For most of the last few decades, homeowners insurance was the most boring line item in your financial plan — a bill you paid and never thought about. In California, it isn’t boring anymore. The market has been upended, and for a lot of families the policy they assumed was permanent has quietly become a problem.

If you own a home in California — especially a higher-value one, or one anywhere near a hillside or wildland — you’ve felt some version of this: a steep renewal increase, a non-renewal notice, or a letter steering you toward the state’s insurer of last resort. You’re not imagining a trend.

Nearly 400,000 policies have been canceled across the state since 2021, and seven of California’s top twelve insurers have pulled back or stopped writing new business. The state’s FAIR Plan — the bare-bones backstop meant to be temporary — has become one of the largest “insurers” in California, with enrollment up sharply in barely over a year.

The instinct is to treat this as a billing problem: rates went up, shop around, move on. That misses the more important issue. For many families, the bigger risk isn’t the premium — it’s a gap in coverage they don’t realize they now have.

What happened to the market

A few forces collided. Years of large wildfires, capped by the January 2025 fires that caused tens of billions in insured losses, pushed insurers’ costs past what they could charge under California’s old rules. For decades, a 1988 law — Proposition 103 — effectively barred insurers from pricing on forward-looking catastrophe models; they could lean only on historical losses. As fire risk climbed, the math stopped working, and carriers responded the only way they could: not renewing, not writing new policies, and retreating from higher-risk areas.

Regulators have started to respond. New rules now let insurers use forward-looking catastrophe models in setting rates for the first time, and a slate of laws that took effect January 1, 2026 created mitigation-discount frameworks and extended non-renewal protections. The idea is that letting carriers price risk accurately coaxes them back into the market. It’s a real shift — but it’s early, and in the meantime the squeeze is on.

