A well-drafted plan can still produce a bad outcome — and the failure point is almost never the documents.

The financial plan was good. The estate plan was good. The investment portfolio was sound. The tax strategy was thoughtful. The outcome still missed by hundreds of thousands of dollars.

That's not hypothetical. It's the most common failure pattern in private wealth, and it has very little to do with the documents themselves. Plans rarely fall apart at the documents. They fall apart at the seams — the places where investment decisions, tax timing, estate structure, retirement income, and business strategy are supposed to meet but don't.

A plan is not a binder. A plan is a set of interdependent decisions across domains, drafted individually by specialists and collectively responsible for an outcome that no specialist owns. When the seams hold, the plan works. When they don't, the documents look fine in isolation and the result still misses.

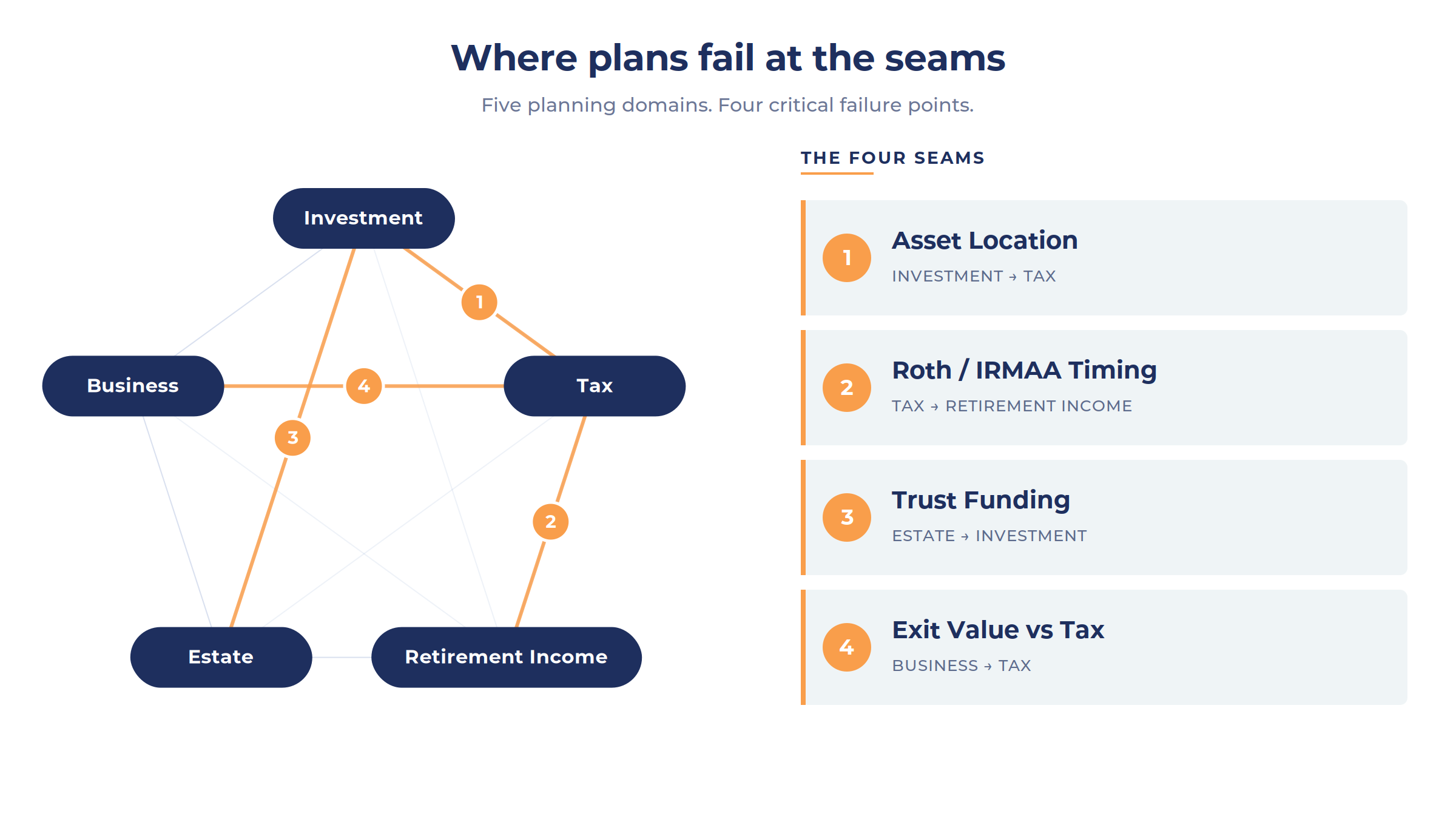

Plans fail at the seams, not the documents

Four examples make the point. They are composites, not specific cases, but the patterns appear constantly.

The trust that was drafted but never funded

A family pays an estate attorney to draft a revocable living trust with thoughtful provisions for asset protection, generational transfer, and tax efficiency. The documents are signed. The binder goes on the shelf. Years later, the grantor passes — and the estate goes through probate anyway, because the assets were never retitled into the trust.

The attorney did her job. The advisor managed the accounts well. No one was accountable for the unglamorous step in between: funding the trust. The seam between drafting and funding got missed, and the entire purpose of the structure went with it.

The Roth conversion that ran into IRMAA

A retired couple and their advisor build a multi-year Roth conversion plan to reduce future required minimum distributions and lower the tax burden on the surviving spouse. The investment logic is clean. The tax-bracket modeling is clean. What the model didn't account for: the conversions push their Modified Adjusted Gross Income across two IRMAA thresholds — the Medicare income-related premium tiers that determine what they pay for Part B and Part D. Their Medicare premiums climb meaningfully for the two years following each large conversion year, because IRMAA uses a two-year lookback. The cost arrives well after the decision was made.

The Roth strategy was right. The tax math was right. The seam between tax planning and healthcare cost planning was missed.

The portfolio with backwards asset location

A balanced portfolio is held across taxable, tax-deferred, and Roth accounts. The asset allocation is appropriate. The fund selection is reasonable. But the allocation across account types runs in the wrong direction: tax-inefficient holdings sit in taxable, tax-efficient holdings sit in the IRA, and high-growth assets sit in accounts where their growth will be most heavily taxed when it comes out.

Academic research on after-tax investing has long estimated that misaligned asset location can quietly cost 50–100 basis points of annualized after-tax return, year after year. The portfolio looks fine. The performance reports look fine. The after-tax wealth curve is meaningfully lower than it should be. The seam between investment selection and tax-location optimization was never addressed.

The exit number that ignored tax

A business owner sells his company for what looks like an $8 million transaction. The personal financial plan is built around an $8 million liquidity event. After federal capital gains, state tax, the net investment income tax, depreciation recapture on certain assets, transaction fees, and net working capital adjustments, he nets roughly $5.4 million.

The same dynamic applies to RSU vesting events, large real estate sales, deferred comp distributions, and any other concentrated liquidity moment. The M&A advisor structured the transaction. The personal financial planner built a reasonable lifestyle around the headline number. No one stress-tested the bridge between what the business cleared and what the owner actually had to retire on. The seam between transaction strategy and personal income planning was a chasm.

Why this keeps happening

The seams keep failing for three structural reasons. None of them are about competence. All of them are about how the work is organized.

Specialists working in silos

The modern advisory ecosystem is deeply specialized. The estate attorney drafts estate documents. The CPA prepares returns and advises on tax. The investment advisor manages portfolios. The insurance broker handles coverage. The M&A advisor runs the transaction. Each is competent in a defined lane. None is accountable for whether the lanes connect.

Specialization produces better work inside each lane and worse outcomes across them. The space between two specialists is no one's job. It defaults to the client, who is rarely positioned to do that job.

