Almost every conversation about investing is about allocation — how much in stocks, how much in bonds, how to diversify. That’s the right place to start. But there’s a second decision that gets almost none of the attention and quietly shapes how much of your return you actually keep: not what you own, but which account you keep it in.

Picture two investors with the exact same portfolio — same funds, same stock-and-bond mix, same everything. The only difference is where each piece sits: which holdings are in the taxable brokerage account, which are in the traditional IRA, which are in the Roth. Over a few decades, those two identical portfolios can deliver meaningfully different after-tax wealth.

That second decision is asset location, and it’s one of the few things in investing that’s close to a free lunch — a way to improve your after-tax return without taking on more risk, changing your allocation, or predicting anything. It just requires putting the right assets in the right accounts. Most people never do it deliberately.

Allocation versus location

Asset allocation is what you own — the mix of stocks, bonds, and other assets that sets your risk and return. Asset location is which type of account holds each of those pieces. They’re different decisions, and the second only matters because the three kinds of accounts are taxed in completely different ways.

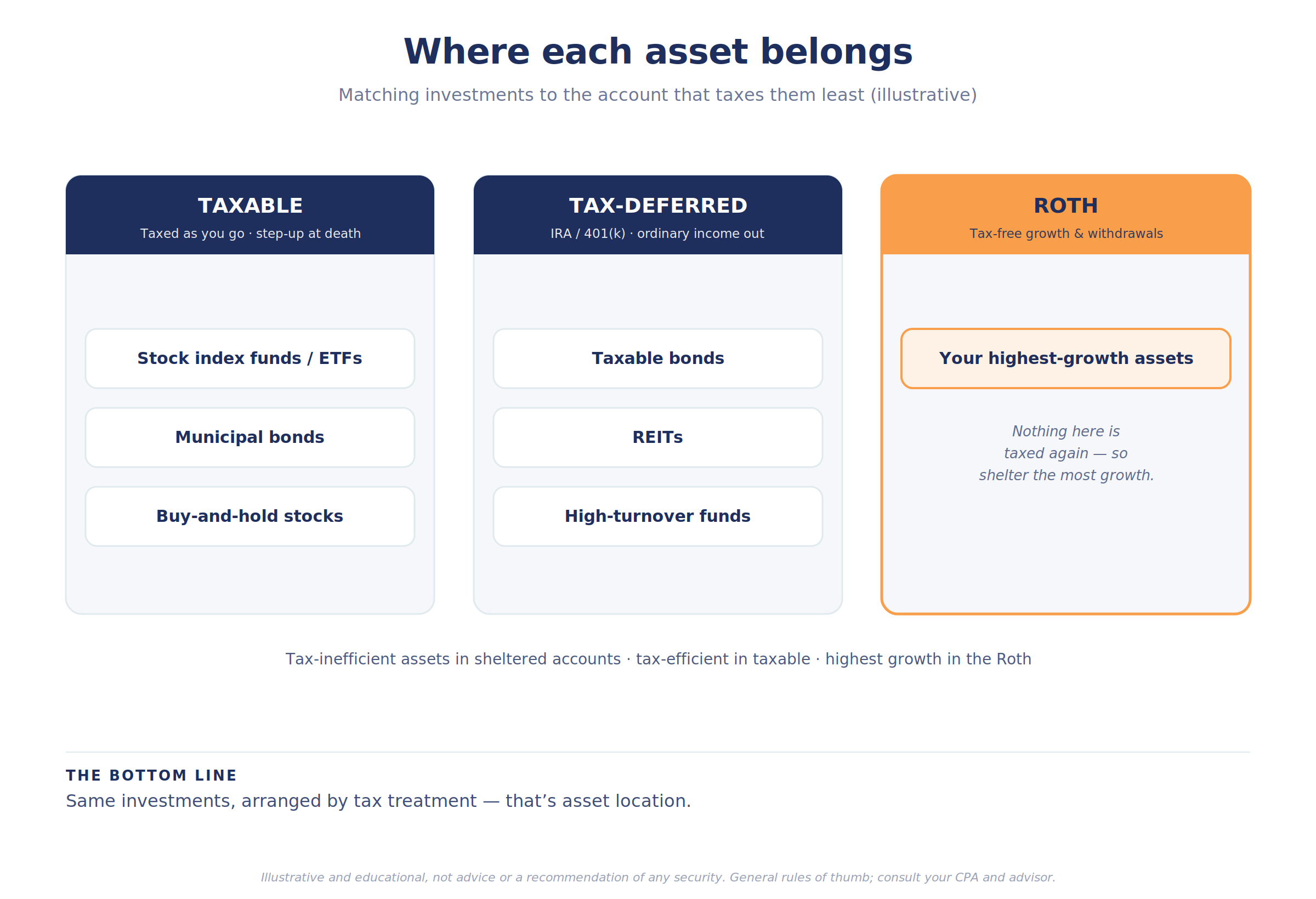

• Taxable accounts (a regular brokerage account). You pay tax along the way: on interest, on dividends, and on gains when you sell. But long-term capital gains and qualified dividends get preferential rates, you control when you realize gains, you can harvest losses, and the assets get a step-up in basis at death.

• Tax-deferred accounts (traditional IRA, 401(k)). Nothing is taxed while it grows, but everything that comes out is taxed as ordinary income — even the portion that would have been a low-taxed capital gain in a brokerage account.

• Tax-free accounts (Roth). Nothing is taxed while it grows, and qualified withdrawals come out completely tax-free. This is the most valuable space you have.

Because the same investment is taxed differently depending on which bucket it lives in, where you put each asset changes your after-tax result.

The basic logic

The core idea is simple: match each asset to the account where its tax treatment hurts the least.

• Put tax-inefficient assets in tax-sheltered accounts. Things that throw off heavily taxed income year after year — taxable bonds and bond funds (interest is taxed as ordinary income), REITs, and high-turnover strategies — generally belong in a traditional IRA or 401(k), where that annual tax drag disappears.

