When you leave a job or retire, the standard advice is to roll your entire 401(k) into an IRA. For most of what’s in the account, that’s fine. For one specific thing — appreciated stock in the company you worked for — it can quietly cost you a fortune in unnecessary taxes, and once it’s done, there’s no going back.

Plenty of long-tenured employees retire with a meaningful slug of company stock sitting inside their 401(k). They bought it through the plan for years, often at a low price, and watched it grow. By the time they leave, the embedded gain can be enormous.

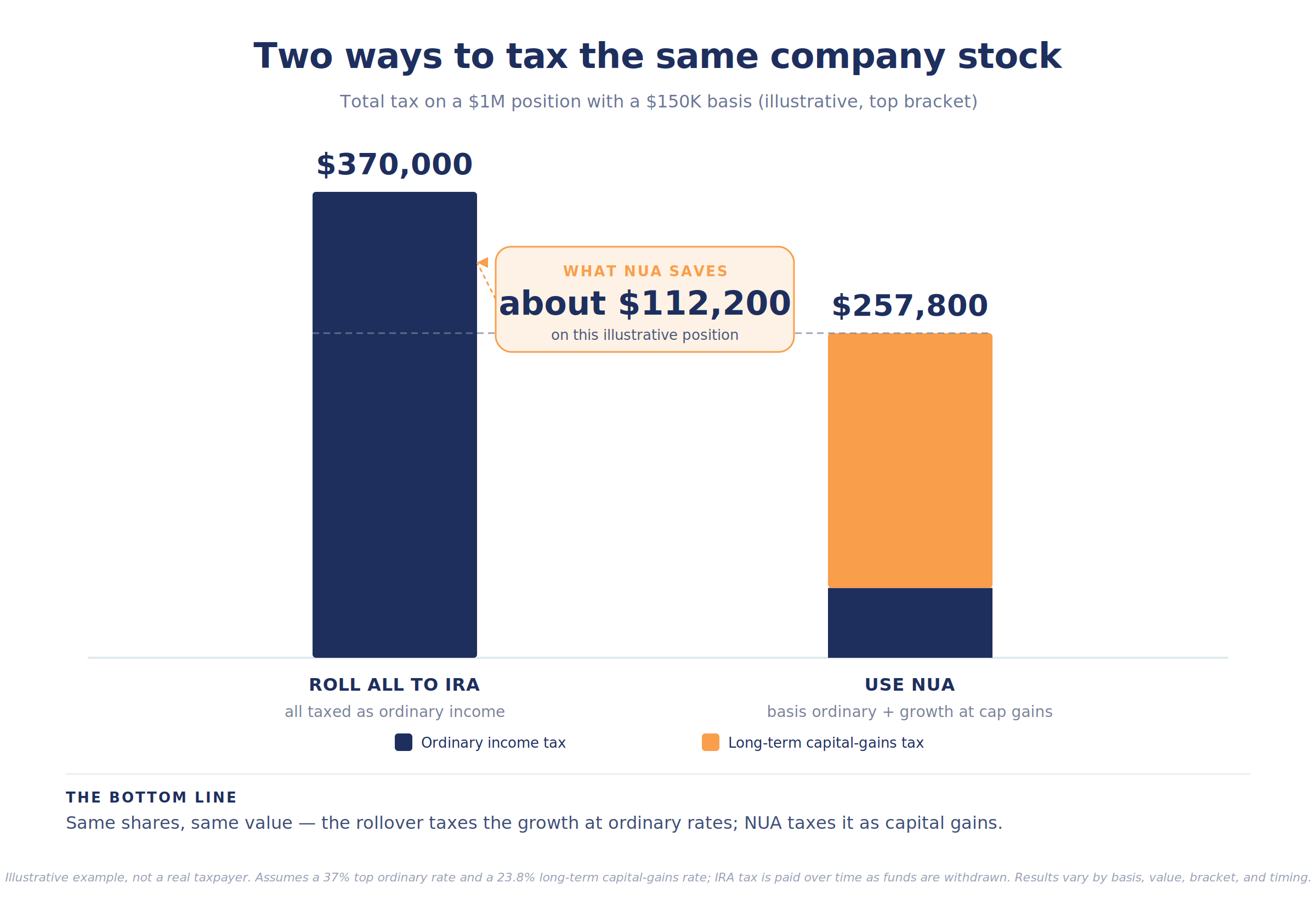

Here’s the trap. Inside a traditional 401(k), every dollar that eventually comes out is taxed as ordinary income — the highest-rate bucket there is. Roll that company stock into an IRA along with everything else, and you lock in ordinary-income treatment on all of it, forever. Decades of appreciation that could have been taxed as capital gains gets converted into ordinary income with a single, well-intentioned form.

There’s a provision in the tax code written specifically to prevent that. It’s called net unrealized appreciation, and almost nobody uses it — because almost nobody hears about it before the rollover paperwork is already filed.

What net unrealized appreciation actually is

NUA is just the growth on your company stock inside the plan — the gap between what the shares cost when they went into your account (the cost basis) and what they’re worth when they come out.

The strategy works by splitting the two pieces apart and taxing each at its own rate:

• The cost basis — what you originally paid — is taxed as ordinary income in the year you take the stock out. On low-basis stock, that’s the small number.

• The appreciation (the NUA) is taxed at long-term capital gains rates when you eventually sell — no matter how long you’ve held the shares, even if you sell a single day later.

