A lot of successful Californians assume that leaving the state is a matter of buying a house somewhere cheaper and forwarding the mail. It isn’t. California doesn’t tax you for leaving — it taxes you until you can prove you actually left, and that proof is built long before the moving truck arrives.

Plenty of people have made the move out of California in the last few years — to Nevada, Texas, Florida, anywhere without a 13.3% top income-tax rate. The math is obvious. What’s less obvious is how hard the state works to keep you on its tax rolls after you go.

There’s a widespread belief that California has an “exit tax” — a one-time toll for leaving. It doesn’t. A 2020 proposal for an annual wealth tax never became law. But the absence of a formal exit tax is almost beside the point, because the state has something stickier: a residency system that presumes you never really left and puts the burden on you to prove you did.

Get that proof wrong, and California can tax your full income — even income earned after you thought you’d moved — for every year it decides you were still a resident, plus penalties and interest.

There’s no exit tax — there’s something harder to beat

Here’s how the system actually works. California taxes its residents on worldwide income, at rates topping out at 13.3% — the highest in the nation. When a high earner files a final California return and then claims to be a nonresident, the Franchise Tax Board notices. It runs a dedicated effort to flag people who file as residents one year and as nonresidents the next, especially those moving to no-tax states.

And the rules are stacked in the state’s favor. Once you’ve established California as your home, the FTB presumes that’s still true until you prove otherwise — you carry the burden of proof, not the state. There’s a four-year window to audit a filed return, and no time limit at all if you don’t file.

That’s the part people underestimate. Leaving California isn’t a moving decision. It’s a documentation decision.

Residence and domicile — the distinction that decides it

The whole question turns on a word most people use loosely: domicile.

You can have several residences — homes in more than one state. But you have only one domicile: the place you treat as your permanent home, the one you intend to return to. California taxes you as a resident if California is your domicile, no matter where you physically spend your time. Spend enough days here and you can be deemed a resident outright; but even careful day-counting doesn’t save you if your domicile is still, in the state’s eyes, California.

This is why “I spent fewer than six months there” isn’t a magic shield. Days matter, but domicile is a facts-and-circumstances question — where your life actually centers — not a number on a calendar.