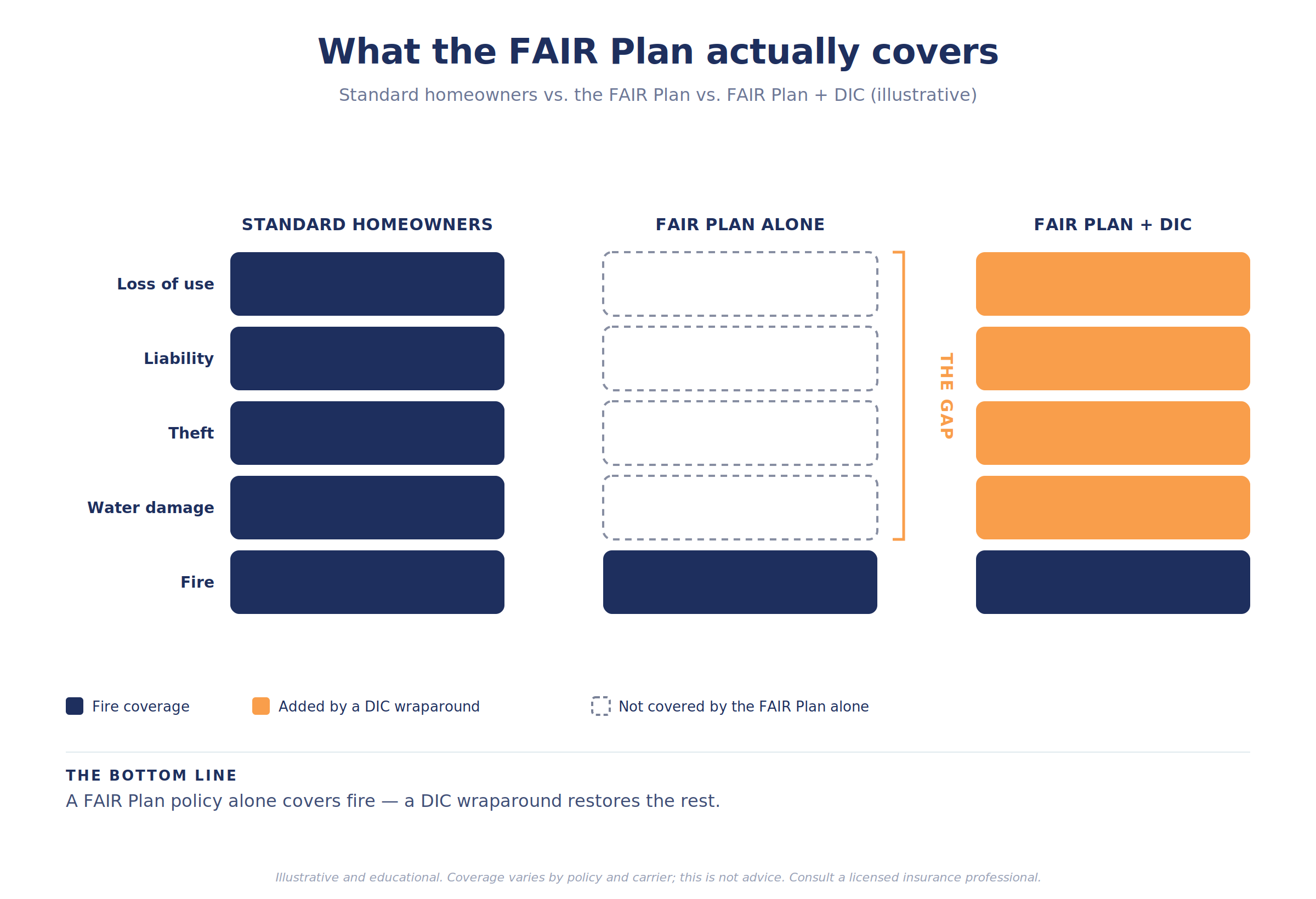

The FAIR Plan isn’t homeowners insurance

Here’s the part that catches people off guard. When private coverage disappears, most people land on the California FAIR Plan — and they assume it’s a like-for-like replacement. It isn’t.

The FAIR Plan is the insurer of last resort, and by design it’s bare-bones: it covers fire and a few related perils, and not much else. A standard homeowners policy bundles things you may never think about — theft, water damage, personal liability if someone is injured on your property, and the cost of somewhere to live while your home is repaired. The FAIR Plan generally doesn’t. To rebuild something like a normal homeowners policy, you pair the FAIR Plan with a separate “difference in conditions” (DIC) policy that fills in everything the FAIR Plan leaves out.

If you’re on the FAIR Plan without a DIC wraparound, you may be carrying far less protection than you think — fire coverage, and a hole where the rest of your policy used to be. And for higher-value homes there’s a second problem: the FAIR Plan caps how much dwelling coverage it will write, and many homes are worth more than that cap. Above it, you’re into surplus-lines and layered coverage to reach full replacement cost.

Why this is a planning problem, not just a bill

Insurance sits at the foundation of a financial plan for a simple reason: it’s what keeps a single bad event from undoing everything else. When the coverage cracks, the cracks run through the whole plan. Three exposures matter most:

• The coverage gap itself. A fire-only policy on a home that needs full replacement coverage — or a policy whose limits haven’t kept up with construction costs — means you’d absorb the difference yourself. For a high-value home, that difference can be enormous.

• Liability. Affluent families usually carry an umbrella policy for liability protection, and that umbrella sits on top of the homeowners policy. If the underlying policy thins out or disappears, the umbrella can have nothing to attach to — leaving a liability gap exactly where you have the most to lose.

• The ripple into everything else. Premiums that jump by thousands hit cash flow. Coverage problems hit home value, complicate a sale, and can stall financing — buyers now factor five figures of annual insurance cost into their offers, and some lenders won’t close without adequate coverage in place.

None of that shows up on the premium notice. It shows up later, at the worst possible moment.

What you can actually do

This is manageable, but it takes treating coverage as a live part of the plan rather than a set-and-forget bill:

• Know what you actually have. Read the policy — or have someone read it with you — and confirm whether you have true homeowners coverage or fire-only, and whether your dwelling limit reflects today’s replacement cost rather than what you paid years ago.

• Close the gap. If you’re on the FAIR Plan, a DIC wraparound restores the liability, theft, water, and loss-of-use coverage it doesn’t include. For high-value homes, that may mean layered or surplus-lines coverage to reach full replacement.