That second line is the whole point. Long-term capital gains top out at 20%, plus the 3.8% surtax for high earners — call it roughly 24% at the high end — while ordinary income tops out at 37%. On a large, low-basis position, moving the appreciation from the 37% column to the 24% column is the difference, and it can run well into six figures.

Why the default rollover quietly costs you

This gets missed because the default sounds so reasonable. “Roll your old 401(k) into an IRA” is good advice most of the time — it keeps the money tax-deferred, consolidates accounts, and simplifies life.

But the moment company stock lands in an IRA, the NUA opportunity is gone permanently. There’s no election to make later, no amended return that fixes it. The appreciation that could have been capital gains is now locked into ordinary-income treatment for good — coming out a chunk at a time as you draw on the IRA, or all at once as ordinary income for your heirs.

The rollover isn’t the safe default for company stock. It’s an irreversible tax decision dressed up as a routine administrative step.

The rules that make or break it

NUA is powerful but unforgiving. The mechanics have to be right, or the whole benefit evaporates:

• It takes a lump-sum distribution. You have to empty the entire plan balance in a single tax year, triggered by a qualifying event — commonly leaving the company, or reaching 59½, disability, or death.

• The stock goes out in kind. The company shares are transferred in-kind to a taxable brokerage account, while the rest of the plan — the mutual funds, the bonds — can roll into an IRA at the same time. Only the company stock uses NUA treatment.

• The cost basis matters enormously. The lower your basis relative to today’s value, the bigger the win. Get the basis in writing from the plan administrator before anything moves; the plan tracks it lot by lot.

• Timing the sale is its own decision. Once the shares are in the brokerage account, you choose when to sell — which means you can spread sales across years to manage your brackets, including the lower-income window many retirees have between retirement and Social Security or required distributions.

One caution: if you’re under 59½, the ordinary-income tax on the basis can also carry a 10% early-withdrawal penalty. The appreciation itself generally isn’t penalized, but the basis piece can be.

When it’s worth it — and when it isn’t

NUA isn’t automatically the right move. It shines in a specific situation: a large position, a low cost basis, and a high ordinary-income bracket — the wider the gap between basis and value, the more there is to save.

It’s less compelling when the basis is high relative to current value, when the position is small, or when you’d have to pay the ordinary-income tax on the basis from money you don’t have on hand. And concentration is a real consideration — holding a big single-stock position for tax reasons can collide with the case for diversifying. Sometimes the right answer is to take the NUA treatment and then sell the position down deliberately; sometimes it isn’t worth the complexity at all.

There’s also an estate wrinkle: unlike most assets, the NUA portion doesn’t get a step-up in basis at death — your heirs still owe capital gains on it when they sell. That doesn’t kill the strategy, but it belongs in the math.

The pattern

The rollover isn’t the decision. It feels like a single administrative choice, but for company stock it’s really a permanent tax election hiding inside a routine step — and the routine version is often the expensive one.

This is the kind of thing that has to be caught before it happens. After the shares are in the IRA, there’s no fixing it. The work is the conversation in the months before you retire or change jobs — your advisor flagging the company stock, your CPA running the basis-versus-rate math, and the two deciding together whether to peel the stock out under NUA or let it ride.

For company stock, the standard rollover isn’t a convenience. It’s a permanent tax decision most people make by accident.

The paperwork you file when you leave a job is a snapshot of a decision made under time pressure, often by checking a box. NUA is a reminder that some of those boxes can’t be unchecked. The work is knowing which ones — before you check them.

The plan is the residue. The planning is the work.

Key takeaways

• Company stock held inside a 401(k) can qualify for “net unrealized appreciation” treatment that most rollovers forfeit.

• With NUA, you pay ordinary income tax only on the stock’s cost basis; the appreciation is taxed at long-term capital-gains rates when sold.

• Rolling company stock into an IRA permanently locks in ordinary-income treatment — there’s no way to undo it.

• The strategy requires a lump-sum distribution of the whole plan in one year, with the company shares moved in kind to a taxable account.

• NUA is most valuable with a large, low-basis position and a high ordinary-income bracket; it’s weaker when appreciation is small.

• The NUA portion doesn’t receive a step-up in basis at death, so heirs still owe capital gains on it.

Common questions about net unrealized appreciation

What is net unrealized appreciation?

It’s the growth on company stock inside your 401(k) — the gap between what the shares cost and what they’re worth at distribution. NUA rules let that growth be taxed at capital-gains rates instead of ordinary income.

Why is rolling company stock into an IRA a problem?

Once it’s in the IRA, all of it — including decades of appreciation — comes out as ordinary income, and the NUA election is gone for good.

How do I actually use NUA?

You take a lump-sum distribution of the entire plan in one calendar year after a qualifying event, move the company shares in kind to a taxable brokerage account, and can roll the rest into an IRA.

Do I have to sell the stock right away?

No. The appreciation is taxed at long-term capital-gains rates whenever you sell, even the next day, so you can time sales across years to manage your brackets.

Is NUA always the better choice?

No. It depends on your cost basis, the size of the position, your tax bracket, and whether holding a concentrated stock position fits your plan. The math has to be run case by case.

What if I’m not yet 59½?

The ordinary-income tax on the cost basis may also carry a 10% early-withdrawal penalty. The appreciation generally isn’t penalized, but the basis piece can be.

This article is for informational and educational purposes only and is not intended as tax, legal, or financial planning advice. Tax rates and NUA rules can change, and their application depends on your specific circumstances. Net unrealized appreciation strategies are complex and generally irreversible once executed; consult your CPA, tax advisor, and financial advisor before taking any distribution.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

*Source: irs.gov