For a generation of California families, one thing was simple: you could pass the family home to your children without their property taxes jumping. The low base your parents locked in decades ago carried over. Proposition 19 ended that — and replaced it with a narrow exclusion, a one-year clock, and a cap that catches a lot of families completely off guard.

If your estate plan was built before 2021 — or your assumptions were — there’s a good chance it rests on a rule that no longer exists.

Under the old law, a parent could transfer a primary residence to a child with no property-tax reassessment at all, regardless of the home’s value, plus up to $1 million of assessed value in other property. The family home passed down with its Proposition 13 base intact. A house bought in 1985 for $150,000 and worth $1.5 million today kept its tiny tax bill into the next generation.

Proposition 19, which took effect in February 2021, rewrote that. The automatic break is gone. What’s left is a much narrower exclusion with strict conditions — and missing any one of them triggers a full reassessment to current market value. For a long-held California home, that can mean a property-tax bill several times larger, every year, indefinitely.

What Prop 19 actually changed

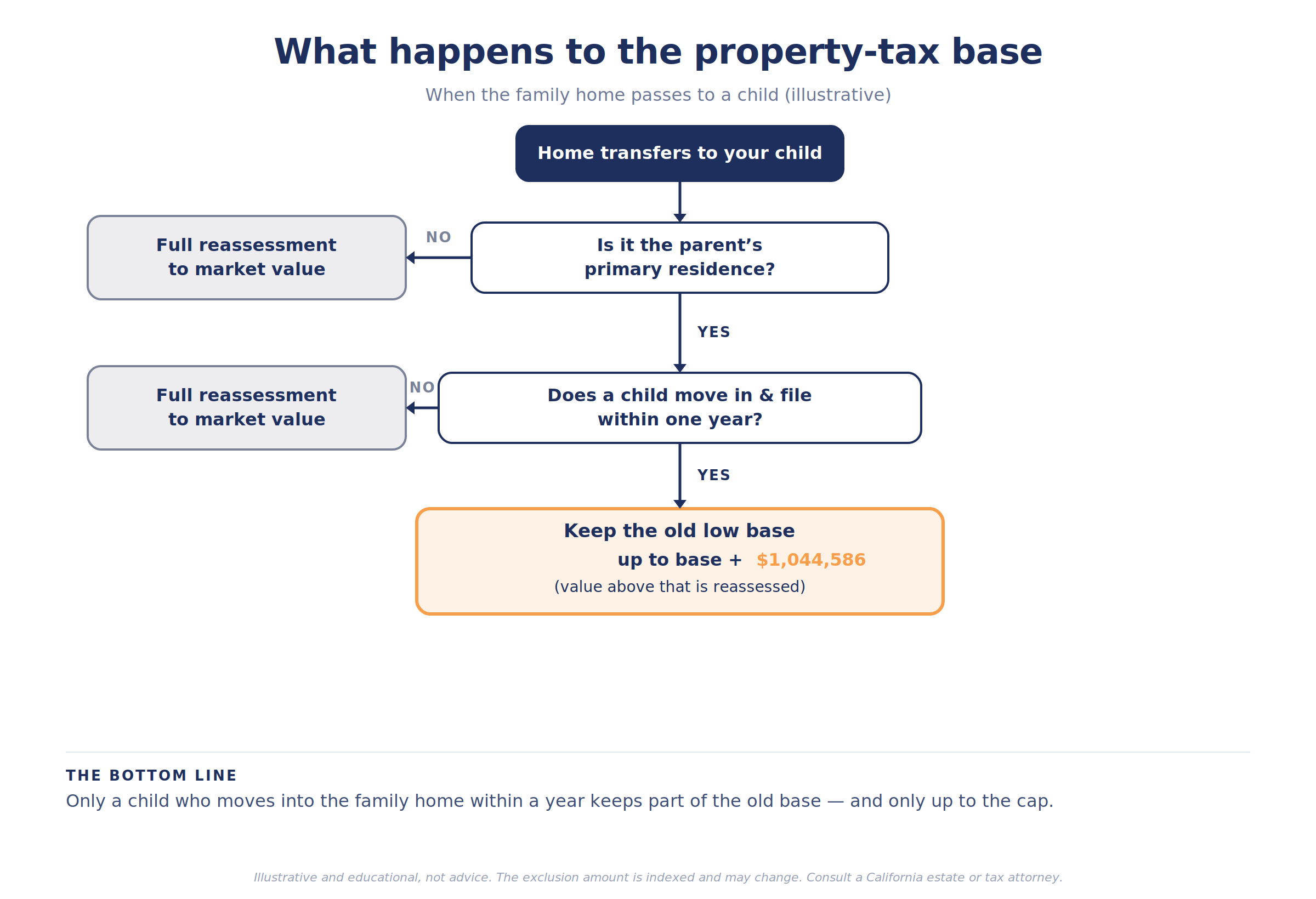

The new rules are tighter in three ways that matter.

• First, it only applies to a primary residence. Under the old law, parents could also pass down rentals, vacation homes, and other property with protection. Under Prop 19, those get no exclusion at all — inherit a rental or a beach house and it’s reassessed to full market value the moment it transfers.

• Second, the child has to move in. The exclusion now applies only if the inheriting child makes the home their own primary residence, and files for it, within one year of the transfer. A child who keeps it as a rental, a second home, or an empty inherited house gets no break — the home is reassessed.

• Third, even when a child does move in, the protection is capped. This is the part almost nobody sees coming.

The cap people don’t see

Even for a qualifying primary residence, Prop 19 doesn’t fully protect the old base anymore. The new taxable value is the parent’s existing assessed value plus roughly $1 million, indexed for inflation — currently about $1,044,586. Anything above that gets added to the tax base.

