Most of the advice about Social Security is a contest over a single number: the age you claim. For a married couple with real assets, that’s the wrong number to obsess over. The decision that echoes for decades isn’t when you turn on your benefit — it’s the one you leave behind for whoever lives longer.

Ask most people about Social Security and the conversation collapses into a single debate: claim early at 62, or wait? It gets framed as a bet on your own life expectancy — beat the breakeven age and you win, die early and you lose.

For an affluent household, that framing misses the part that matters most. If you don’t need the check at 62 to pay the bills — and many successful retirees don’t — the decision stops being about maximizing your own lifetime payments and starts being about two things the breakeven math ignores: protecting your spouse, and managing your taxes for the next thirty years.

Handled well, Social Security becomes one more coordinated piece of the plan. Handled as a standalone “when do I claim” question, it quietly leaves money — and protection — on the table.

The number that actually matters — the survivor benefit

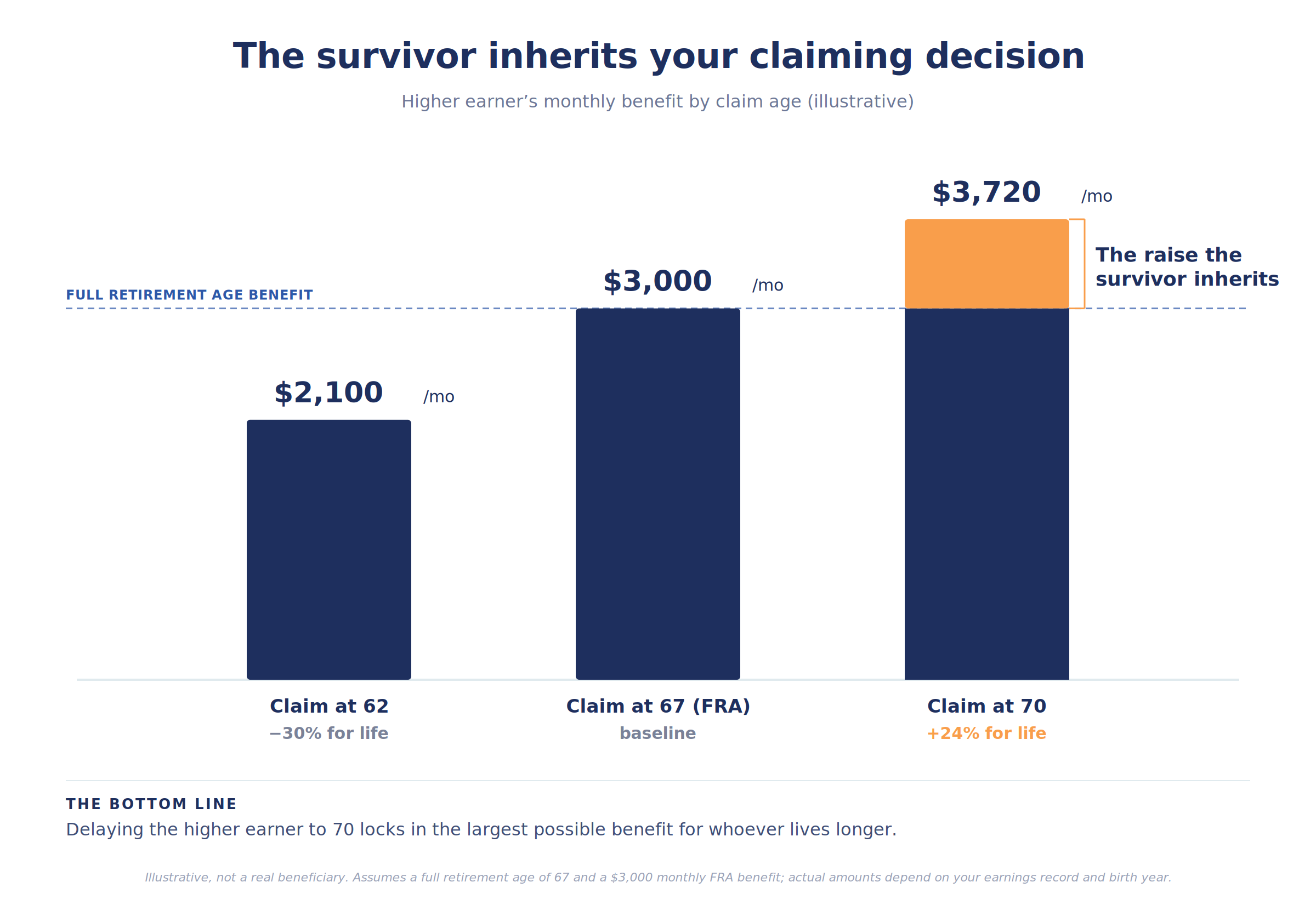

Here’s the rule most couples never hear: when one spouse dies, the survivor receives the higher of the two benefits, not both. The smaller one goes away.

That single fact reframes everything. For a married couple, the higher earner’s benefit isn’t just their own retirement income — it’s the income the surviving spouse will live on, potentially for decades. And every year the higher earner delays claiming, up to age 70, that benefit grows by about 8% — a permanent, inflation-adjusted raise the survivor inherits.

So the highest-value move for many couples is to have the higher earner delay to 70 while the lower earner claims earlier, locking in the largest possible survivor benefit while still bringing in some cash flow along the way. Then, no matter who dies first, that inflated benefit continues for the survivor. It’s not about who lives to the breakeven age. It’s about making sure the one who lives longest is protected.