• Keep tax-efficient assets in taxable accounts. Broad stock index funds and ETFs are naturally tax-efficient: low turnover, mostly qualified dividends, and gains you choose when to realize. They’re comfortable in a taxable account, where they also pick up the step-up in basis at death.

• Put your highest-growth assets in the Roth. Since nothing in a Roth is ever taxed again, it’s the best home for the assets you expect to grow the most. Tax-free growth is worth the most when there’s the most growth to shelter.

None of this changes your overall allocation. You still own the same mix — you’ve just arranged it so the tax code takes a smaller bite.

The mistakes that cost the most

A few placement errors show up again and again:

• Municipal bonds inside an IRA. Municipal bond interest is already federally tax-free. Holding munis in a tax-deferred account wastes that exemption — and worse, converts their tax-free interest into ordinary income when it eventually comes out. Munis, if you own them, belong in a taxable account.

• Taxable bonds in a taxable account for a high earner. For someone in a top bracket, holding taxable bonds in a brokerage account means paying ordinary-income rates on the interest every year. That same bond exposure, tucked into a tax-deferred account, avoids the annual hit.

• Turning capital gains into ordinary income. Hold a high-growth stock fund in a traditional IRA and every dollar of that growth eventually comes out as ordinary income — losing the preferential long-term capital-gains rate it would have qualified for in a taxable account.

• Forgetting the step-up. Highly appreciated assets held in a taxable account get a step-up in basis at death, which can erase the embedded gain for your heirs. That’s a reason to hold certain appreciated positions in taxable accounts rather than spending them down first.

Why it ties everything together

Asset location isn’t a standalone trick; it’s the thread that connects a lot of the other decisions in a financial plan.

The size and makeup of your tax-deferred accounts drive your future required minimum distributions and can push you into IRMAA surcharges — so what you hold there, and how fast it grows, matters years later. The value of your Roth space shapes how aggressively to use it and whether to do conversions. The step-up in basis influences which accounts to spend from first. Location is where investment management and tax planning actually meet — and it’s the kind of thing that only works when someone is looking at the whole household balance sheet at once, not each account in isolation.

