Most business owners can name what their company is “worth.” Far fewer can name what they’ll actually keep from a sale, and almost none can name what they need their net proceeds to be to fund the post-exit life they’ve described. Those are different numbers. The gaps between them determine whether an exit works.

The most common conversation in our office that starts with a business owner saying “I think the business is worth around $X” ends, several months later, with a different conversation about a different set of numbers. Not because the original number was wrong. Because the original number was incomplete.

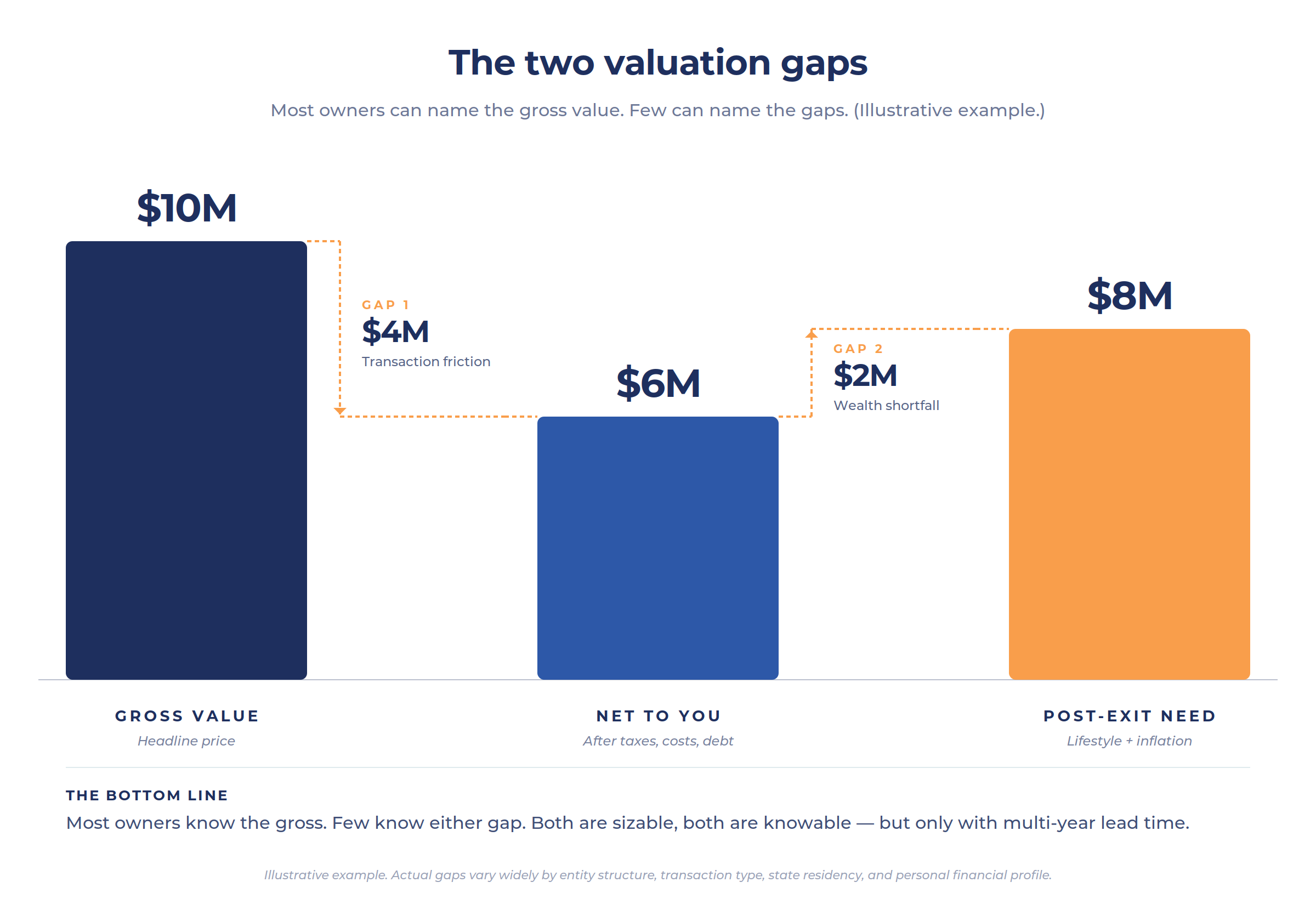

Business owners tend to think about their company’s worth as a single figure — typically a multiple of EBITDA, derived from an industry rule of thumb, sometimes informed by what a comparable business sold for a few years ago. That number isn’t wrong as a starting point. It’s just not the number that determines whether the exit works.

Two other numbers do. The size of the gaps between them determines whether an owner walks away with the post-exit life they planned for, or with a surprise.

The first gap: what the business sells for vs. what you keep

Headline valuation is gross. What an owner walks away with is net. Between those two numbers sits a category of friction that most owners haven’t modeled and many advisors don’t surface until late in the process.

The components:

• Federal capital gains tax. Long-term rates plus the 3.8% Net Investment Income Tax. For business sales structured as stock sales of qualifying QSBS, federal capital gains may be partially or fully excluded (see the prior post in this series on QSBS). For most transactions, the federal tax is a real, substantial number.

• State tax. California taxes capital gains at ordinary income rates — up to 13.3% at the top bracket, with no special treatment. State residency at the time of the transaction affects this materially.

• Ordinary-income components. Personal goodwill, employment agreements, non-compete payments, deferred compensation, and certain earnout structures get treated as ordinary income rather than capital gain. The blend can shift the effective rate significantly higher than the headline capital-gains rate.

• Transaction costs. Investment banking fees (often 2–5% of deal value), legal fees, accounting fees, due diligence costs, broker commissions. For a meaningful transaction, the all-in cost can run 5–10% of headline value.

• Working capital adjustments. Almost every transaction includes a working capital target. Falling below it reduces the purchase price, dollar for dollar, at closing.

• Escrow holdbacks. Typically 10–15% of purchase price held back for 12–24 months against indemnification claims. That money is yours eventually, if no claims arise — but it’s not money you have on closing day.

• Earnouts. When a portion of the price is paid contingent on post-closing performance, that portion isn’t guaranteed. Earnouts pay out partially in most cases, fully in a minority of cases, and not at all more often than buyers and sellers expect at signing.

• Debt payoff. Outstanding business debt comes off the top of proceeds. For owners with leveraged growth strategies, this can be a significant component.

The result: for many transactions, the gap between headline value and what the owner actually has in their personal account a year after closing is 30–50% of the gross number. Not 5%. Not 10%. Often closer to 40%.

Owners who model this gap before the transaction can structure to reduce it. Owners who don’t tend to discover it during diligence — when many of the structural decisions that could have reduced it have already been made.

The second gap: what you keep vs. what you need

Even after the first gap is fully accounted for, the net number isn’t the number that matters. The number that matters is whether that net is enough to fund the post-exit life the owner described.

This is the part most business owners underestimate. Not because they’re unrealistic about their lifestyle — they’re often realistic about today’s. They underestimate future-state requirements:

• Lifestyle expansion in retirement. Post-exit life is often more expensive than pre-exit life, not less. Travel, healthcare, family support, philanthropy, and discretionary spending tend to expand when work no longer fills the calendar.

• Healthcare. Especially in the gap years between business exit and Medicare. ACA exchange coverage for an early-60s couple can run $25,000–35,000 per year, and most exiting business owners don’t qualify for subsidies at their income level.

• Inflation over a 30+ year horizon. A 65-year-old today has reasonable odds of living to 90+. That’s three decades of compounding inflation against a portfolio that needs to provide income.

• Taxes on investment income post-sale. After the exit, the investment portfolio becomes the income source. Interest, dividends, and realized gains all carry tax. For owners with substantial net proceeds, the post-exit tax bill is often higher than ordinary income tax was before.

• Family obligations. Adult children’s housing, education, and starting capital. Aging parents. Multigenerational support that wasn’t on the household balance sheet during peak earning years.

• Estate planning capacity. What the owner wants to transfer to family, charity, or other beneficiaries — and what infrastructure is needed to do that efficiently.

The classic exit planning finding: owners’ personal financial needs are larger than they thought, and their business is worth less than they thought. Both gaps converge in the wrong direction.

Why owners don’t know the size of either gap

No formal valuation has been done. Industry data suggests only about 62% of affluent business owners have had a recent formal valuation. The other 38% are working from rules of thumb.

The personal financial projection isn’t rigorous. A spreadsheet showing today’s spending extended forward at 3% inflation is not a post-exit financial plan. It misses healthcare in the gap years, taxes on investment income, family obligations, and the lifestyle expansion that often follows exit.

The tax math isn’t modeled. “I’ll figure out taxes at exit” is one of the most expensive sentences in business ownership.

There’s no separation between business and personal balance sheet. For many owners, the business is the financial plan. The retirement account, the personal savings, the family home are footnotes. That works until it doesn’t — typically at the moment of transaction.

What changes when you know the gaps

The decision space transforms.

For an owner whose first gap is larger than they thought — net well below the headline number — the levers are operational and structural: improving deal terms, restructuring entity type, positioning for QSBS treatment, timing residency for state tax purposes, separating personal goodwill from enterprise value, restructuring earnout terms.