Delaying isn’t about return — it’s longevity insurance

The objection to waiting is always the same: “But I’m giving up years of checks.” True. And if you view Social Security as an investment to maximize, early claiming can look tempting.

But Social Security isn’t an investment. It’s insurance against the one financial risk you can’t diversify away: living a very long time. The danger in a long retirement isn’t dying early — your plan survives that easily. It’s outliving your money. A larger, inflation-adjusted, government-backed check for life is the cleanest hedge against that risk there is, and the only way to buy more of it is to wait.

For a healthy person who can comfortably fund the gap years from other assets, delaying to 70 isn’t leaving money on the table — it’s buying the most valuable longevity insurance available, at a price a well-funded balance sheet can absorb. For someone in poor health, or without the assets to bridge the gap, the calculus flips, and claiming earlier can be exactly right. The point isn’t that later is always better. It’s that the decision should be made on purpose, against your plan, not by reflex.

The quiet window — claiming late opens room for Roth conversions

There’s a second reason delaying can pay off, and it has nothing to do with the benefit itself.

The years between retiring and claiming Social Security — often the early-to-mid 60s, before required distributions begin — are frequently the lowest-income years of an affluent person’s adult life. No paycheck, no Social Security yet, no forced withdrawals. That low-income window is prime real estate for Roth conversions — moving money from pre-tax accounts to Roth while you’re temporarily in a low bracket.

Turn Social Security on early and you fill that window with taxable income, shrinking the room to convert. Delay it, and you keep the window open — converting at low rates, which then shrinks future required distributions and the Medicare surcharges they trigger. The claiming decision and the tax-diversification work we’ve covered elsewhere in this series aren’t separate projects. They’re the same project.

The taxes nobody warns you about

Two tax realities catch affluent retirees off guard.

First, your benefits are taxable — and for high-income households, heavily so. Up to 85% of your Social Security can be subject to federal income tax depending on your combined income, and the thresholds that determine this are not indexed for inflation. They haven’t been adjusted in almost 40 years. The practical result: nearly every successful retiree pays tax on 85% of their benefit. It’s less a loophole to plan around than a number to build into the projections — though at least 15% of your benefit is always exempt from federal tax no matter what.

Second, if you claim before your full retirement age while still working, an earnings test temporarily withholds $1 of benefit for every $2 you earn above an annual limit. Those dollars aren’t lost forever — your benefit is recalculated upward at full retirement age — but it’s usually a reason for someone still working to simply wait. Once you reach full retirement age, the earnings test disappears entirely.

The pattern

The claiming age isn’t the decision. It’s the visible tip of a set of decisions that run much deeper — survivor protection, longevity insurance, the conversion window, the tax drag — and those are the parts that actually move the outcome.

This is why Social Security doesn’t belong in its own silo, decided the year you turn 62 by a rule of thumb. It belongs in the plan, coordinated with your withdrawal sequence, your Roth strategy, and your Medicare timing — your financial advisor modeling the claiming ages against the rest of the picture, ideally years before anyone files.

For a married couple, the most important Social Security decision isn’t when you claim. It’s the benefit you leave behind for whoever lives longer.

The day you file for Social Security feels like the decision. It isn’t. The decision is everything that led up to it — how you bridged the gap years, what you converted, how you protected your spouse. By the time you file, the planning is either already done, or it isn’t.

The plan is the residue. The planning is the work.

Key takeaways

• For married couples, the survivor keeps only the larger of the two Social Security benefits — so the higher earner’s claiming age sets the income the surviving spouse lives on.

• Delaying benefits up to age 70 raises them by about 8% per year, a permanent, inflation-adjusted increase the survivor inherits.

• Social Security is best understood as longevity insurance, not an investment to maximize — most valuable for healthy retirees who can fund the gap years.

• The low-income years before claiming (and before required distributions) are a prime window for Roth conversions; claiming early shrinks that window.

• Up to 85% of benefits can be federally taxable, and the thresholds were never indexed, so most affluent retirees pay tax on 85%.

• Claiming before full retirement age while still working triggers the earnings test; it disappears once you reach full retirement age.

Common questions about Social Security claiming

When should I claim Social Security?

It depends on your health, marital situation, other assets, and tax picture. For healthy, well-funded couples, delaying the higher earner to 70 is often valuable; for others, claiming earlier can be right. It’s a planning decision, not a fixed rule.

Why does delaying matter so much for married couples?

Because the survivor keeps only the larger benefit. Delaying the higher earner to 70 maximizes the check the surviving spouse will rely on, potentially for decades.

Isn’t waiting just a bet on living longer?

Partly, but it’s better understood as insurance against living a long time and outliving your money — a risk a larger lifetime check directly hedges.

How does claiming affect my taxes?

Up to 85% of benefits can be taxable, and turning benefits on adds income that can crowd out low-bracket Roth conversion opportunities in your early retirement years.

Can I work and collect Social Security?

Yes, but if you claim before full retirement age, an earnings test temporarily withholds part of your benefit above an annual limit. The withheld amount is credited back later, and the test ends at full retirement age.

Is there ever a reason to wait past 70?

No. Delayed credits stop accruing at 70, so there’s no benefit increase for waiting beyond it.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. Social Security rules, benefit amounts, and tax thresholds can change, and the right claiming strategy depends on your specific circumstances. Consult the Social Security Administration, your CPA or tax advisor, and your financial advisor about your situation before making a claiming decision.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.