This is the heart of tax-aware portfolio management: managing the entire portfolio across every account for after-tax return, within a disciplined, rules-based framework — rather than treating each account as its own island.

The caveats

A few honest qualifiers:

• It only matters if you have meaningful assets across more than one type of account. If everything you have is in a 401(k), there’s nothing to locate.

• Allocation comes first. Don’t distort your risk level chasing a tax benefit — the investment decision leads, and location optimizes around it. The tax tail shouldn’t wag the investment dog.

• It adds complexity. Because your allocation now spans several accounts, you have to rebalance at the household level, not account by account, and keep the whole picture in view.

The pattern

Asset allocation is the decision everyone talks about. Asset location is the one that quietly compounds in the background — invisible on any single statement, worth more with every year and every dollar, and almost entirely within your control.

That’s the through-line one more time: the value is in the part nobody’s looking at. Two portfolios can hold the very same investments and end up worlds apart on an after-tax basis, purely because of where each piece was kept. The arranging is unglamorous and it never shows up as a number you can point to — which is exactly why it gets skipped, and exactly why it’s worth doing.

Asset allocation decides what you own. Asset location decides how much of the return you actually keep.

You can’t control the markets, but you can control how efficiently your accounts are arranged around them — and over a few decades, that arrangement quietly adds up. It’s the least visible decision in a portfolio and one of the most durable. The work is in the arranging, done deliberately and revisited as the plan changes.

The plan is the residue. The planning is the work.

Key takeaways

• Asset allocation is what you own; asset location is which type of account holds each asset — and it can meaningfully change your after-tax results.

• The three account types are taxed differently: taxable (preferential rates on gains and qualified dividends, step-up at death), tax-deferred (everything out as ordinary income), and Roth (tax-free).

• General rule: put tax-inefficient assets (taxable bonds, REITs, high-turnover funds) in sheltered accounts, keep tax-efficient assets (stock index funds) in taxable, and place your highest-growth assets in the Roth.

• Common costly mistakes include holding municipal bonds in an IRA (wasting their tax exemption) and holding taxable bonds in a brokerage account as a high earner.

• Location ties into RMDs, IRMAA, Roth strategy, and the step-up in basis — it’s where investment management and tax planning meet at the household level.

• It only matters with assets across multiple account types, allocation should always come first, and rebalancing has to happen across the whole portfolio, not account by account.

Common questions about asset location

What’s the difference between asset allocation and asset location?

Allocation is the mix of what you own (stocks, bonds, etc.). Location is which type of account — taxable, tax-deferred, or Roth — holds each of those pieces.

Where should I hold bonds?

Tax-inefficient bonds, whose interest is taxed as ordinary income, generally belong in a tax-deferred account like a traditional IRA, especially for higher earners. Municipal bonds are the exception — they belong in a taxable account.

Why are municipal bonds a mistake in an IRA?

Their interest is already federally tax-free, so holding them in a tax-deferred account wastes the exemption and turns tax-free interest into ordinary income when withdrawn.

What belongs in a Roth?

Generally your highest-growth assets, since Roth growth and qualified withdrawals are never taxed — tax-free growth is most valuable where there’s the most growth.

Does asset location change my risk or allocation?

No. You keep the same overall mix; you’re just arranging which account holds which piece to improve the after-tax result.

When does asset location not matter?

When nearly all your money is in a single type of account. The benefit comes from having assets spread across taxable, tax-deferred, and Roth accounts.

This article is for informational and educational purposes only and is not intended as tax, legal, investment, or financial planning advice. The tax treatment of accounts and investments depends on your specific circumstances and can change, and asset location strategies are not appropriate for everyone. Asset allocation and diversification do not ensure a profit or protect against loss in declining markets. Consult your CPA, tax advisor, and financial advisor about your situation before acting.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Via Luce Capital is not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Via Luce Capital, and may also be employees of Via Luce Capital. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of Via Luce Capital.

This commentary may incorporate research and tools provided by Helios Quantitative Research LLC (“Helios”), which is associated with, and under the supervision of, Clear Creek Financial Management, LLC (“Clear Creek”), a Registered Investment Advisor. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital.