Most California families assume the house passes down the way it always has — same home, same low property-tax bill, one generation to the next. Since 2021, that assumption has been wrong. And the document most people trust to fix it doesn’t.

For decades, passing the family home to your children in California came with a quiet but enormous benefit: the kids kept your property-tax base. A house bought in 1990 and assessed near $300,000 stayed assessed near $300,000 after it changed hands, even if it was worth seven figures on the open market. The bill barely moved.

Proposition 19 ended that for transfers on or after February 16, 2021. When a home passes to the next generation now, the old protection survives only under a narrow set of conditions — and across much of Orange County, the value of the house all but guarantees that some of it gets reassessed anyway.

The part that catches families off guard isn’t the law itself. It’s the discovery that the living trust they set up years ago — the one they were told would “take care of everything” — has no effect on the reassessment at all.

What Prop 19 actually changed

Before Prop 19, two measures (Propositions 58 and 193) let a parent transfer a principal residence to a child at any value without reassessment, plus up to $1 million of assessed value in other property — rentals, vacation homes, commercial buildings.

Prop 19 replaced that with something far tighter:

• The exclusion applies only to a principal residence. Rentals, vacation homes, and investment real estate are reassessed to full market value when title transfers — no exclusion at all.

• The child has to move in. The home must become the heir’s own primary residence, generally within one year of the transfer.

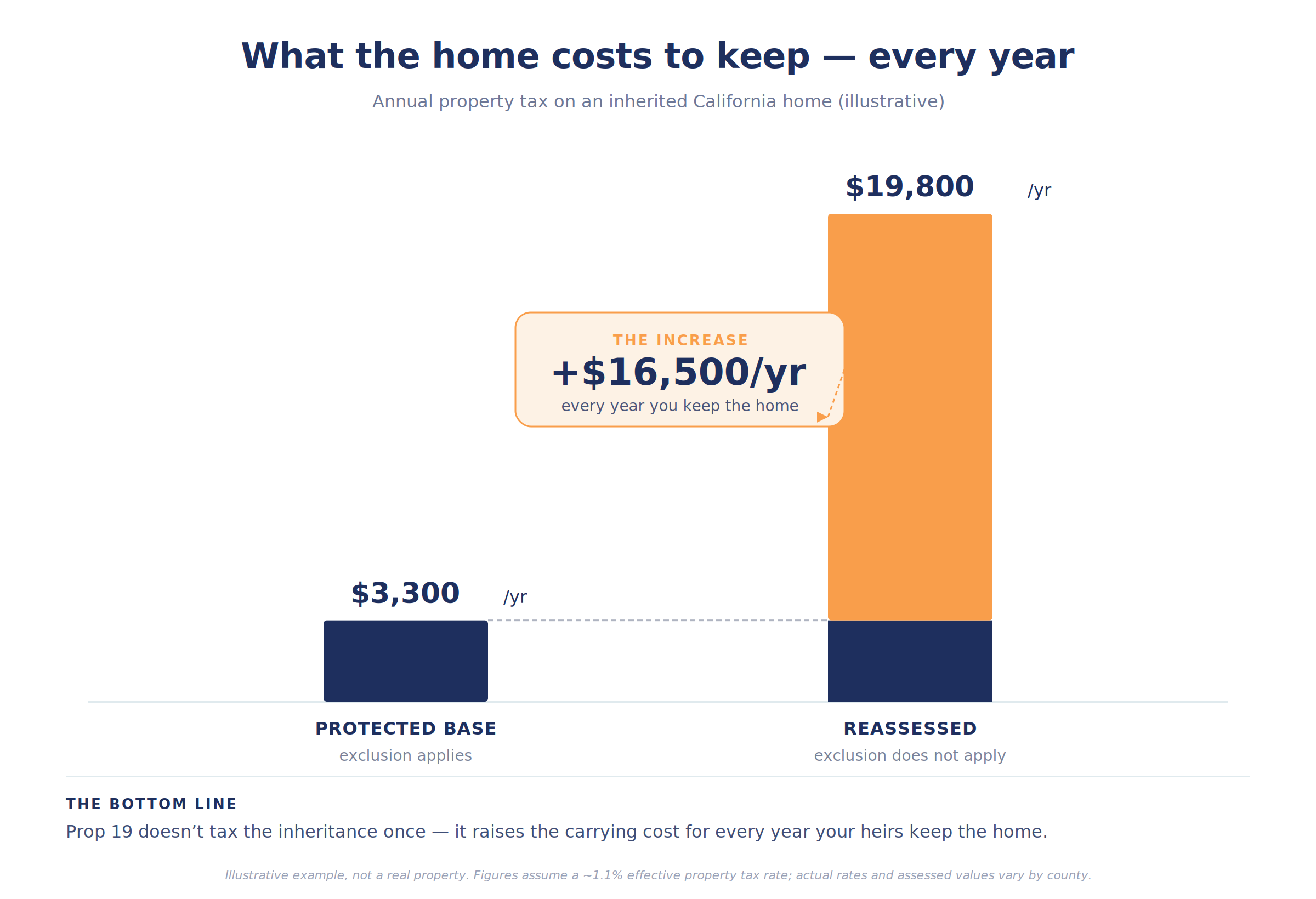

• There’s a dollar cap. Even when the child moves in, the protected amount is the parent’s existing assessed value plus roughly $1 million, a figure adjusted for inflation each year. Anything above that gets added back to the taxable base.

For a long-held OC home, that cap bites. Take an illustrative house assessed at $300,000 but worth $1.8 million at transfer. The protected base lands around $1.3 million, and the rest is reassessed. The new bill settles somewhere between the old one and a full market reset — and it stays there, every year, indefinitely.

Why the living trust doesn’t help

This is the misunderstanding worth correcting directly: a standard revocable living trust does not avoid a Prop 19 reassessment.

A revocable trust is an excellent tool for avoiding probate, keeping the transfer private, and controlling how and when assets pass. But for property-tax purposes, the state looks through the trust to the change in beneficial ownership. When the parents die and the home passes to the children through the trust, that is still a parent-to-child transfer — and Prop 19 applies in full.

The trust controls how the house moves. It does nothing about what the move costs.

The conditions that trip families up

Even families who know the home must become a primary residence lose the exclusion on technicalities:

• Missing the move-in window. The heir has to actually occupy the home as a primary residence within the required timeframe — not eventually, not someday.

• Missing the filing. The exclusion isn’t automatic. The heir has to file a claim (form BOE-19-P) with the county assessor within the deadline. Skip it, and the reassessment stands.

• Assuming a rental qualifies. A home the parents rented out — or one the child plans to rent — gets no exclusion, even if the parents lived there decades earlier.

• Several heirs, one house. When siblings inherit together, generally only one needs to make it a primary residence to protect the base — but the ownership and buyout math gets complicated fast, and the clock keeps running.

None of these are obscure. They’re just invisible until someone is grieving, busy, and unaware there’s a deadline attached to the house.

There’s a repeal effort — but you can’t plan around a maybe

One more wrinkle. A ballot initiative aiming to repeal the inheritance portions of Prop 19 — restoring the old parent-child rules — has been circulating for signatures, with a chance of reaching the November 2026 ballot. Two earlier attempts didn’t qualify.

It might pass. It might not. Either way, it isn’t a plan. A family organizing around a repeal that hasn’t happened is making a bet, not a decision. The sound posture is to plan for the law as it stands and adjust if it changes — not to wait and hope.

What planning actually looks like

Prop 19 isn’t really a tax-form problem. It’s a decision problem, and the decisions are the kind that take time to get right:

• Does anyone in the next generation actually want to live in the house? If not, the exclusion may be beside the point, and the real conversation is whether keeping the home makes sense at all.

• Is a lifetime transfer worth considering? Moving property during life carries its own trade-offs — loss of the step-up in basis at death, possible gift-tax consequences, loss of control — and it is not automatically better. That’s a question for your attorney and CPA, not a default setting.

• Can the heirs carry the cost even with the exclusion? A protected base on a multimillion-dollar home is still a real annual bill. Sometimes the honest answer is that the home gets sold, and the planning is about doing that cleanly and tax-efficiently.

These aren’t questions you answer in the week after a death. They belong in the estate conversation years earlier, coordinated across your attorney (who structures the documents), your CPA (who models the tax), and your financial advisor (who ties it to the rest of the plan).

Your children don’t inherit your property-tax bill. They inherit a decision about whether they can afford to keep the house — and a deadline they may not know exists.

The estate plan you signed is a snapshot. Prop 19 is a reminder that the snapshot isn’t the work. The work is the years of coordinated decisions behind it — who lives where, what transfers when, and whether the math still holds.

The plan is the residue. The planning is the work.

Key takeaways

• Since February 16, 2021, Prop 19 has sharply narrowed California’s parent-child property-tax exclusion.

• The exclusion now applies only to a principal residence the heir moves into as their own primary home (generally within a year) — and even then it’s capped.

• Rental and vacation properties get no exclusion; they’re reassessed to full market value on transfer.

• A standard revocable living trust avoids probate but does not prevent a Prop 19 reassessment.

• The exclusion isn’t automatic; it requires a timely BOE-19-P claim with the county assessor.

• A repeal initiative may reach the 2026 ballot, but planning around an uncertain outcome isn’t a plan — structure for the law as it stands.

Common questions about Prop 19 and inherited homes

Does putting my house in a living trust protect my kids from a Prop 19 reassessment?

No. A revocable trust handles probate, privacy, and control, but the state still treats the transfer to your children as a parent-child transfer subject to Prop 19.

My kids don’t want to live in the house. Is there any exclusion?

Generally no. The current exclusion requires the heir to make the home their own primary residence. If no one will live there, the home is typically reassessed to market value.

What about a rental or vacation property?

Those receive no parent-child exclusion under Prop 19 and are reassessed to full market value when they transfer — even if the parents once lived there.

How much is protected if my child does move in?

The parent’s existing assessed value plus an inflation-adjusted amount of roughly $1 million. Value above that is added to the taxable base.

Is the exclusion automatic?

No. Your heir must file form BOE-19-P with the county assessor within the deadline. Miss it, and the exclusion is forfeited.

Should I just transfer the house to my kids now?

Maybe, maybe not. Lifetime transfers carry trade-offs — including loss of the step-up in basis at death and potential gift-tax issues — and aren’t automatically better. That’s a decision for your attorney and CPA alongside your financial plan.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. Proposition 19 rules, exclusion amounts, and filing deadlines may change, and their application depends on your specific circumstances and county. Consult your estate planning attorney, CPA, and financial advisor about your situation before acting.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.