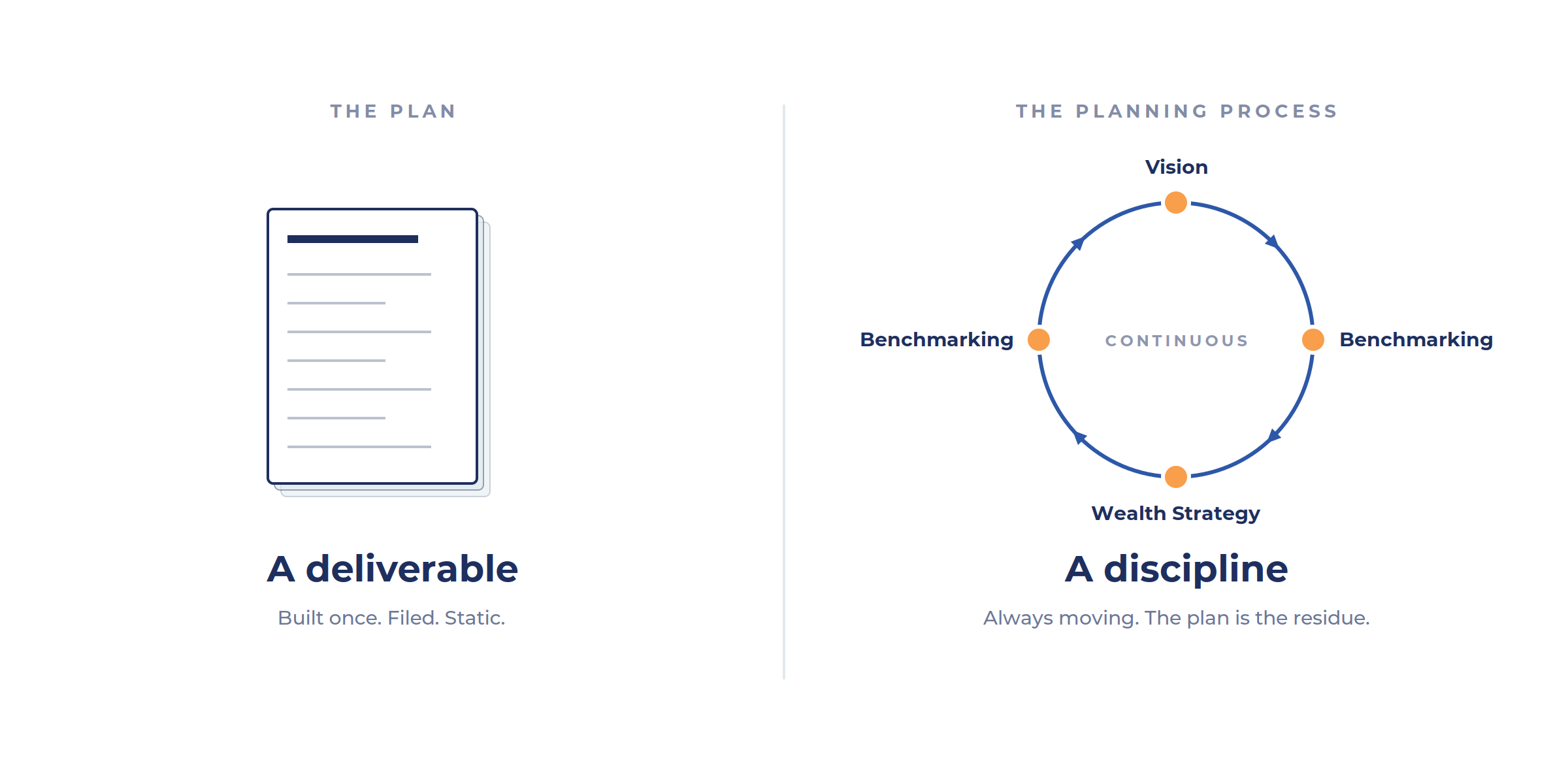

Deliverable-thinking instead of process-thinking

A financial plan is often treated as a document that gets produced, presented, and filed. Once delivered, the engagement effectively pauses until the next "review." But the variables a plan depends on don't pause. Tax law changes. Income changes. Family circumstances change. Markets move. The business grows or shrinks. Children get older. Estate structures age out of relevance.

A plan built on last year's variables doesn't survive contact with this year's reality. Treating the plan as a deliverable rather than the residue of an ongoing process is how the seams open up over time.

No one accountable for the whole picture

Even when a client has a strong roster — attorney, CPA, advisor, insurance broker, banker — often no single person is accountable for whether the parts fit together. The implicit assumption is that the client is the integrator. The client receives recommendations from each specialist, decides what to act on, and is supposedly the one ensuring nothing conflicts.

Most clients don't have the bandwidth, the cross-domain fluency, or the time to do that job — and even if they did, they shouldn't have to. Integrating across domains is itself a skill, not a default capability of being wealthy.

What integration actually requires

Closing the seams isn't a matter of hiring more specialists. It's a matter of organizing the work differently. Three things matter.

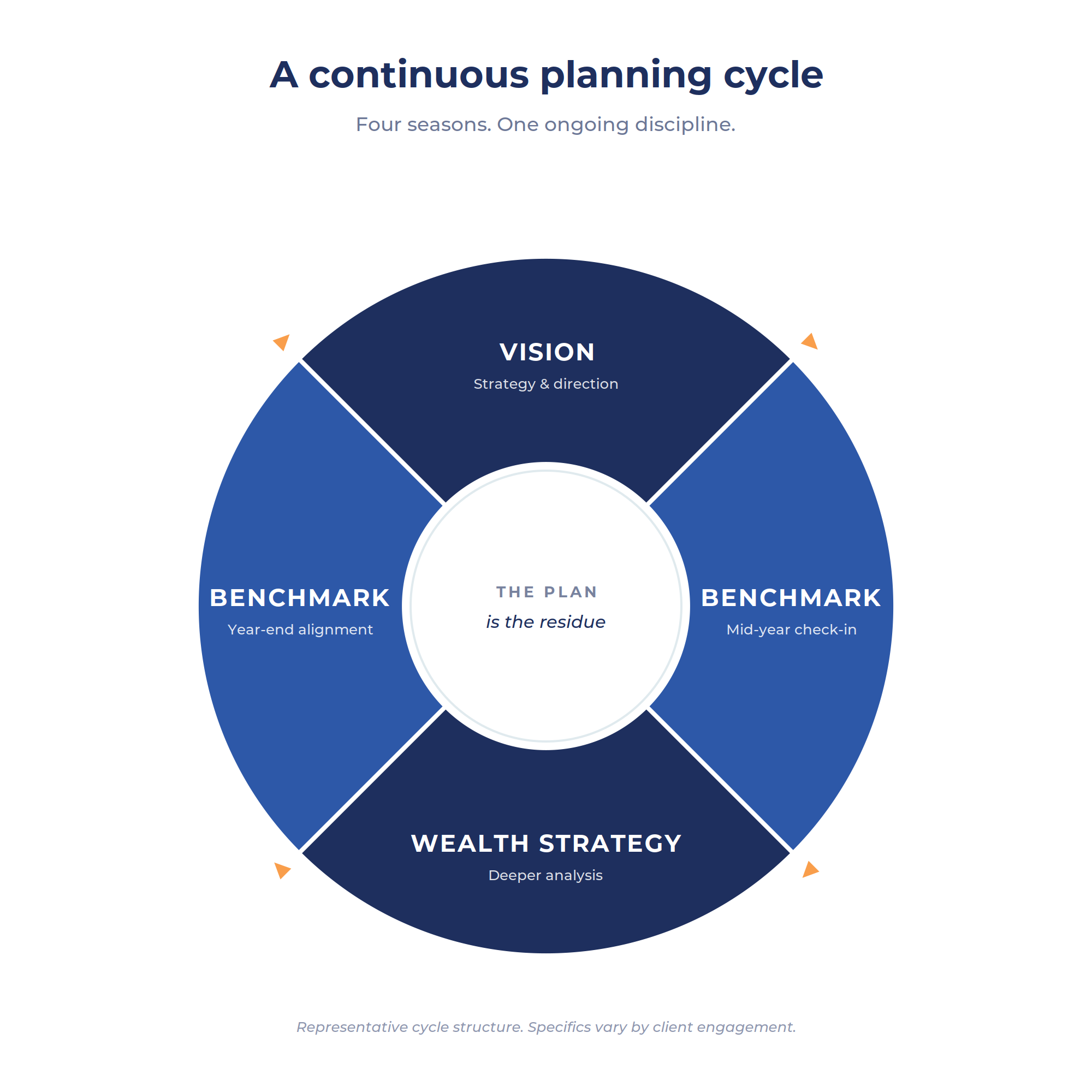

A continuous engagement cycle, not a one-time deliverable. Real planning runs in seasons of the year, each with a different focus — vision and strategic positioning early in the year, implementation benchmarking in the middle, deeper wealth-strategy work mid-year, and another benchmarking pass before year-end. The plan is the residue of that cycle. It isn't the goal of the cycle.

Coordinated work with the rest of the client's team. The advisor doesn't replace the CPA or the attorney. The advisor's job at the seams is to surface where decisions in one lane carry consequences in another, model those consequences before they get committed to, and pull the right specialists into the conversation when a seam needs joint attention. This work is unglamorous, recurring, and exactly where the value lives.

Single-point accountability for whether the parts fit. Boutique by design is not a marketing posture — it's a structural choice. One principal advisor is accountable for whether the plan integrates. Not a team of people each accountable for part of the picture. One person who can say "the trust isn't funded yet — that needs to close before quarter-end," or "the Roth conversion has to land below the IRMAA threshold this year; here is how we cap it." Accountability at the integration layer is what makes the seams hold.

Plans rarely fall apart at the documents. They fall apart at the seams.

The plan is the residue of the process

The deliverable mindset treats the plan as the destination. The integration mindset treats planning as the discipline — and the plan as what gets produced along the way.

The distinction matters because the seam failures described above aren't edge cases. They're the central failure mode of successful families and business owners with strong individual specialists. The documents are usually fine. The integration is usually where the dollars go missing.

Every financial decision sits inside a plan. Whether the plan holds depends entirely on whether someone is accountable for the seams.

Key takeaways

• Financial plans rarely fail at the documents. They fail at the seams between domains — where investment, tax, estate, retirement income, and business decisions are supposed to meet.

• Common seam failures include trusts that are drafted but never funded, Roth conversions that miss IRMAA thresholds, asset location that runs opposite to tax efficiency, and exit values that overlook what's left after tax.

• The seams keep failing because specialists work in silos, plans are treated as deliverables rather than ongoing processes, and no one is structurally accountable for whether the parts fit together.

• Integration requires a continuous engagement cycle, coordinated work with the rest of the client's team, and single-point accountability for the whole picture.

• Planning is the integrating discipline. The plan is the residue.

Examples in this article are illustrative composites and do not reflect specific client situations or outcomes.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).