An example, illustrative: parents bought a home decades ago; its assessed value is now $400,000, but it’s worth $1.9 million today. A child moves in within the year and qualifies. The protected value is $400,000 plus about $1,044,586 — roughly $1.44 million. The remaining ~$460,000 of market value is added to the base. The child keeps part of the old low base, but not all of it — and the tax bill rises accordingly. For higher-value coastal homes, where the gap between the old assessed value and today’s market value is enormous, the reassessed portion can be substantial.

The living-trust myth

Here’s a costly misunderstanding: many people believe that holding the home in a revocable living trust protects it from Prop 19. It doesn’t.

A standard revocable living trust is a probate-avoidance tool. It controls how the home passes, but it doesn’t change the property-tax consequence — when the parents die and the home passes to the children, Prop 19’s reassessment rules apply just the same. The trust gets the home to the kids smoothly; it does nothing about the tax base.

There are more advanced structures — certain irrevocable trusts and lifetime-transfer strategies — that some families use to manage Prop 19 exposure, but they involve real trade-offs (giving up control, gift-tax and step-up-in-basis considerations) and they’re genuinely complex. This is firmly attorney territory, and the right answer depends entirely on the family’s situation. The point isn’t that there’s a magic fix — it’s that the default plan most people have quietly stopped working in 2021.

It’s a decision, not a form

What makes Prop 19 a planning issue rather than a filing issue is the choice it forces on the next generation.

When parents pass, the heirs face a real decision under a one-year clock: move into the family home, make it a primary residence, and file the paperwork to keep part of the old base — or accept the reassessment, which often means a much higher carrying cost, and decide whether to keep or sell. That’s not an administrative step. It’s a financial and family decision, often made in the middle of grief, frequently among siblings with different lives and different interests. A child living out of state, or one who already owns a home, may not be able or willing to move in within a year — and the break is lost.

Those conversations go far better when they happen in advance: understanding who would realistically want the house, what the reassessed cost would be, whether keeping it even makes sense, and how it fits the rest of the estate. The planning is in having the conversation before the clock starts, not after.