For an owner whose second gap is larger than they thought — need well above net — the levers are different: extending the runway by growing business value, building outside assets, adjusting lifestyle expectations, refining the timing of exit.

For an owner whose gaps are smaller than they thought — yes, this happens — the conversation becomes: when do you actually want to exit, given that the financial constraint isn’t the binding constraint anymore?

The CEPA framework refers to the point where the gaps close as the “freedom point.” It’s the moment when exit becomes optional rather than financially necessary. Reaching it is a planning outcome, not an accident. And it can’t be reached the year of the exit.

The pattern

For most of this series, the underlying theme has been that planning isn’t paperwork. Estate planning isn’t the document. Roth conversions aren’t a one-time decision. SALT relief isn’t the headline number. Each example points to the same thing: the work that determines whether a plan succeeds happens years before the moment the plan is supposed to deliver.

Business exit is the clearest example. The valuation matters. The gaps matter more. The size and trajectory of both gaps is knowable, modelable, and adjustable — but only with lead time. By the time of the transaction, neither gap can be materially changed.

Business value is one number. The two gaps are the planning.

The plan is the residue. The planning is the work.

Key takeaways

• Most business owners think about company value as a single number — typically a multiple of EBITDA. That’s a starting point, not the answer.

• Two gaps determine whether an exit works: the gap between gross sale value and net to owner (taxes, transaction costs, working capital, escrow, debt), and the gap between net to owner and what’s needed to fund the post-exit life.

• The first gap commonly runs 30–50% of headline value for owners who haven’t structured the transaction with it in mind.

• The second gap is often underestimated because lifestyle expansion, healthcare in the gap years, taxes on investment income, and family obligations weren’t fully modeled.

• Both gaps are knowable, modelable, and adjustable — but only with multi-year lead time. By exit year, neither can be materially changed.

• The “freedom point” — where the gaps close — is a planning outcome, not an accident.

Common questions about the valuation gap

What is the valuation gap?

In exit planning, the “valuation gap” refers to the difference between what a business is currently worth and what’s needed to fund the owner’s post-exit life. In practice, two distinct gaps are involved: (1) the gap between gross business value and what the owner actually keeps after taxes, transaction costs, and other friction, and (2) the gap between what the owner keeps and what they need to fund their post-exit life.

How much do business owners typically lose between gross and net proceeds?

The friction varies significantly based on entity structure, transaction type, state residency, and deal structure. For many transactions, the all-in reduction — federal and state taxes, transaction costs, working capital adjustments, escrow holdbacks, debt payoff, and ordinary-income components — runs 30–50% of headline value. For C-corporation owners holding QSBS-qualifying stock, federal capital gains may be partially or fully excluded, materially reducing the friction. The exact number depends on facts and structuring.

What is the difference between business value and exit-ready value?

Business value is what the business would sell for in a transaction today, based on financial performance and market conditions. Exit-ready value is what the business needs to be worth — combined with the owner’s other assets and net of taxes and transaction costs — for the owner to fund the life they want after the transaction. The first is determined by the market. The second is determined by the owner’s personal financial requirements.

Why do business owners overestimate what they'll keep from a sale?

A few reasons recur. Most owners think in terms of gross value rather than net proceeds. They underestimate transaction costs (often 5–10% all-in). They underestimate state and federal tax on the sale. They overlook ordinary-income components (personal goodwill, non-competes, deferred comp). They don’t account for working capital adjustments or escrow holdbacks. They sometimes treat earnout payments as guaranteed when they’re often partial. The accumulation compresses headline value into net proceeds by 30–50% in many transactions.

What is the “freedom point” in exit planning?

The “freedom point” — a term used in the Certified Exit Planning Advisor (CEPA) framework — is the moment when the value of a business owner’s total wealth (business + other assets) is sufficient to fund the personal financial requirements of their post-exit life, after taxes and transaction costs. At the freedom point, exit becomes optional rather than financially necessary. Reaching it earlier rather than later changes the negotiating dynamic of any eventual transaction.

When should a business owner have a formal valuation done?

Most exit planning frameworks recommend a formal business valuation well before the contemplated exit window — typically 3–5 years out, with updates every 1–2 years thereafter. The valuation isn’t just for the eventual transaction; it’s a planning input that informs operational priorities, tax structure decisions, gifting strategies, and personal financial projections. Industry data suggests only about 62% of affluent business owners have had a recent formal valuation, leaving most working from rules of thumb that may not reflect their actual market position.

This article is for informational and educational purposes only and is not intended as tax, legal, business valuation, or financial planning advice. Business sale outcomes depend on a wide range of facts including entity structure, transaction type, state residency, deal terms, and individual financial circumstances. Consult your CPA, corporate attorney, financial advisor, and a qualified business valuation professional about your specific situation.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.