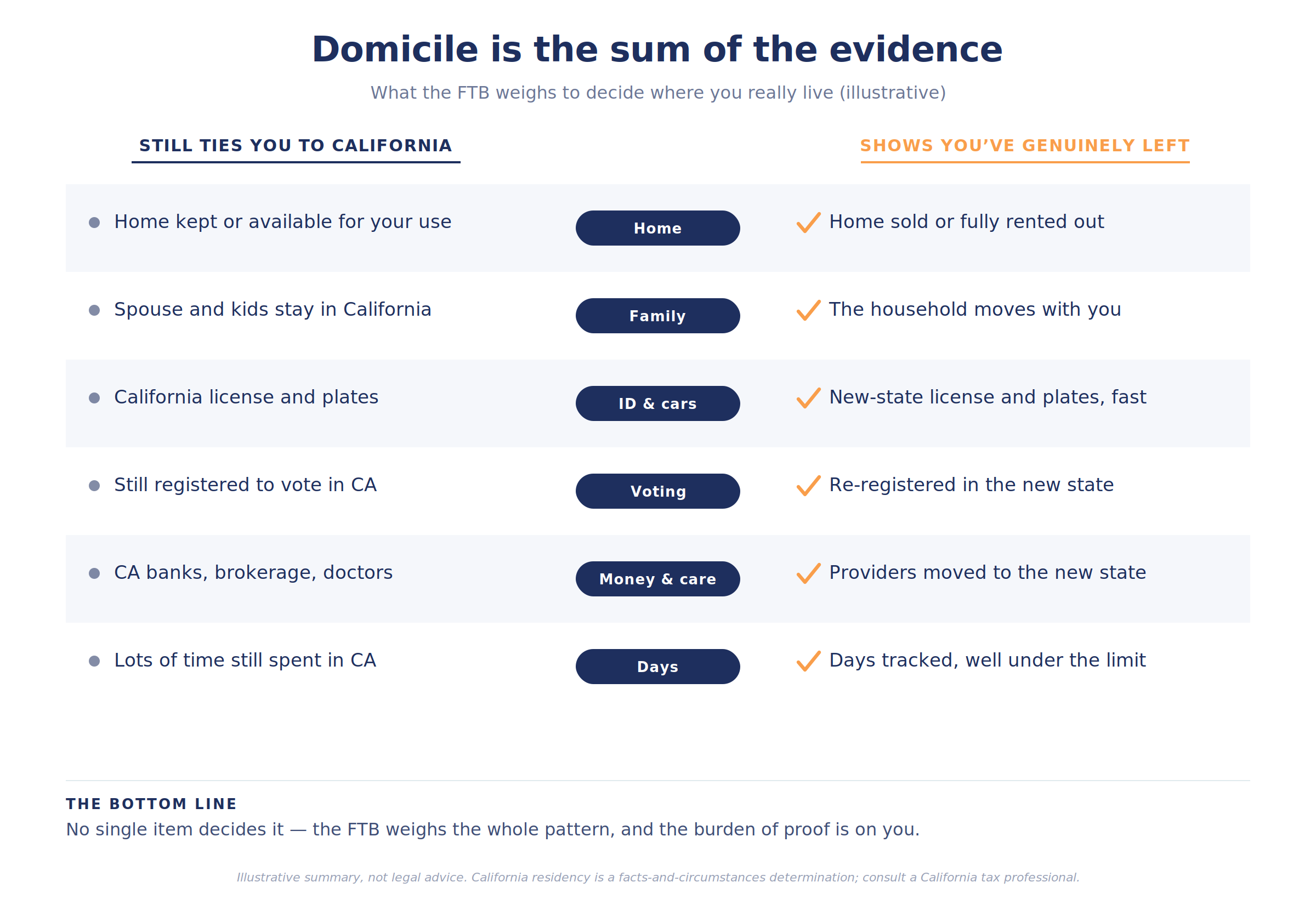

What the FTB actually looks at

A residency audit is an exercise in reconstructing where your life really is, and the state has subpoena power to do it. Auditors have used toll-road records, airline boarding passes, hotel and credit-card statements, cell-phone location data, social media, and even children’s school enrollment to place taxpayers day by day.

The factors that carry the most weight:

• Where your home is — and whether you kept one here. Holding onto a California home, even a rented one, is one of the strongest signals of continued domicile, and a house left available for your personal use is read as intent to stay.

• Where your family is. A spouse and minor children remaining in California pull your domicile toward California.

• The everyday ties. Driver’s license, vehicle registration, voter registration, primary bank and brokerage accounts, doctors and dentists, professional licenses — these are among the first records the FTB requests, and they carry real evidentiary weight.

The pattern matters more than any single item. A new Texas license means little if your family, your home, and your doctors are all still in Newport Beach.

The mistake that costs the most — leaving after the gain, not before

Here’s the timing trap that turns a clean move into an expensive one. The window to escape California’s tax on a big gain closes before the gain happens, not after.

Say a major liquidity event is coming — a business sale, a large stock position, deferred compensation paying out. If you’re still a California resident when that income is recognized, California taxes it, full stop. Moving the following year doesn’t help; you needed to have genuinely changed domicile before the income hit. And some income stays California’s regardless: California-source income — rental income from a California property, income from a California business — remains taxable here even after you’ve left.

This is why the move has to be planned around the calendar of your income, not just your address. Establishing a defensible new domicile is a deliberate, documented pattern of behavior that takes time to build — and it has to be in place before the year that matters, not assembled after an audit notice arrives.

The pattern

Leaving California isn’t a single act. It’s a body of evidence, built on purpose, over time. The people who get tripped up treat it as a change of address; the people who do it cleanly treat it as a change of life, documented as they go — and timed around the income events that actually move the needle.

It’s also a coordination problem. The decision touches your CPA (who models the tax and the timing), an attorney (who updates the trust, will, and powers of attorney to your new state), and your financial advisor (who ties it to the liquidity event, the portfolio, and the rest of the plan). None of them can fix it alone, and none of them can fix it after the fact.

California doesn’t tax you for leaving. It taxes you for not proving you left — and the proof is built before you go.

A move across state lines changes a lot, but it shouldn’t reset your plan to zero. The strategy that made sense in California — the tax coordination, the liquidity planning, the estate documents — has to travel with you and adapt to the new state’s rules. The work isn’t the move. It’s making sure the plan keeps up with it.

The plan is the residue. The planning is the work.

Key takeaways

• California has no formal exit tax, but it taxes residents on worldwide income up to 13.3% and aggressively audits high earners who leave.

• Once California is your domicile, the state presumes you’re still a resident until you prove you’ve established a new domicile elsewhere — the burden of proof is on you.

• Residency turns on domicile (your one permanent home), a facts-and-circumstances test, not just a day count.

• The FTB reconstructs where your life really is using records from toll roads and flights to bank accounts, doctors, and children’s schools.

• Keeping a California home — even a rented one — is one of the strongest signals that you never truly left.

• The window to avoid California tax on a big gain closes before the income event, not after; some California-source income stays taxable regardless.

Common questions about leaving California

Does California have an exit tax?

No formal one. A proposed wealth tax didn’t become law. The real cost comes from residency audits that can tax your income as if you never left.

How does California decide if I’m still a resident?

Primarily by your domicile — the one place you treat as your permanent home — judged on the full facts of your life, not just how many days you spent in the state.

If I keep my California house, is that a problem?

It’s one of the strongest signals of continued domicile, especially if it’s available for your personal use. Selling or genuinely renting it out (not keeping it available) helps show you’ve left.

What does the FTB look at in an audit?

A wide range: driver’s license, voter registration, where your family lives, bank and brokerage accounts, doctors, professional licenses, and even travel and phone records to place you day by day.

I’m selling my business or exercising a big stock position. When should I move?

Generally well before the income is recognized. If you’re still a California resident when the gain hits, California taxes it. The planning has to happen before the event, not after.

Once I leave, is all my income free of California tax?

No. California-source income — such as rent from California property or income from a California business — generally remains taxable by California even after you become a nonresident.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. California residency and domicile rules are complex, fact-specific, and subject to change, and the consequences of getting them wrong can be significant. Consult a qualified California tax professional, an attorney, and your financial advisor about your specific situation before making any move.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.