A few more things worth knowing

• The benefit side. Prop 19 wasn’t all restriction. It also lets homeowners who are 55 or older, severely disabled, or victims of a wildfire or disaster carry their low base year value to a replacement home anywhere in California, up to three times. For downsizing retirees, that portability can be genuinely valuable.

• Grandchildren. A grandparent can use the same parent-child exclusion to pass a home to a grandchild only if the grandchild’s parent — the grandparent’s child — is already deceased.

• It may change again. There’s an active effort to repeal the inheritance portion of Prop 19 and restore the old rules; a measure could reach the November 2026 ballot. Two earlier attempts didn’t qualify. It’s worth watching, but planning on today’s law — not a hoped-for repeal — is the safer course.

The pattern

The family home is usually the most emotionally loaded asset in an estate and the least deliberately planned. Prop 19 turned what used to be automatic into something conditional — a benefit you now have to qualify for, on a deadline, with paperwork. The trap isn’t the law itself; it’s assuming the old rules, or a living trust, still have you covered.

That’s the through-line again: the document isn’t the plan. A trust that passes the house perfectly can still hand your children a tax bill nobody saw coming, because the property-tax question lives outside the trust. The work is mapping the real decision before it lands on people who are grieving and on a clock.

Under the old rules, the family home passed down with its tax base intact. Under Prop 19, that base survives only if a child moves in within a year — and only up to a cap.

A house can pass to the next generation flawlessly on paper and still become a burden the year it transfers, simply because of a property-tax rule most plans were never updated for. The fix isn’t exotic; it’s a conversation — about who wants the home, what it would cost to keep, and how it fits everything else — held while there’s still time to act on the answer. The work is having it early.

The plan is the residue. The planning is the work.

Key takeaways

• Proposition 19 (effective 2021) ended the automatic parent-child property-tax break; the family home is reassessed to market value unless strict conditions are met.

• The exclusion now applies only to a primary residence the inheriting child moves into — and files for — within one year; rentals and vacation homes get no exclusion at all.

• Even a qualifying home is only protected up to the parent’s assessed value plus about $1,044,586 (indexed); value above that is added to the tax base.

• A revocable living trust does not avoid Prop 19 reassessment; it controls how the home passes, not the property-tax consequence.

• Heirs face a real decision under a one-year clock — move in and keep part of the base, or accept reassessment and decide whether to keep or sell.

• Prop 19 also added portability for homeowners 55+, disabled, or disaster victims; a 2026 ballot effort could repeal the inheritance rules, but planning on current law is safer.

Common questions about Prop 19 and inherited homes

Can my children inherit my low property-tax base?

Only if a child makes the home their primary residence within one year and files for the exclusion — and even then, only up to the parent’s assessed value plus about $1,044,586. Above that, the excess is reassessed.

What about a rental or vacation home?

Those get no parent-child exclusion under Prop 19. They’re reassessed to full market value when they transfer.

Does a living trust protect the home from reassessment?

No. A revocable living trust avoids probate and controls how the home passes, but it doesn’t change Prop 19’s property-tax reassessment.

What if my child lives out of state or already owns a home?

Then moving into the inherited home within a year may not be realistic, and the exclusion is lost — the home is reassessed. This is worth discussing in advance.

Did Prop 19 add any benefits?

Yes. Homeowners who are 55+, severely disabled, or disaster victims can transfer their low base year value to a replacement home anywhere in California, up to three times.

Could Prop 19 be repealed?

There’s an effort to repeal the inheritance portion that could reach the November 2026 ballot, though earlier attempts didn’t qualify. Plan on current law rather than a possible change.

This article is for informational and educational purposes only and is not tax, legal, or financial planning advice. Proposition 19’s rules, exclusion amounts, and filing requirements are complex, change with inflation adjustments, and apply differently to each family’s situation; the law may also change by ballot measure. Property-tax and trust decisions have significant, sometimes irreversible consequences. Consult a qualified California estate or tax attorney, your CPA, and your financial advisor before acting.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.