoming payroll taxes would cover about 78% of scheduled retirement benefits. Combine the retirement and disability funds and the date stretches to 2034, with about 83% payable.

Cue two equally unhelpful reactions. The first: “Social Security is going bankrupt — count it at zero.” The second: “Congress always fixes it — count it at 100%.” Both are predictions dressed up as planning. Neither belongs in a serious retirement income plan.

What the report does and doesn’t say

Start with what depletion actually means, because the word does a lot of misleading work. Social Security is funded primarily by payroll taxes, which keep flowing regardless of the trust fund’s balance. Depletion doesn’t mean checks stop; it means the program can pay only what current revenue covers — roughly 78 cents on the scheduled dollar for retirement benefits. A reduction, not a disappearance.

It’s also worth knowing that we’ve been here before. In 1983, with the trust fund months from the same cliff, Congress passed a package of gradual fixes — taxing benefits, slowly raising the retirement age — that bought four decades of solvency. The political pattern is that action comes late, and it comes in the form of adjustments, not rescues or collapses.

None of that is a guarantee. The honest position is that nobody — not the trustees, not the analysts, not your advisor — knows what benefits will look like in 2033. Independent models don’t even agree on the date: Penn Wharton’s latest projection puts depletion in early 2033 rather than late 2032. When credible experts differ on the timing and no one can model Congress, precision is an illusion. Plan accordingly.

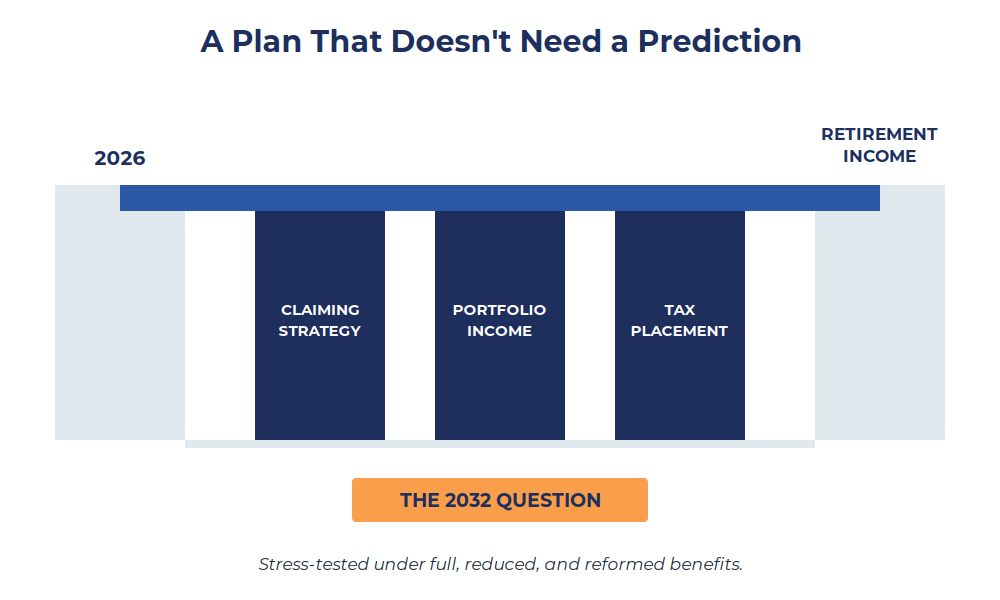

The planning answer: stress-test, don’t forecast

Here’s how we’d frame it inside an actual retirement income plan. Social Security is one income layer among several — portfolio withdrawals, and for some households rental income, deferred compensation, or a pension. The question isn’t “what will Congress do?” It’s “does this plan still work if benefits are reduced?”

That’s a testable question. Run the plan three ways: full scheduled benefits, benefits reduced by roughly the trustees’ shortfall starting in 2033, and a middle path where a fix arrives but trims benefits modestly for higher earners — historically the most likely shape of reform. For most well-funded households, the honest result is that a reduction is absorbable: it changes the withdrawal math at the margins, not the retirement. Knowing that — seeing it modeled, in numbers — is worth more than any prediction, because it converts an anxiety into a line item.

If the plan doesn’t hold up under the reduced-benefit scenario, that’s not bad news. That’s the plan doing its job: telling you now, while there’s a decade of adjustments available — savings rate, retirement date, spending structure, tax placement — instead of in 2033, when there aren’t.

The claiming-age trap

One predictable response to headlines like these: “I’ll claim at 62 and get mine before the cuts.” Sometimes that’s right; usually it’s expensive. Claiming early locks in a permanently reduced benefit — a guaranteed cut of up to 30% — to hedge a possible one. It also shrinks the survivor benefit your spouse may live on for decades, and for households doing Roth conversions in the gap years before required minimum distributions, early Social Security income can crowd out low-bracket conversion room.

The claiming decision should come out of the same stress test as everything else: longevity assumptions, spousal benefits, tax interactions, and yes, a reduced-benefit scenario — weighed together, not driven by a headline. For some households the analysis genuinely favors early claiming. But it should be a conclusion, not a reflex.

Where this fits in a plan

At Via Luce Capital, retirement income planning is scenario-based by design — we’d rather show you how the plan behaves under three futures than pretend to know which one arrives. Social Security’s 2032 question is a perfect example of why.

You can’t control what Congress does. You can control whether your plan requires them to act.

If you’ve never seen your retirement plan run with benefits at 78%, that’s a conversation worth having while the answer can still change something.

Key takeaways

• The 2026 trustees report projects the Social Security retirement trust fund (OASI) depletes in late 2032, after which payroll taxes would cover about 78% of scheduled benefits — a reduction, not a disappearance.

• Both extreme reactions — counting benefits at zero or assuming a full fix — are predictions, not planning.

• The durable approach is a three-scenario stress test: full benefits, reduced benefits, and modest reform. A well-built plan should be able to name its result under each.

• Claiming at 62 to “beat the cuts” trades a possible future reduction for a guaranteed permanent one, and can shrink survivor benefits and Roth conversion room.

• In 1983, Congress resolved the same cliff with gradual adjustments — late action and modest trims are the historical pattern, but a plan shouldn’t depend on it repeating.

Common questions about Social Security’s 2032 question

Will Social Security still exist when I retire?

Under current law, yes. Even if the trust fund depletes as projected, ongoing payroll taxes would fund roughly 78% of scheduled retirement benefits. Depletion means reduction, not elimination.

Should I claim early before benefits are cut?

Not as a reflex. Claiming at 62 permanently reduces your benefit and can reduce your spouse’s survivor benefit. Whether it makes sense depends on longevity, spousal benefits, taxes, and your broader income plan — it’s an analysis, not a hedge.

How should a retirement plan account for this?

By modeling it. Run the plan with full benefits, with the projected reduction starting in 2033, and with a moderate-reform scenario. The goal is a plan that works in all three, not a bet on one.

Didn’t this almost happen before?

Yes — in 1983 the trust fund was months from depletion when Congress enacted gradual fixes, including taxing benefits and raising the retirement age over time. History suggests adjustment rather than collapse, but history isn’t a guarantee.

Does this change Roth conversion planning?

It can. Reduced future benefits would lower taxable income in later years, and early claiming can crowd out conversion room in the gap years. It’s another reason claiming, conversions, and withdrawals should be planned together rather than separately.

This article is for informational and educational purposes only and is not tax, legal, or financial planning advice. Social Security projections reflect current trustee estimates under current law and are subject to change; future legislative action cannot be predicted. Consult your financial advisor and tax professional regarding your specific situation.

Brent Rupnow is a Registered Representative with, and Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.