• Harden the home. Mitigation now pays in dollars: fire-safe roofs, defensible space, and ember-resistant work can qualify for premium discounts, and some carriers will even guarantee renewal for homes that earn a recognized “wildfire prepared” designation. It’s one of the few levers genuinely in your control.

• Coordinate the umbrella. Make sure your liability umbrella still has a qualifying underlying policy beneath it, and that the limits line up.

This is exactly the kind of thing a financial plan is supposed to catch — and it’s worth coordinating a coverage review with the rest of the plan rather than handling it in isolation.

The pattern

Homeowners insurance was the part of the plan you were allowed to ignore. That’s the part that changed. The premium increase is the visible symptom; the coverage gap is the real risk, and it stays invisible until something forces it into the open.

That’s the through-line in so much of this: the damage usually hides in the part nobody was looking at. Insurance isn’t the exciting corner of a financial plan, but it’s the corner that keeps one bad day from rewriting all the others. In this market, “I’ve had the same policy for years” is no longer a reason to relax — it’s a reason to check.

The premium increase is the part you can see. The coverage gap is the part that costs you — and it stays hidden until the day you need the policy to work.

California’s insurance market may settle as carriers learn to price the new risk and slowly return. Until it does — and even after — the move is the same: know what you’re actually covered for, close the gaps deliberately, and treat the policy as a living part of the plan instead of a bill you file away. The work is looking before you’re forced to.

The plan is the residue. The planning is the work.

Key takeaways

• California’s home insurance market is in crisis: hundreds of thousands of non-renewals since 2021, sharp premium increases, and rapid growth of the state’s FAIR Plan.

• The FAIR Plan is the insurer of last resort and is bare-bones — generally fire and a few related perils, not the theft, water, liability, and loss-of-use coverage a standard homeowners policy includes.

• To approximate real homeowners coverage on the FAIR Plan, you pair it with a separate “difference in conditions” (DIC) policy; high-value homes may also need layered or surplus-lines coverage above the FAIR Plan’s caps.

• The biggest risk usually isn’t the premium — it’s an unnoticed coverage gap, including a liability umbrella left without a qualifying underlying policy.

• Home hardening (fire-safe roof, defensible space, ember-resistant work) can now earn premium discounts and, in some cases, renewal guarantees.

• Treat coverage as a live part of your financial plan: confirm what you actually have, check that limits reflect today’s replacement cost, and coordinate with your umbrella.

Common questions about California’s insurance crisis

Is the FAIR Plan the same as homeowners insurance?

No. It’s the insurer of last resort and covers mainly fire and a few related perils. It generally doesn’t include theft, water damage, liability, or loss-of-use — which is why people pair it with a separate “difference in conditions” policy.

Why did my insurer non-renew me?

Years of large wildfire losses pushed carriers’ costs past what they could charge under California’s older pricing rules, so many pulled back from higher-risk areas. It often isn’t about your home specifically.

What is a “difference in conditions” (DIC) policy?

A wraparound policy that fills in the coverage the FAIR Plan leaves out — liability, theft, water damage, loss-of-use — so that, combined, you approximate a standard homeowners policy.

My home is worth more than the FAIR Plan will cover. Now what?

The FAIR Plan caps dwelling coverage, so high-value homes often need layered or surplus-lines coverage above that cap to reach full replacement cost.

Can I lower my premium?

Possibly. Home-hardening measures like a fire-safe roof, defensible space, and ember-resistant upgrades can qualify for discounts, and some carriers will guarantee renewal for homes that earn a recognized wildfire-prepared designation.

How does this affect selling or refinancing?

Coverage problems can complicate both. Buyers now factor high insurance costs into offers, and some lenders won’t close without adequate coverage in place.

This article is for informational and educational purposes only and is not insurance, tax, legal, or financial planning advice, and is not a recommendation of any insurance product, carrier, or coverage. Insurance availability, pricing, coverage terms, and California regulations are changing rapidly and vary by property and circumstance. Consult a licensed insurance professional and your financial advisor about your specific situation before making coverage decisions.

Brent Rupnow is a Registered Representative with, and Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.